Thread by Julien Bittel, CFA

- Tweet

- Mar 17, 2023

- #CentralBank #Finance #Economics

Thread

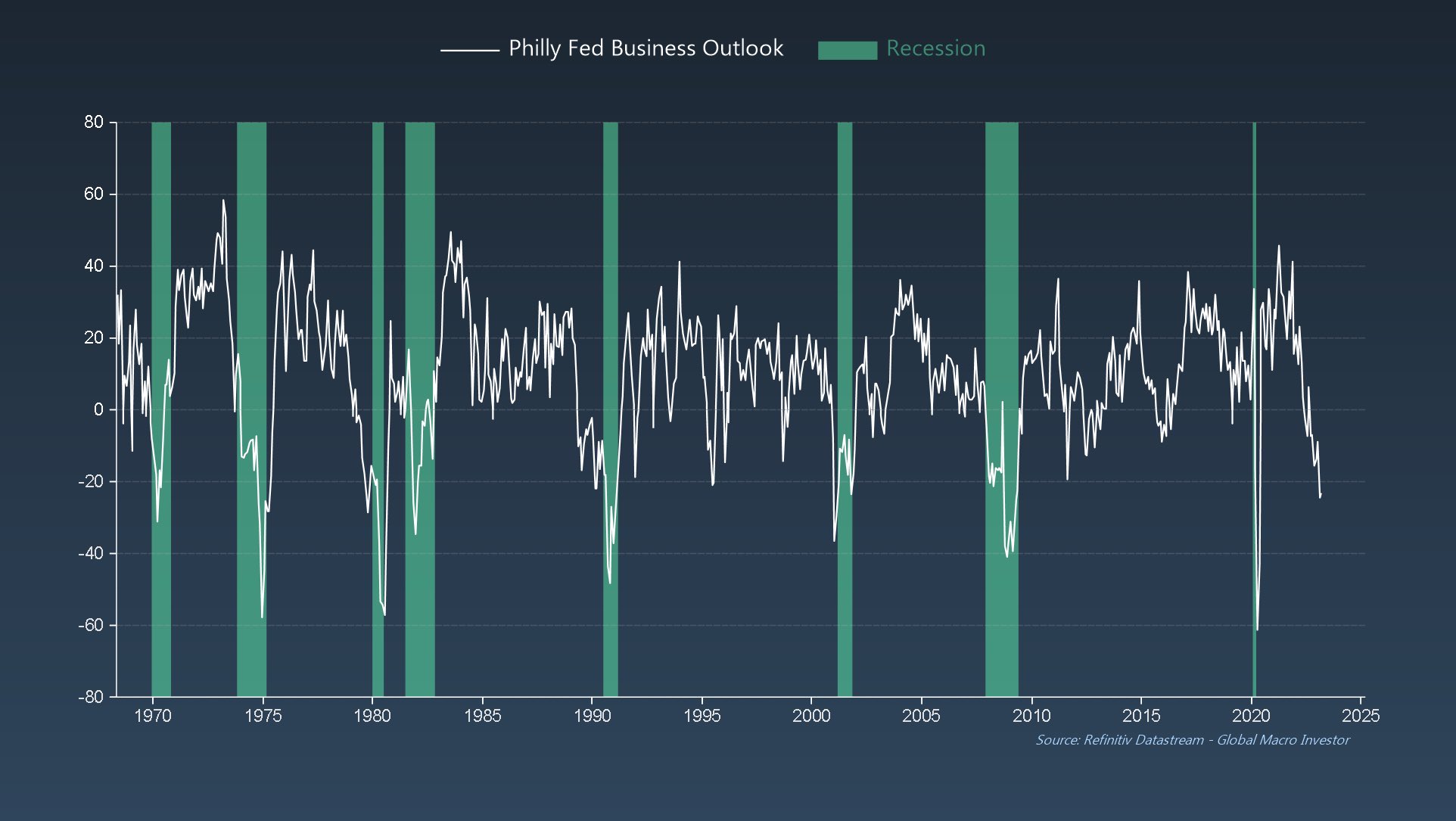

Bears really coming out of the woodwork on March Philly Fed data…

I think it’s the wrong take.

