Thread

1/22

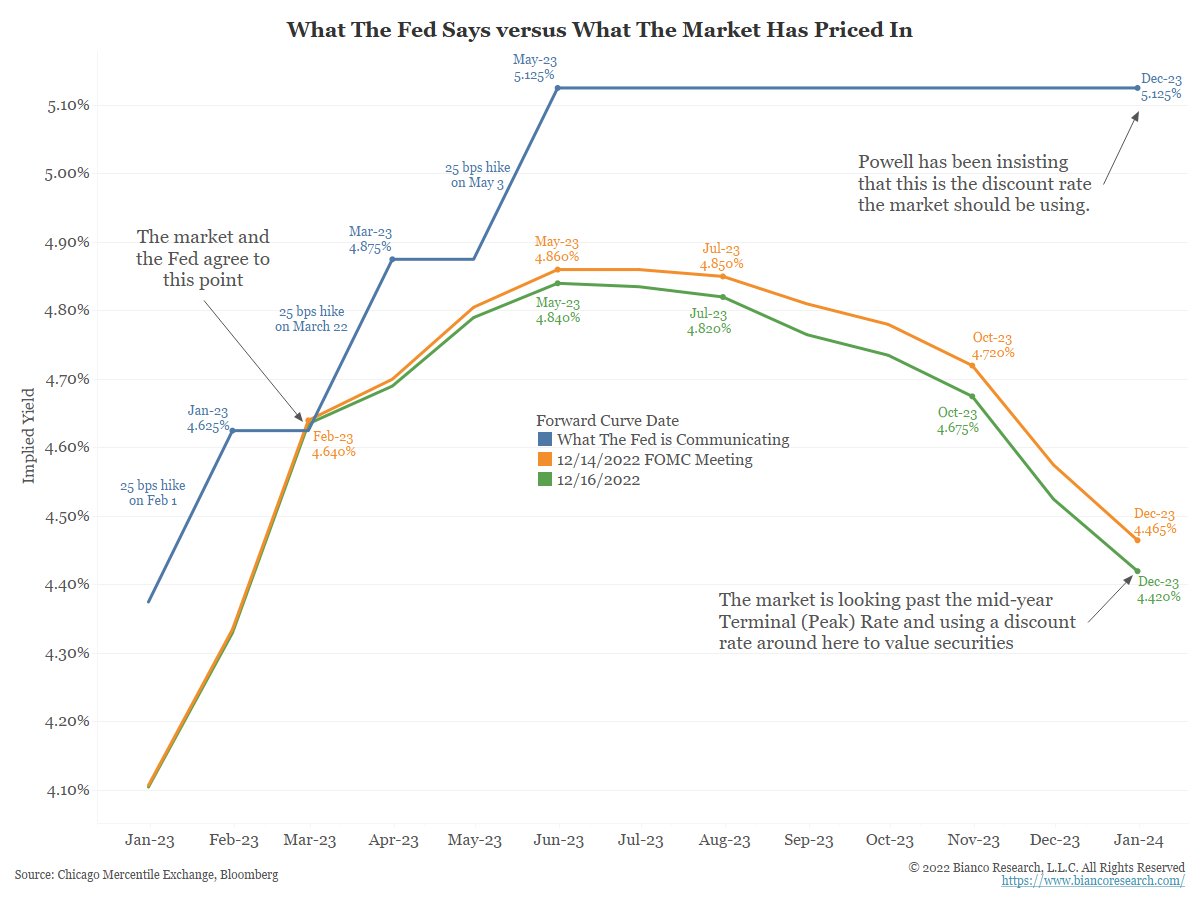

As this chart shows, there is a big difference between what the market and the Fed think.

And this divergence will define the first part of 2023 trading.

A 🧵to explain

As this chart shows, there is a big difference between what the market and the Fed think.

And this divergence will define the first part of 2023 trading.

A 🧵to explain

2/22

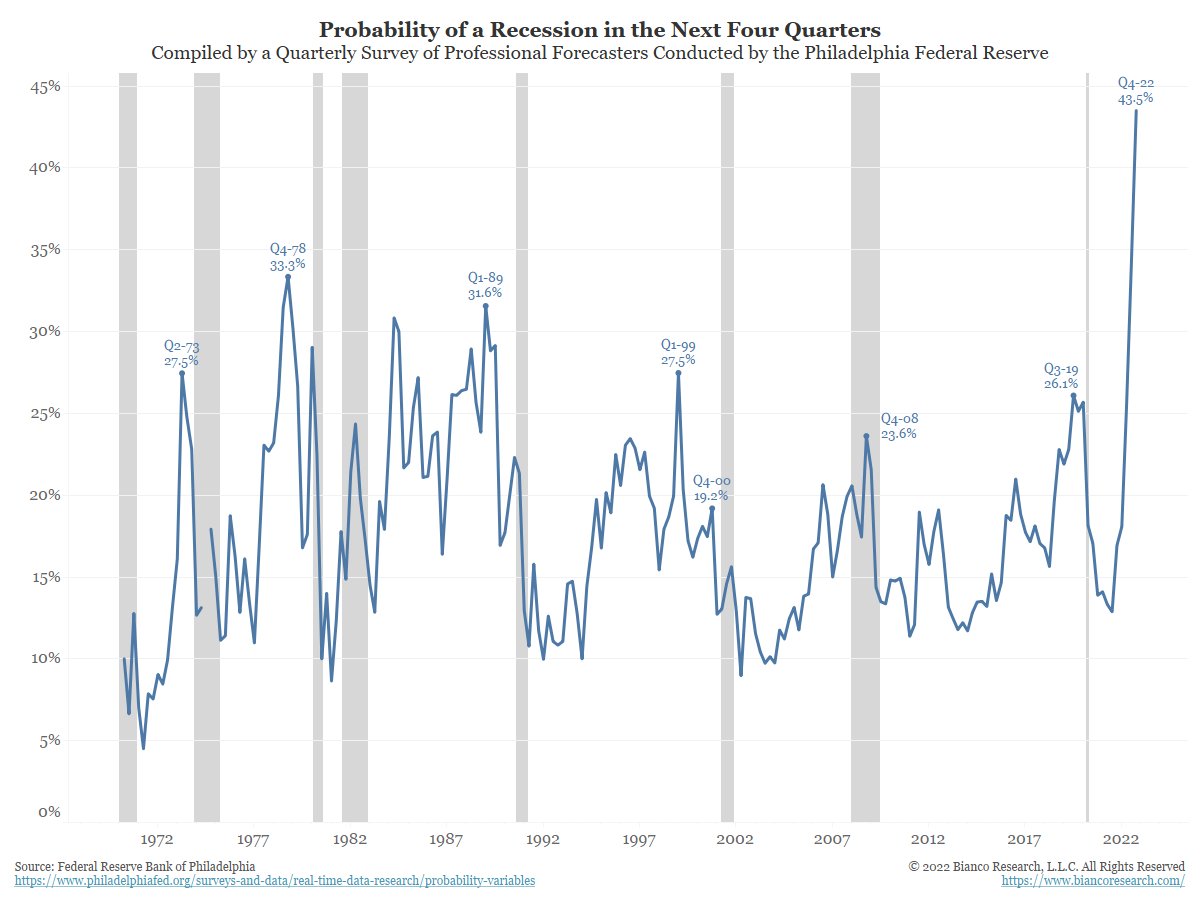

So, why does the market think the Fed will do much less?

The latest Philadelphia Federal Reserve quarterly survey of professional forecasters shows the probability of a recession in the next year is the highest in the 50+ years this survey has been conducted.

So, why does the market think the Fed will do much less?

The latest Philadelphia Federal Reserve quarterly survey of professional forecasters shows the probability of a recession in the next year is the highest in the 50+ years this survey has been conducted.

3/22

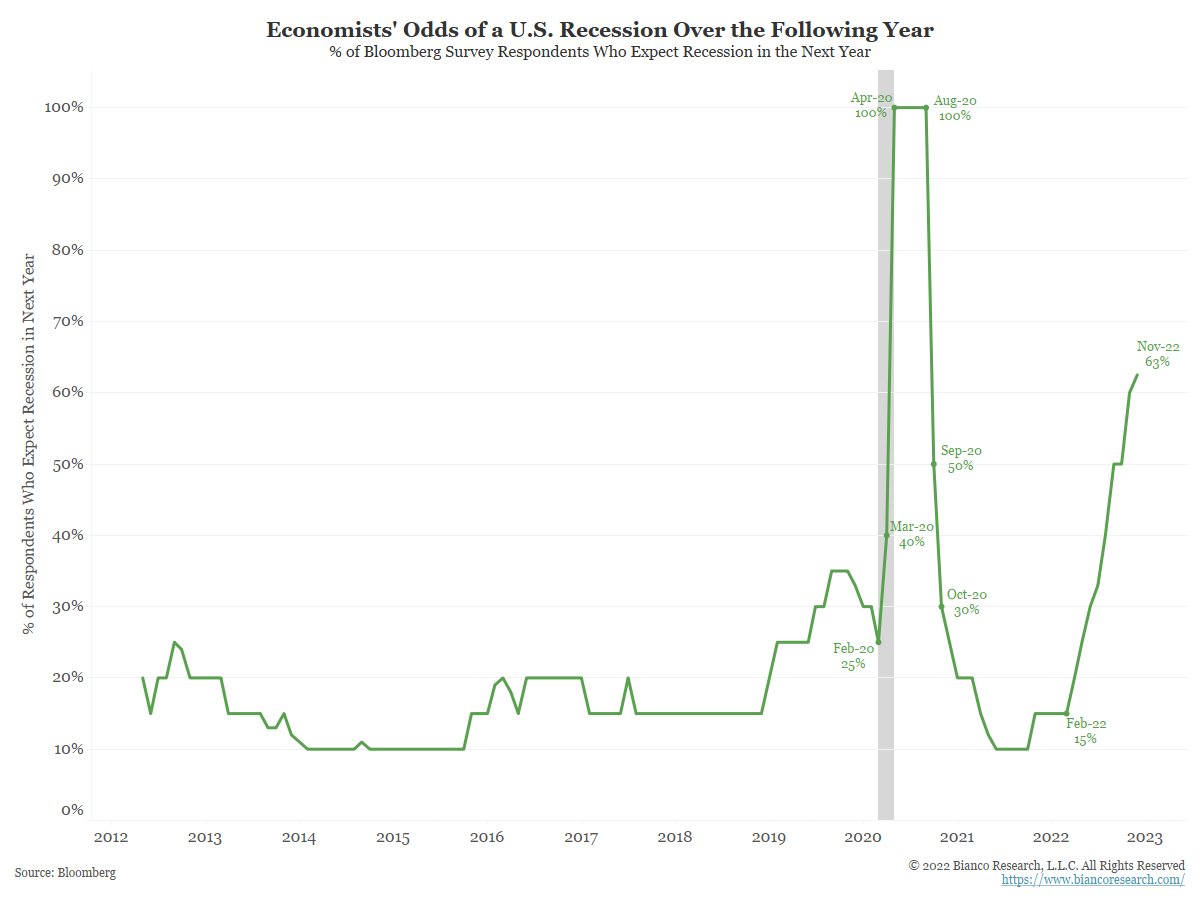

A similar monthly survey conducted by Bloomberg of about 70 economists shows the probability of a recession is even higher at 63%.

This survey began in 2008, and the only time it was higher was when the US economy was actually in recession in 2020.

A similar monthly survey conducted by Bloomberg of about 70 economists shows the probability of a recession is even higher at 63%.

This survey began in 2008, and the only time it was higher was when the US economy was actually in recession in 2020.