A lot of people are using the 1970s as the period most similar to today…

Some are using 2000 or 2008…

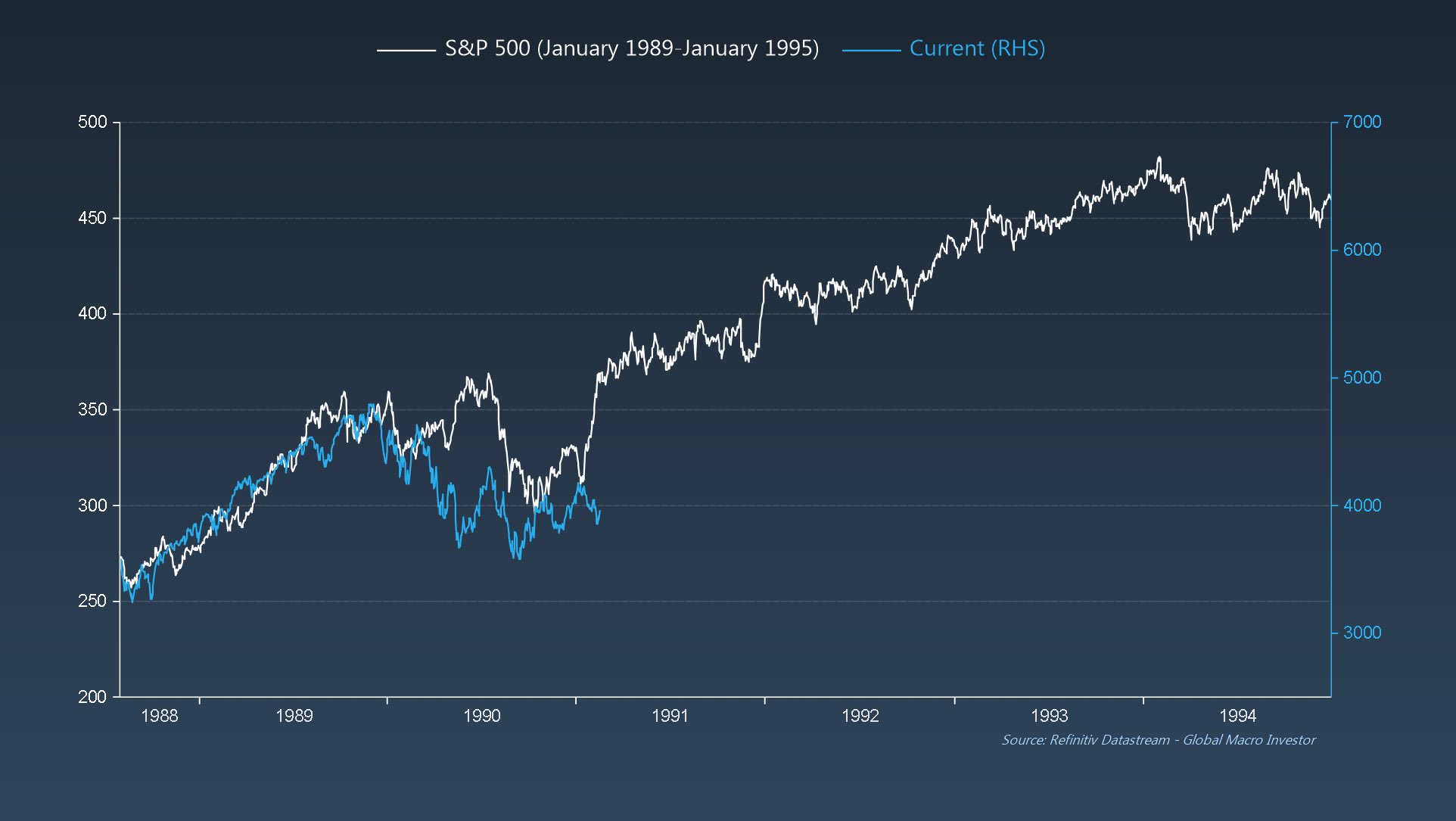

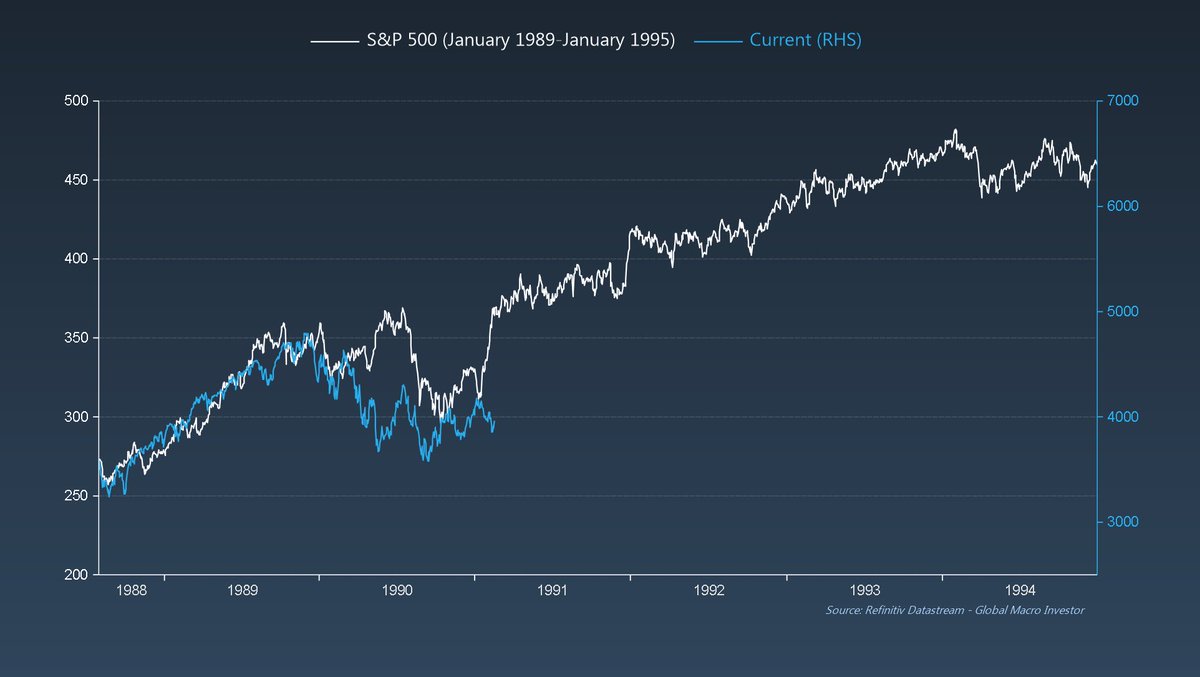

We’re using 1990.

It’s a near perfect fit. Let me show you…

A thread 🧵

I think it’s the wrong take.

A lot of people are using the 1970s as the period most similar to today…

Some are using 2000 or 2008…

We’re using 1990.