4/22

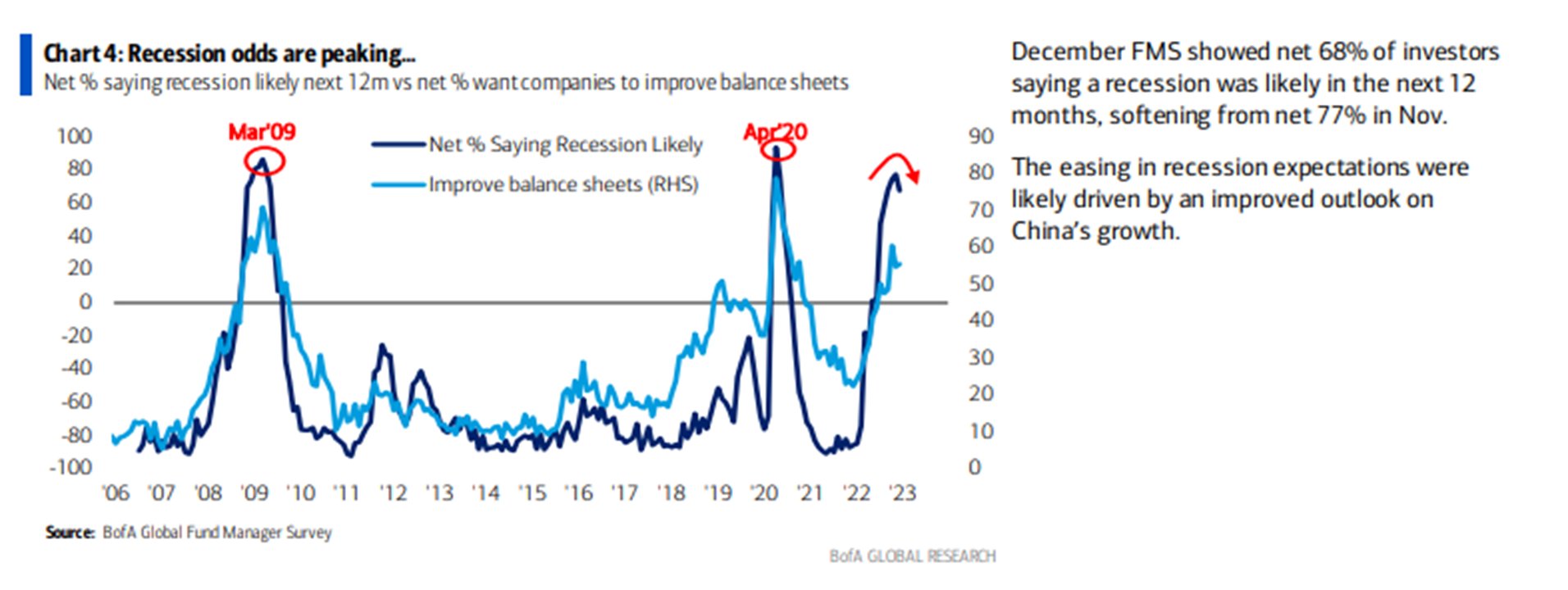

And before you conclude that the 63% of ECONOMISTS predicting a recession "doesn't count," note that the BofA's December Global Fund Managers survey, in which 300 FUND MANAGERS participated, had nearly an identical response at 68%.

And before you conclude that the 63% of ECONOMISTS predicting a recession "doesn't count," note that the BofA's December Global Fund Managers survey, in which 300 FUND MANAGERS participated, had nearly an identical response at 68%.

5/22

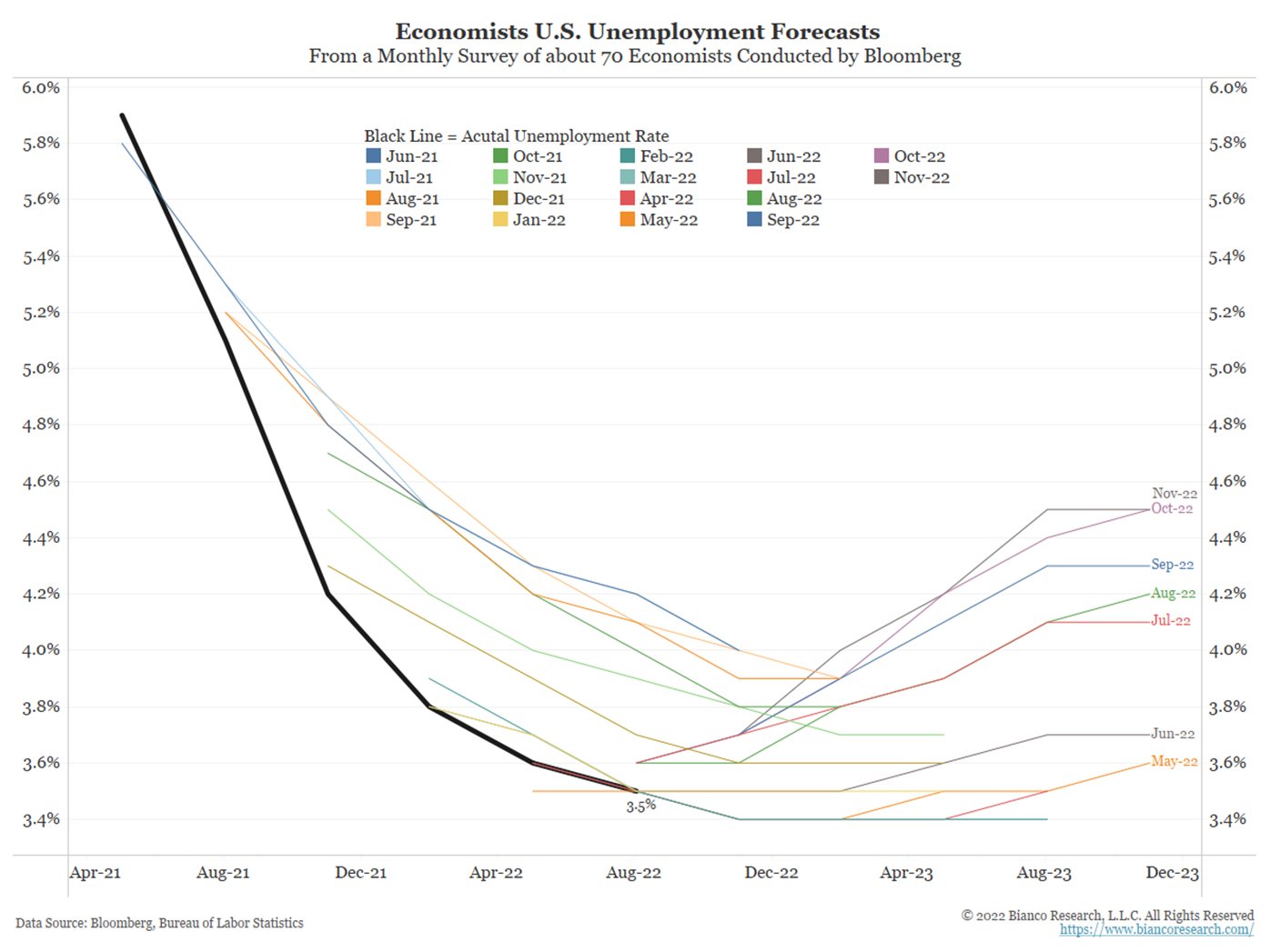

Additionally, economists see the unemployment rate for year-end 2023 will now be 4.5% (Oct and Nov surveys). Note that in May (gold line), they had it at 3.6%.

This is a big rise, and such an increase only occurs in recessions.

Additionally, economists see the unemployment rate for year-end 2023 will now be 4.5% (Oct and Nov surveys). Note that in May (gold line), they had it at 3.6%.

This is a big rise, and such an increase only occurs in recessions.

6/22

So, what does the Fed see causing the fund's rate to stay at 5.125% next year?

Start with the labor market.