It’s a near perfect fit. Let me show you…

A thread 🧵

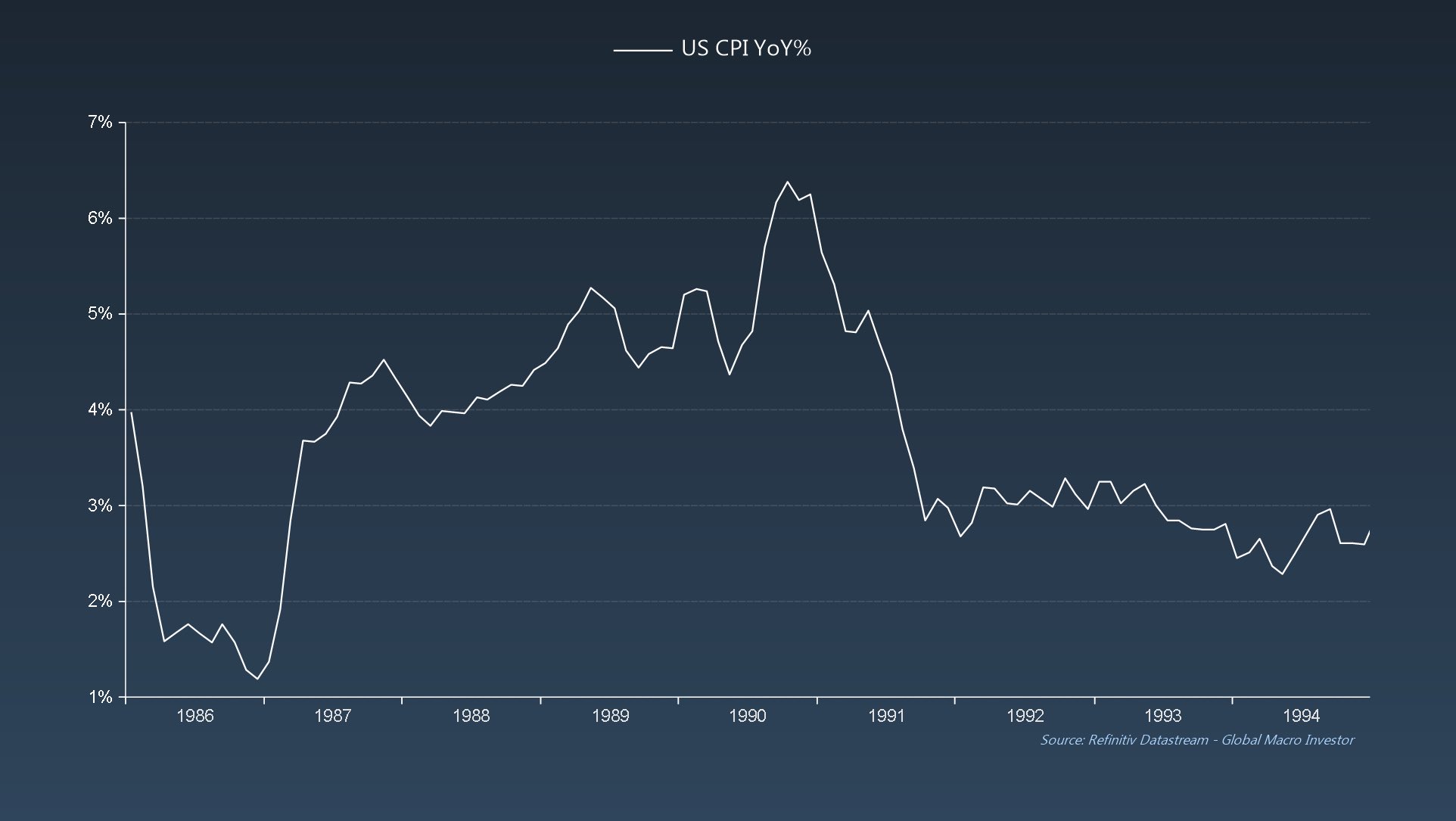

Back in 1990, CPI rose to 6.4% year-on-year (near ten year highs at the time), igniting fears that the 1970s were returning with a vengeance…

Sound familiar?

Sound familiar?

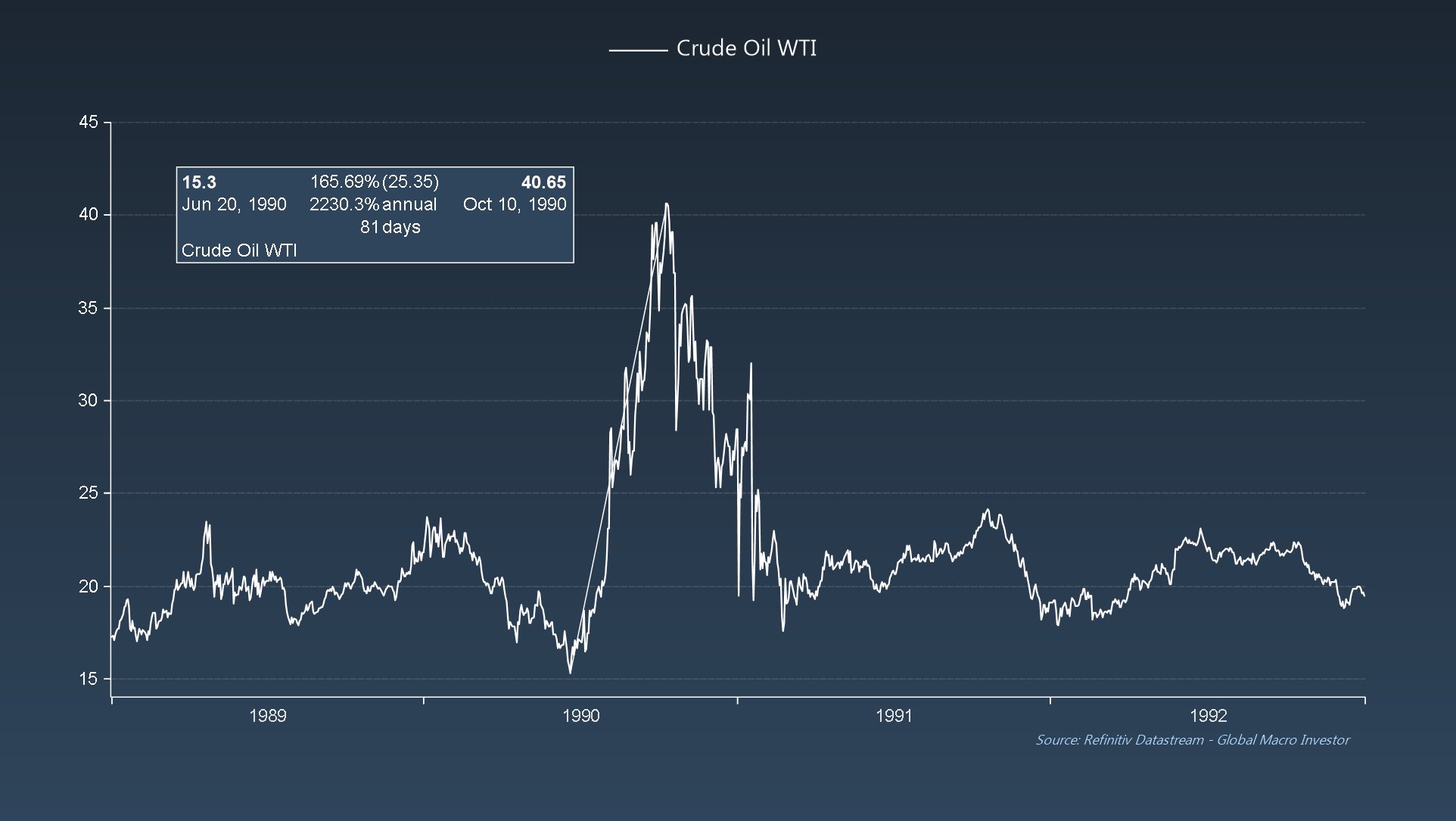

This was driven by a massive 166% spike in oil prices in response to the invasion of Kuwait by Iraq, with the subsequent embargo by the UN of Iraqi oil knocking out two of the world’s largest oil producers.