The simple truth is the jobs market is NOT weakening. And the Fed is not changing unless it shows UNMISTAKABLE signs of weakening.

Initial claims are NOT rising.

So, what does the Fed see causing the fund's rate to stay at 5.125% next year?

Start with the labor market.

The simple truth is the jobs market is NOT weakening. And the Fed is not changing unless it shows UNMISTAKABLE signs of weakening.

Initial claims are NOT rising.

7/22

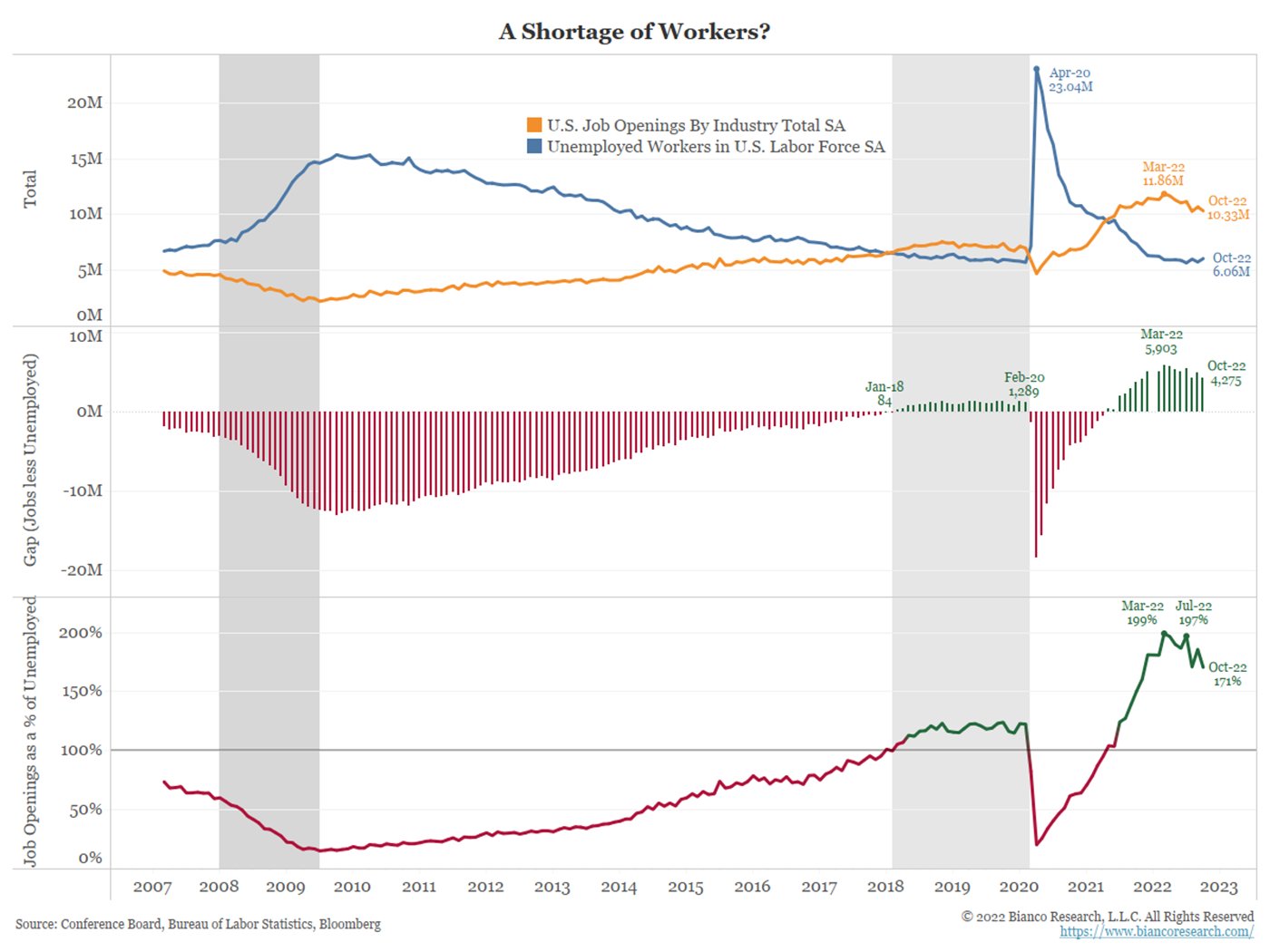

There are 1.7 open jobs for every unemployed person (bottom panel).

There are 1.7 open jobs for every unemployed person (bottom panel).