This resulted in a worldwide energy crisis…

This resulted in a worldwide energy crisis…

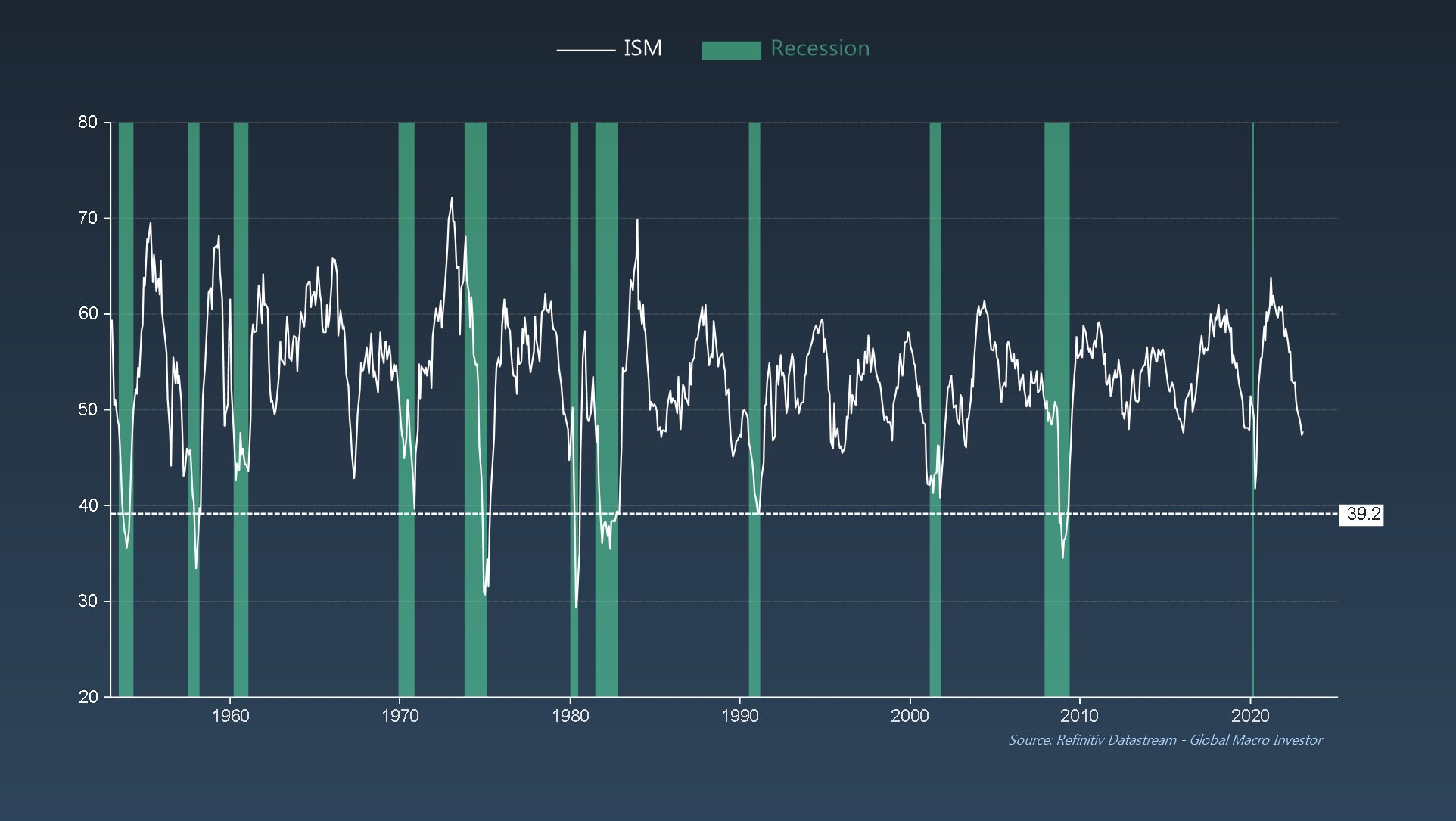

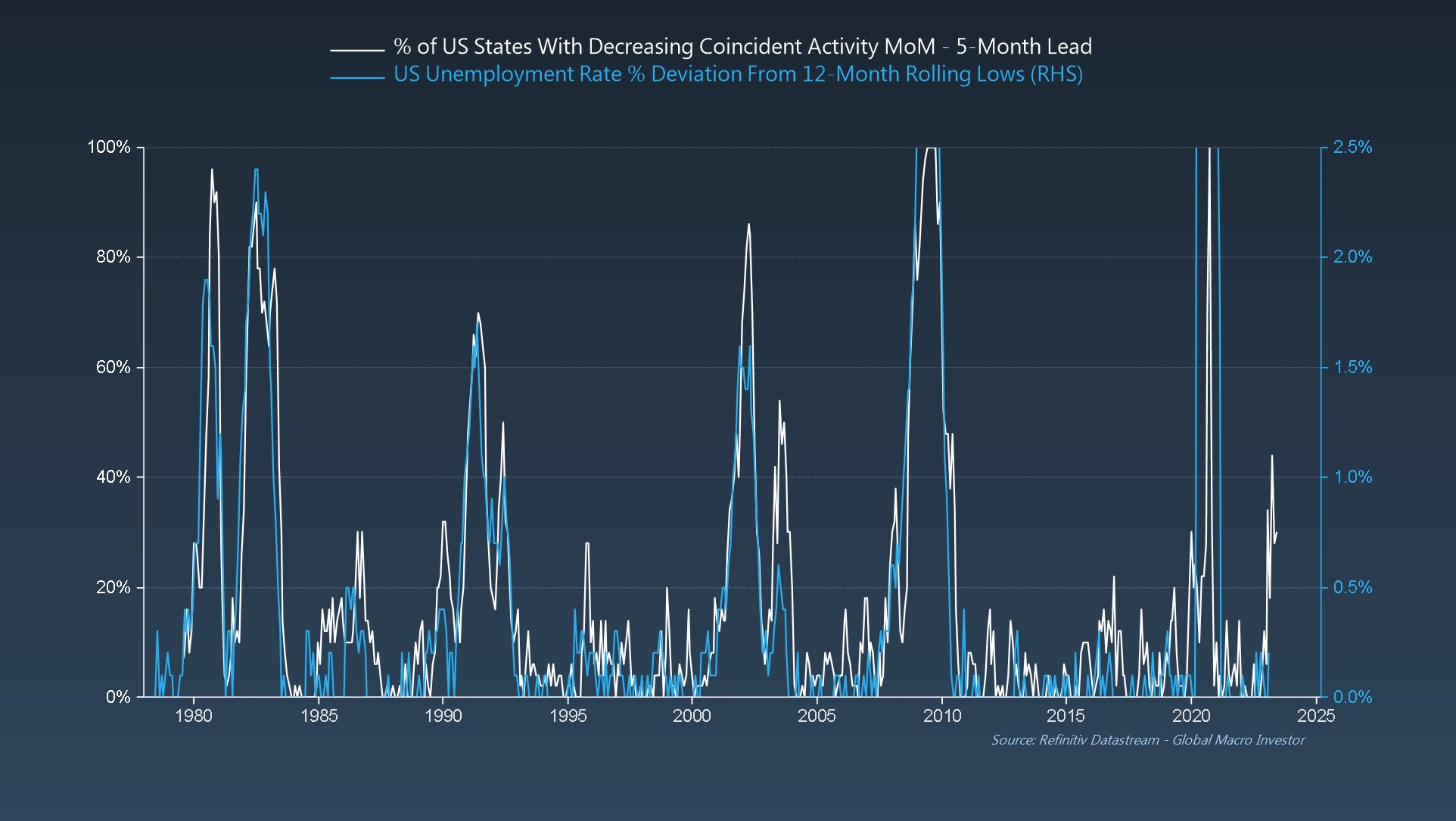

The Fed hiked rates from 5.75% to 10% to slay the inflation dragon which triggered a growth collapse and the ISM fell to 39.2 - 100% recession territory going back to the early 1950s…

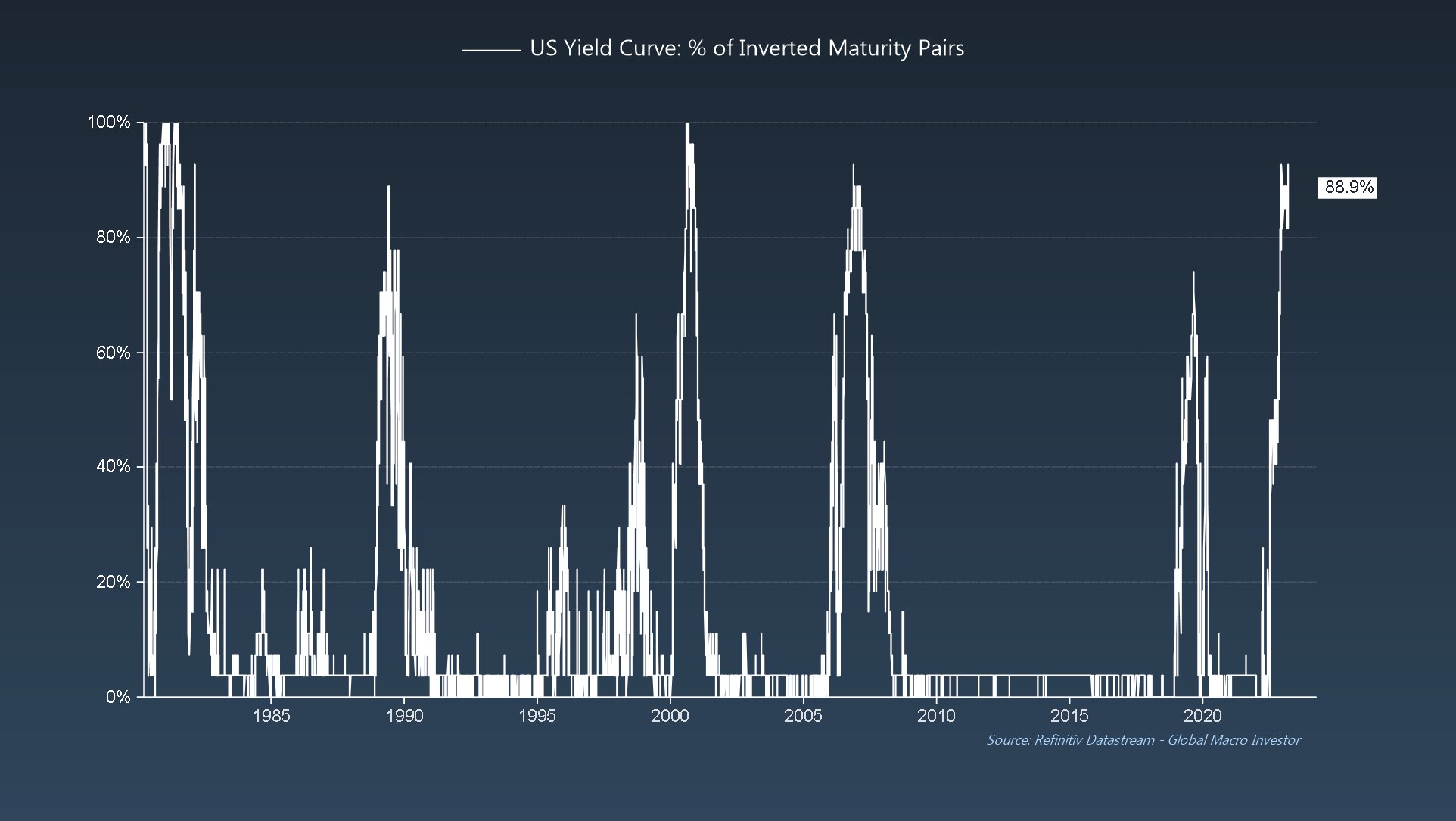

Additionally, just like today, nearly 90% of the yield curve was inverted...