8/22

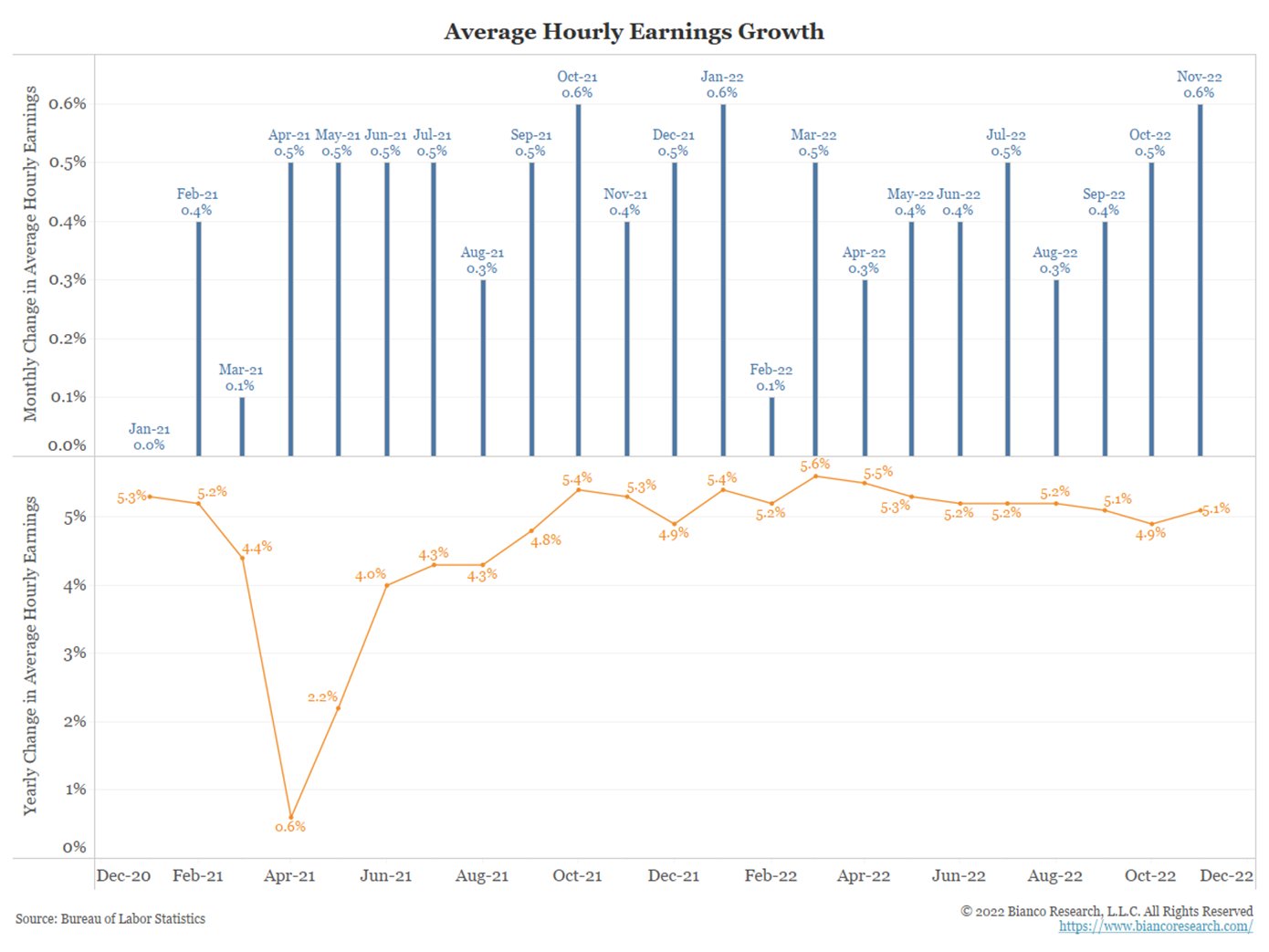

And year-over-year wage growth (orange, bottom panel) is holding around 5%.

Simply, if everyone gets 5% pay raises, they can "afford" 5% inflation.

5% inflation is unacceptable.

And year-over-year wage growth (orange, bottom panel) is holding around 5%.

Simply, if everyone gets 5% pay raises, they can "afford" 5% inflation.

5% inflation is unacceptable.

9/22

So, these are the battle lines. Who will win?

Wall Street has been losing to the Fed all year by insisting the Fed would "pause" then "pivot."

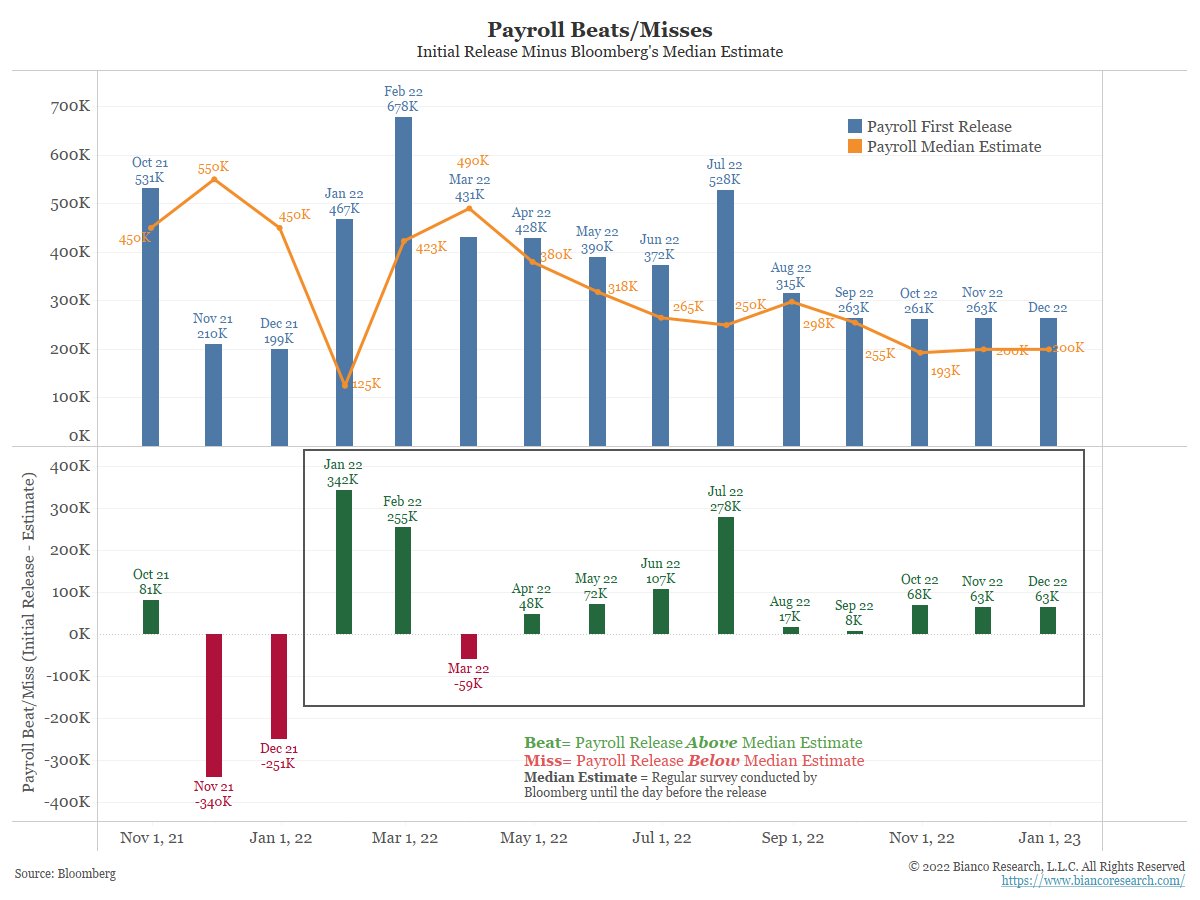

Wall Street has been bearish on jobs. Instead, payrolls have beaten 11 of the last 12 months, including 8 in a row (rectangle).

So, these are the battle lines. Who will win?

Wall Street has been losing to the Fed all year by insisting the Fed would "pause" then "pivot."

Wall Street has been bearish on jobs. Instead, payrolls have beaten 11 of the last 12 months, including 8 in a row (rectangle).

10/22

And the payrolls beating 8 times in a row has a record streak and should tell Wall Street something is amiss ... they are getting the jobs market wrong.

And the payrolls beating 8 times in a row has a record streak and should tell Wall Street something is amiss ... they are getting the jobs market wrong.