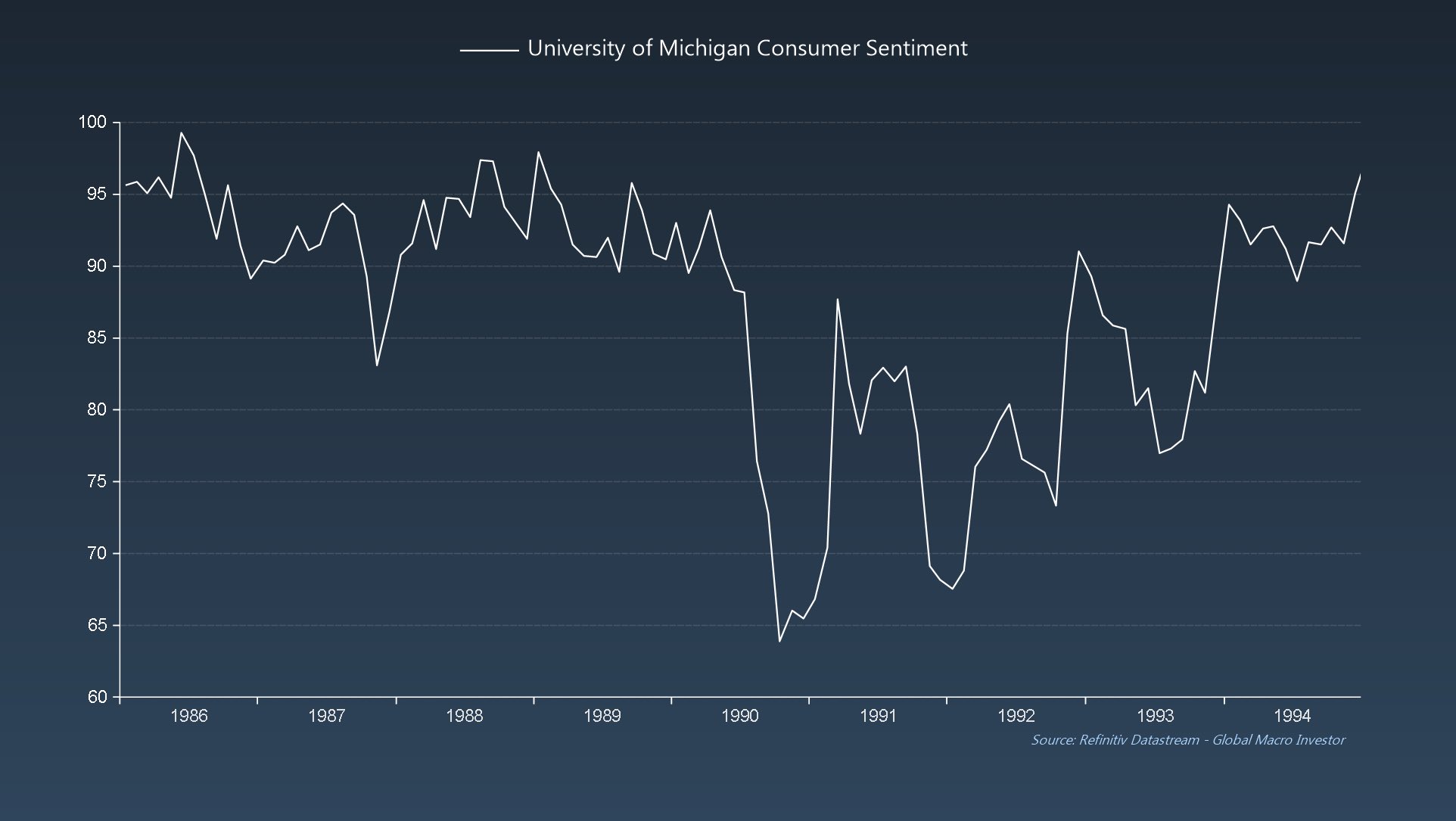

Consumer sentiment imploded - war, inflation and Fed hikes killed it…

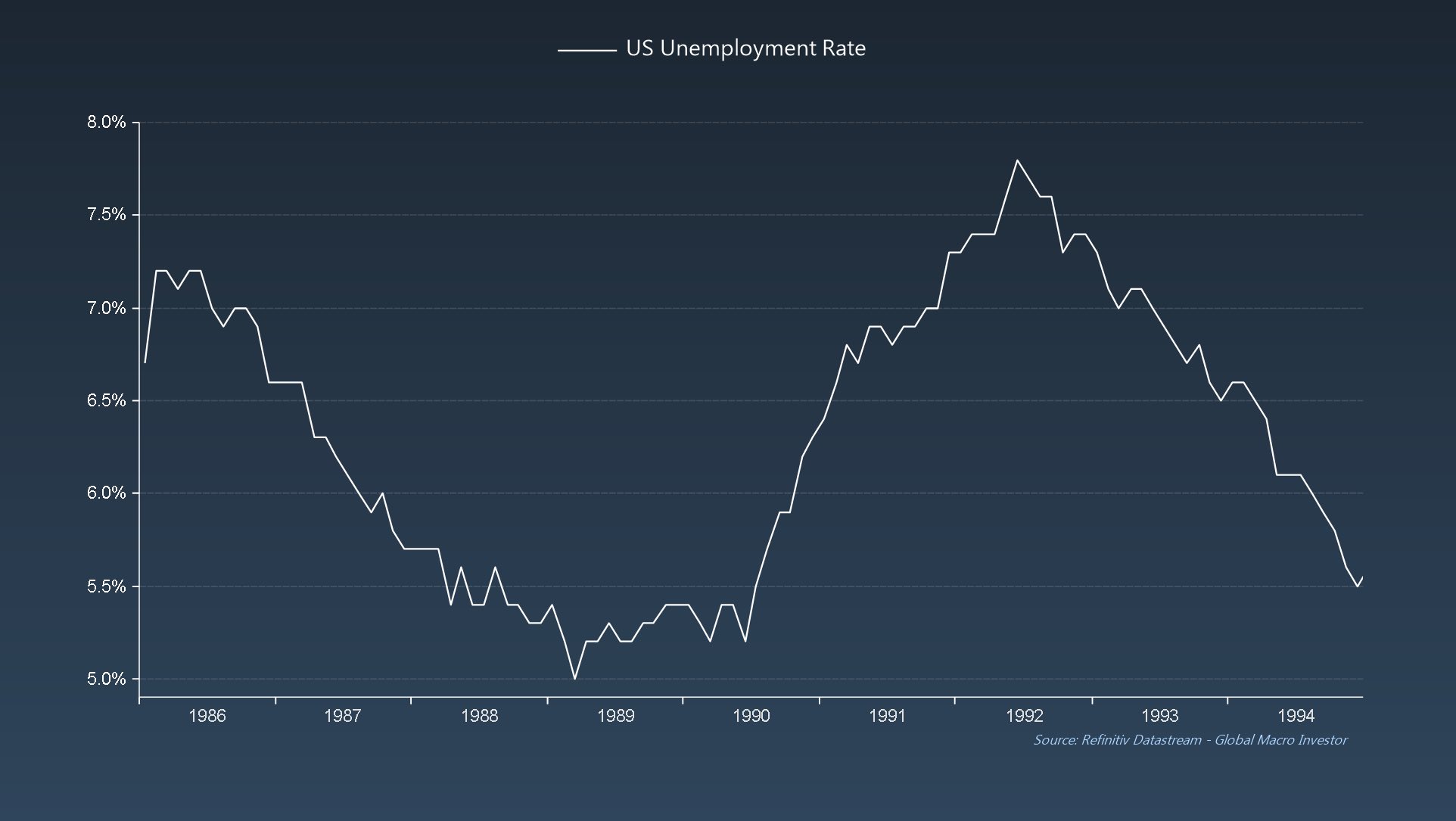