11/22

Instead, they are doubling down, that jobs are falling apart.

Their latest rationalization is a big downward revision to Q2 2022 job growth.

Even if true, these revisions are due in Feb 2024 (14 months). So, don't hold your breath!

Instead, they are doubling down, that jobs are falling apart.

Their latest rationalization is a big downward revision to Q2 2022 job growth.

Even if true, these revisions are due in Feb 2024 (14 months). So, don't hold your breath!

12/22

So, if the pattern continues that Wall Street is too pessimistic or too impatient on their pessimism and does not get its "pivot" because the economy does not IMMEDIATELY fall apart, what does it mean for markets?

So, if the pattern continues that Wall Street is too pessimistic or too impatient on their pessimism and does not get its "pivot" because the economy does not IMMEDIATELY fall apart, what does it mean for markets?

13/22

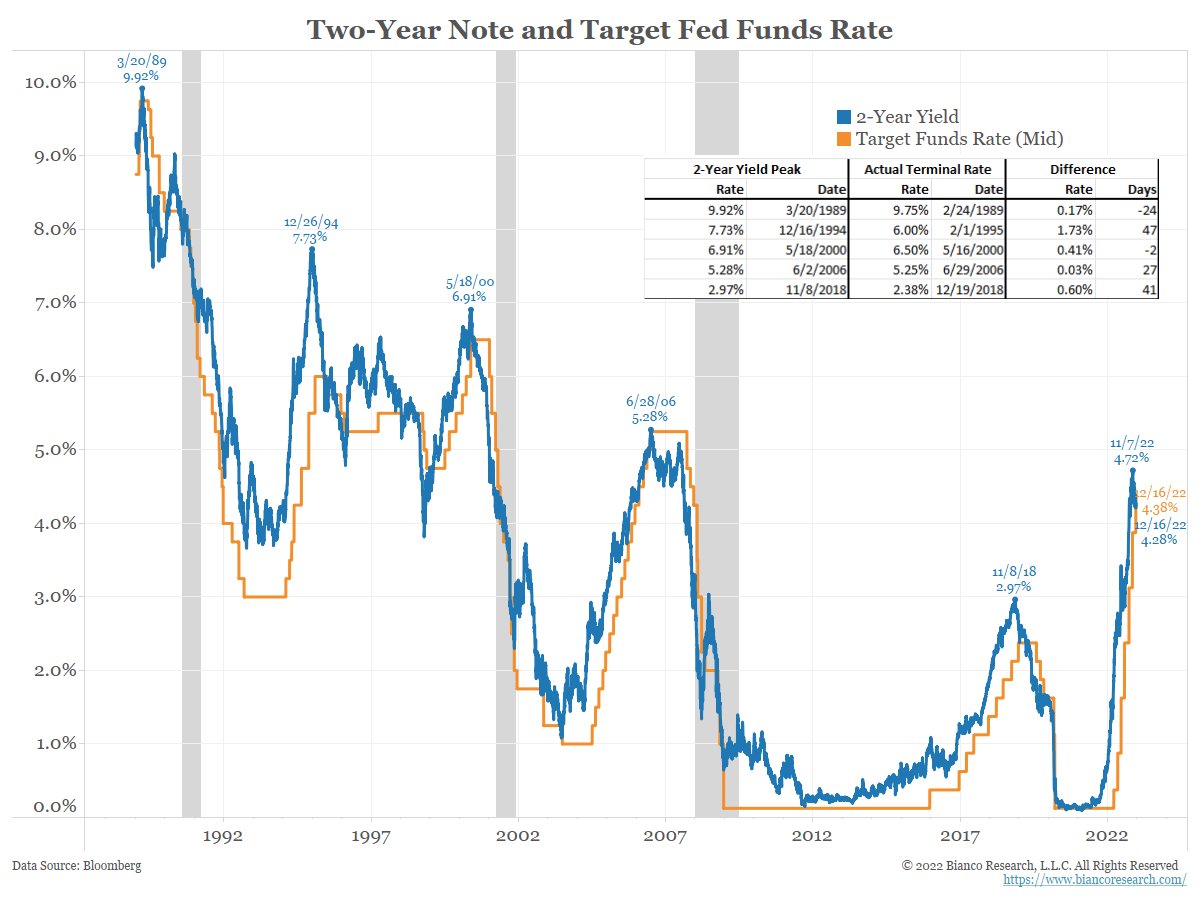

Short rates, the 2-year yield did not peak at 4.72% on Nov 7.

Rate hike cycles ended with the 2-year yield ABOVE the terminal (peak) funds rate.

If the Fed goes to 5% - 5.25%, history says the 2-year yield peaks above the terminal rate or at least 5.25%.

Short rates, the 2-year yield did not peak at 4.72% on Nov 7.

Rate hike cycles ended with the 2-year yield ABOVE the terminal (peak) funds rate.

If the Fed goes to 5% - 5.25%, history says the 2-year yield peaks above the terminal rate or at least 5.25%.