Unemployment rose from 5% to 7.8%…

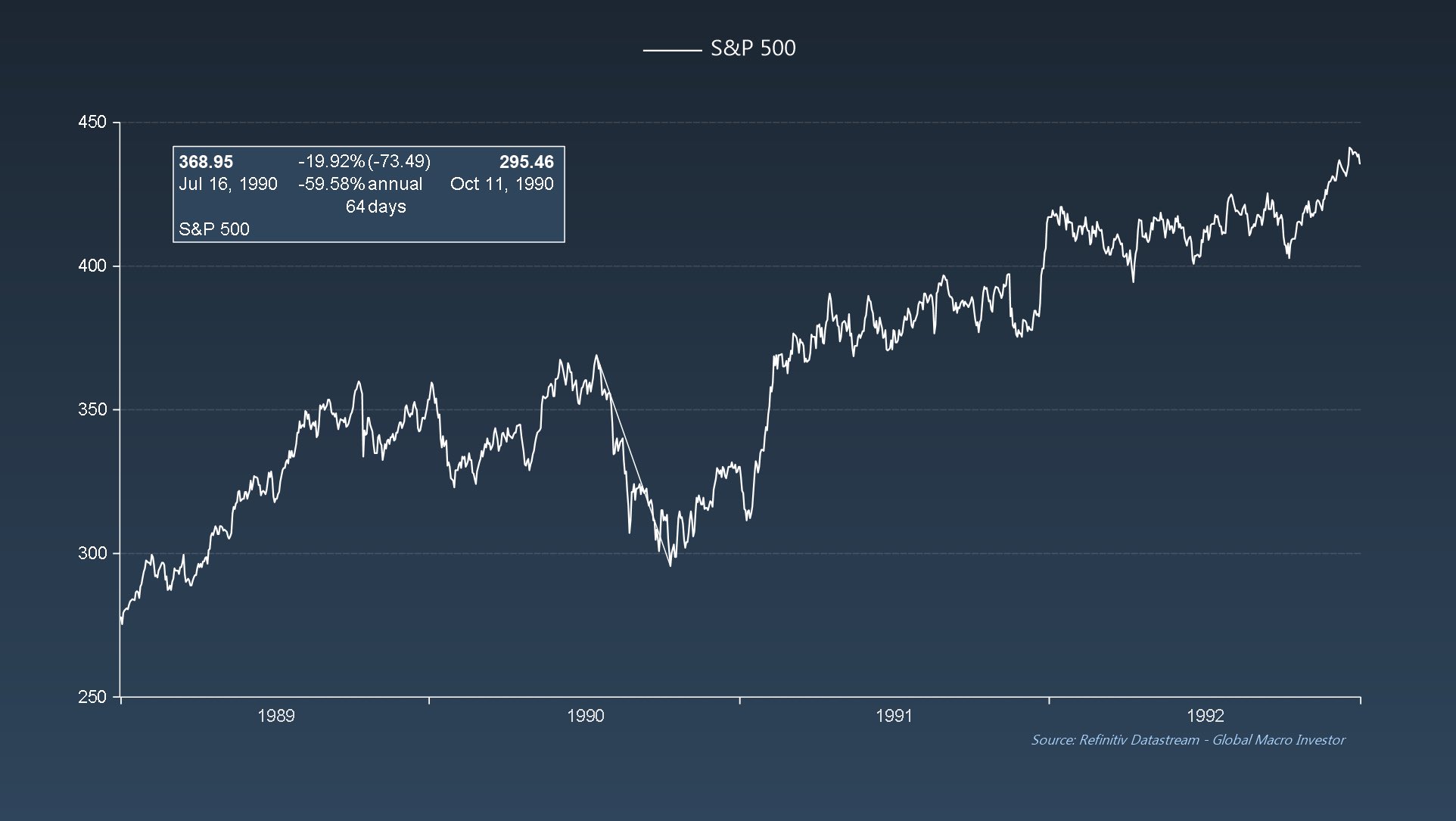

And yet, the S&P 500 only fell by 20%…

But wait, there’s more!

But wait, there’s more!