14/22

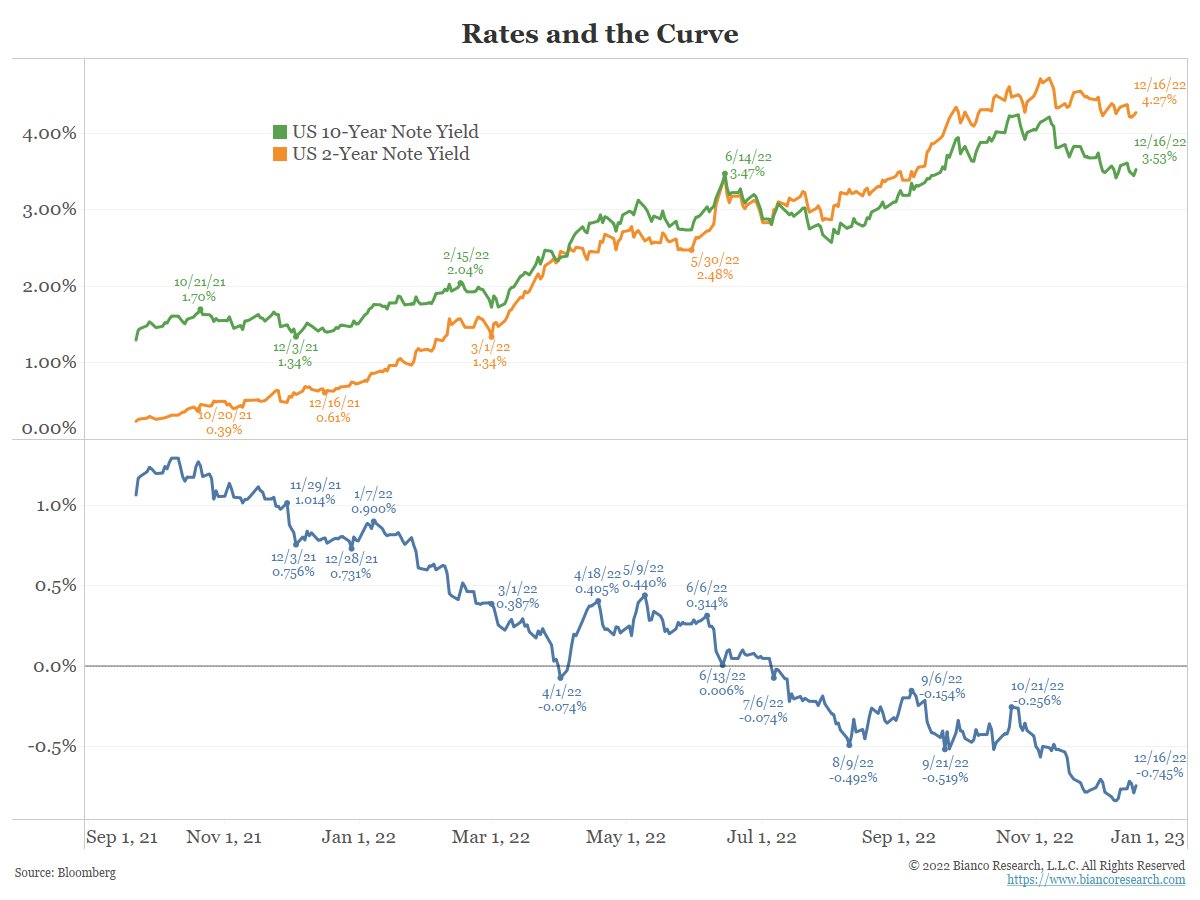

How about long rates (10-year yield)?

If the economy is not falling apart, the curve inversion will stall.

This should drag the 10-year yield higher (green). The curve (blue), already at a 41-year extreme, should stay within -100 bps if it even gets that extreme.

How about long rates (10-year yield)?

If the economy is not falling apart, the curve inversion will stall.

This should drag the 10-year yield higher (green). The curve (blue), already at a 41-year extreme, should stay within -100 bps if it even gets that extreme.

15/22

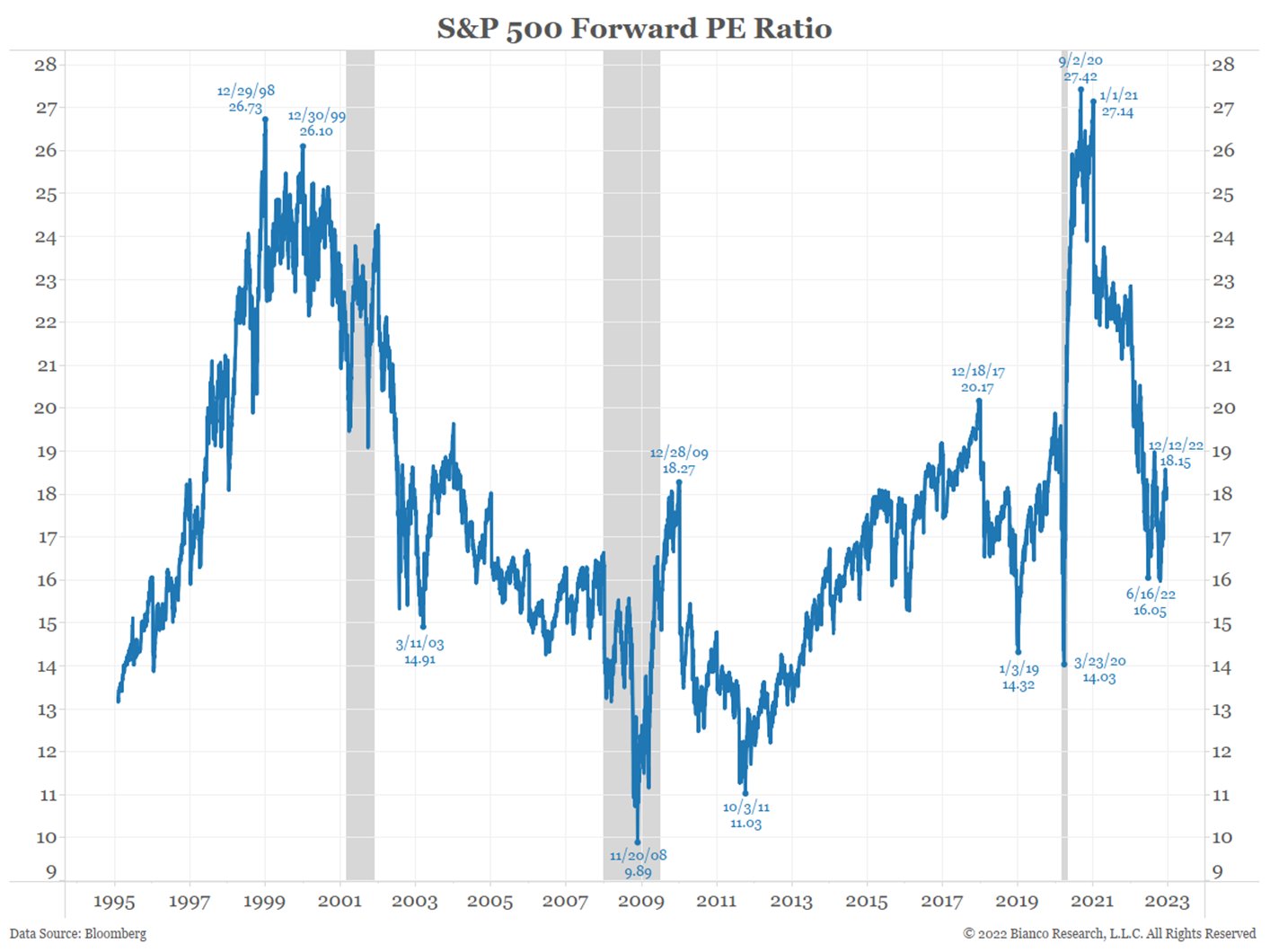

So, rates have yet to peak.

How about stocks?

If rates are going higher, then the discount rates used in valuation are also going higher.

Then paying over 18x for next year's earnings with higher discount rates looks awfully expensive.

So, rates have yet to peak.

How about stocks?

If rates are going higher, then the discount rates used in valuation are also going higher.

Then paying over 18x for next year's earnings with higher discount rates looks awfully expensive.

17/22

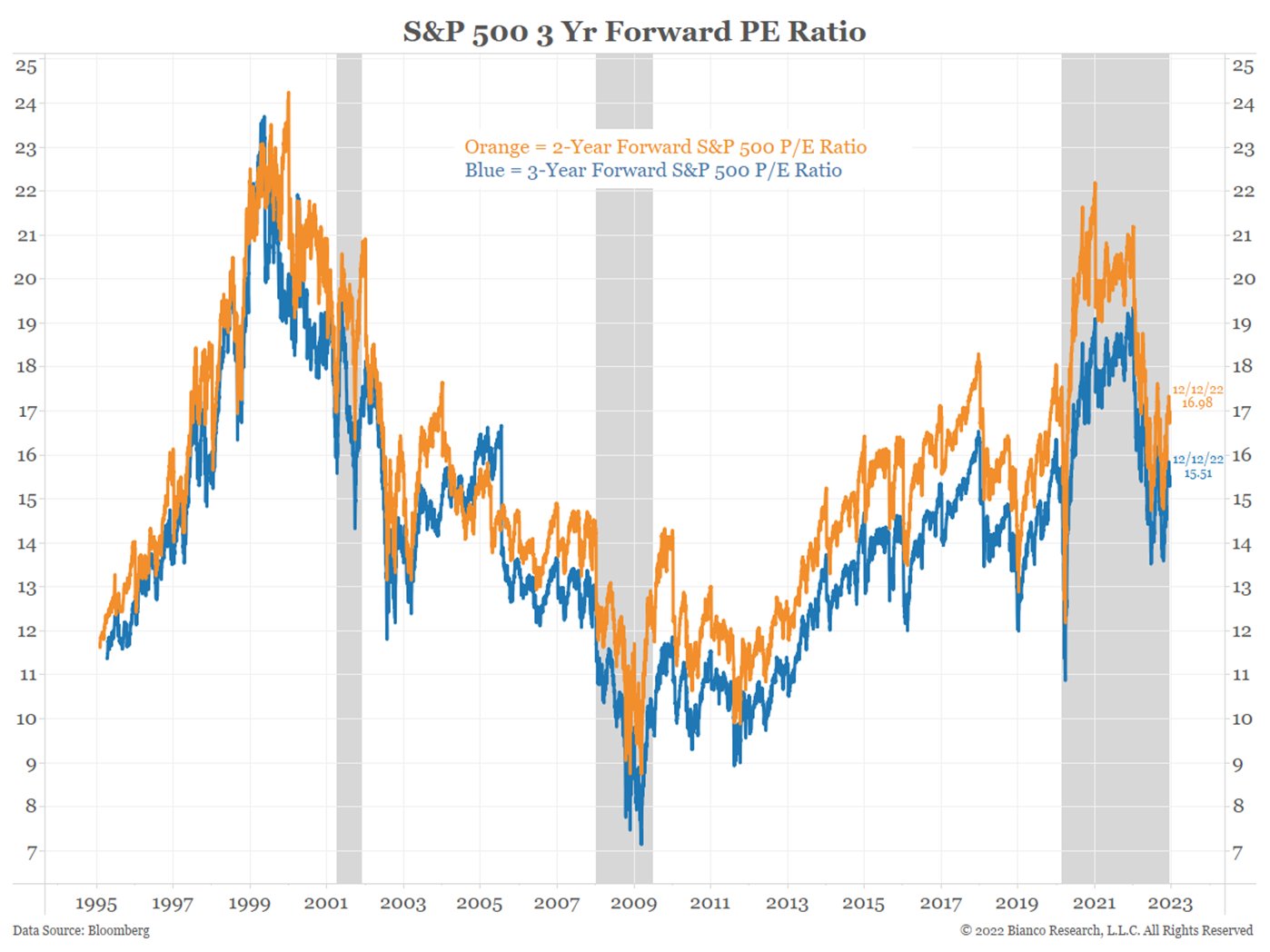

Not to mention paying almost 17x for 2-year out earnings or >15x for 3-year out earnings.

This is very expensive UNLESS discount rates start falling because inflation is returning to 2% forever. Not so as a reaction to heading into a recession.

Not to mention paying almost 17x for 2-year out earnings or >15x for 3-year out earnings.

This is very expensive UNLESS discount rates start falling because inflation is returning to 2% forever. Not so as a reaction to heading into a recession.

18/22

So here we are in 2022.

Use all your skill to pick good stocks and hope they lose money and fire people, aka a recession.

Then you will be rewarded with higher stock prices as the Fed pivots.

So here we are in 2022.

Use all your skill to pick good stocks and hope they lose money and fire people, aka a recession.

Then you will be rewarded with higher stock prices as the Fed pivots.

19/22

Because if your stocks perform by delivering earnings and have to hire more people, and God forbid ... see enough demand for their product that they have to RAISE prices, your reward is another wipeout in stock prices as the Fed never pivots.

Because if your stocks perform by delivering earnings and have to hire more people, and God forbid ... see enough demand for their product that they have to RAISE prices, your reward is another wipeout in stock prices as the Fed never pivots.

20/22

This is what 15 years of QE, negative interest rates, forward guidance, and Fed puts have done. The market is all about liquidity. It is a junkie for liquidity. It is all that matters.

This is what 15 years of QE, negative interest rates, forward guidance, and Fed puts have done. The market is all about liquidity. It is a junkie for liquidity. It is all that matters.

21/22

Or what was the most successful investing style between 2009 and 2021?

Buy broad-based equity ETFs and whine that the Fed is not doing enough to make you rich. Not only did everyone think this, most still believe this!

Or what was the most successful investing style between 2009 and 2021?

Buy broad-based equity ETFs and whine that the Fed is not doing enough to make you rich. Not only did everyone think this, most still believe this!

22/22

This idea that the economy weakens, the Fed pivots, and markets soar works with inflation of ~2% forever (09 to 21).

But if inflation is >2% forward, the worst thing that can happen is the economy weakens enough for the Fed to pivot.

www.zerohedge.com/markets/ignore-cpi-and-fomc-why-michael-wilson-sees-bloodbath-ahead-rerun-2008

This idea that the economy weakens, the Fed pivots, and markets soar works with inflation of ~2% forever (09 to 21).

But if inflation is >2% forward, the worst thing that can happen is the economy weakens enough for the Fed to pivot.

www.zerohedge.com/markets/ignore-cpi-and-fomc-why-michael-wilson-sees-bloodbath-ahead-rerun-2008