Bearish sentiment hit exactly the same level as October 2022: 59%…

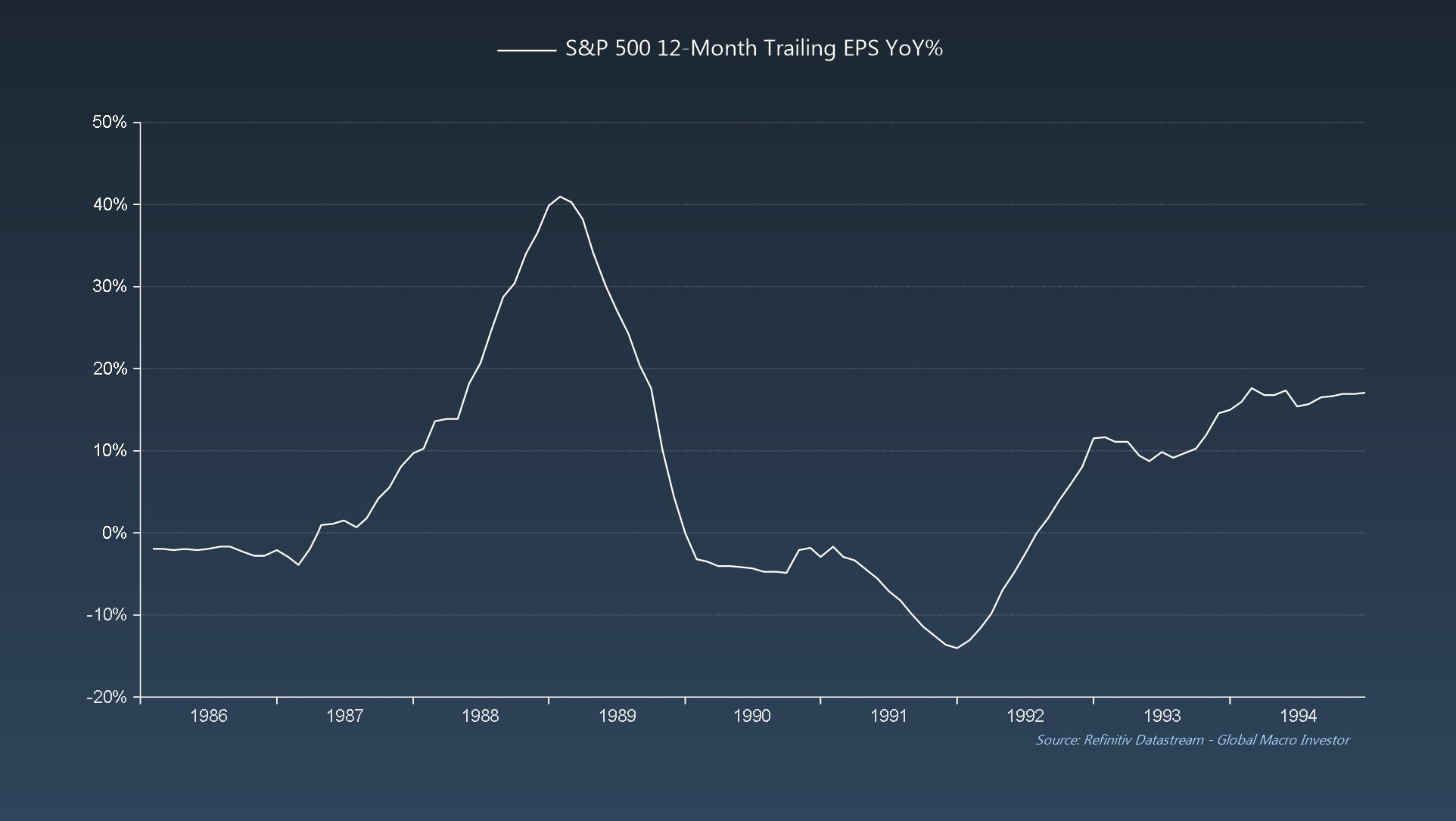

We had a deep and protracted two year earnings recession…

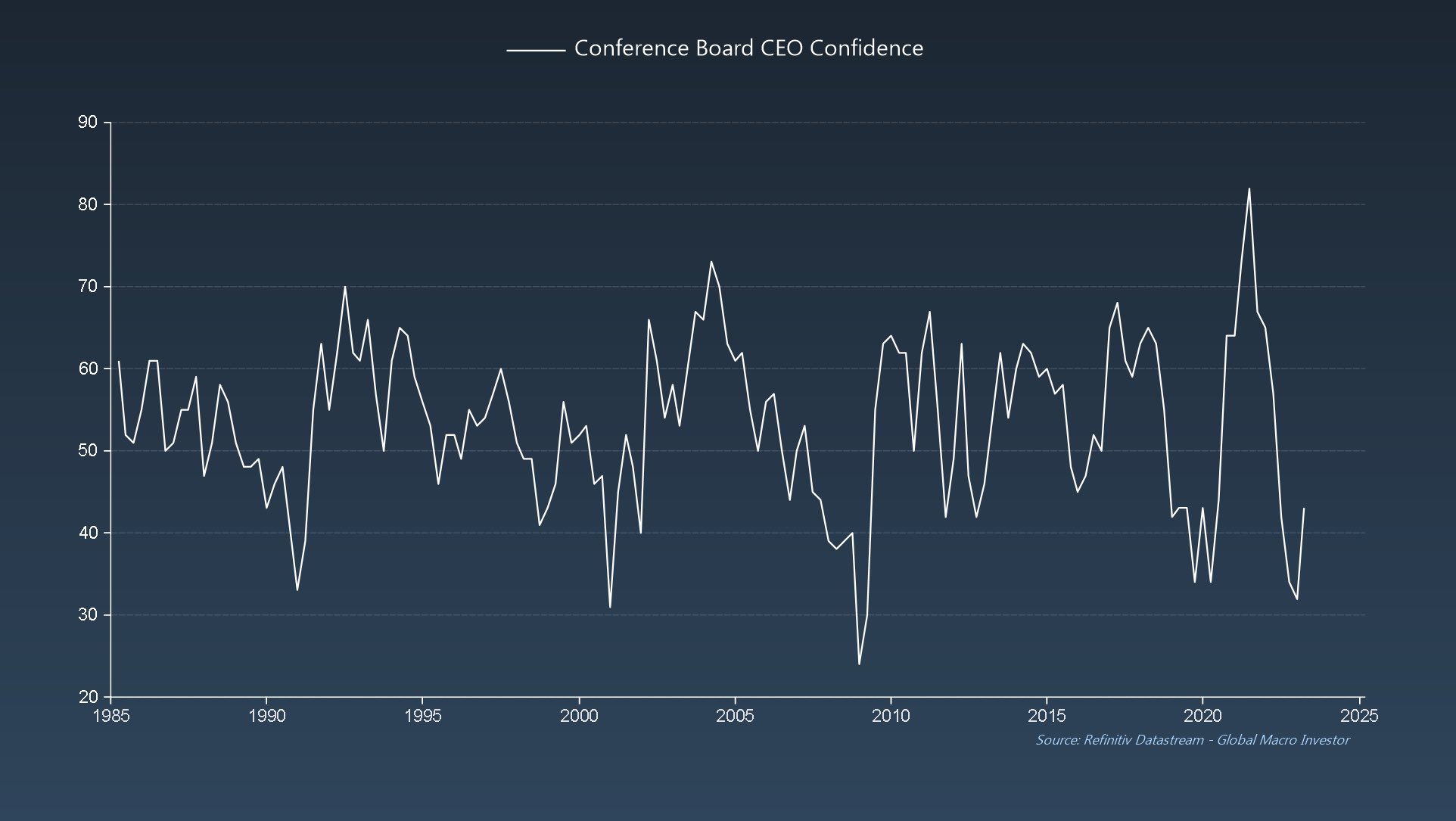

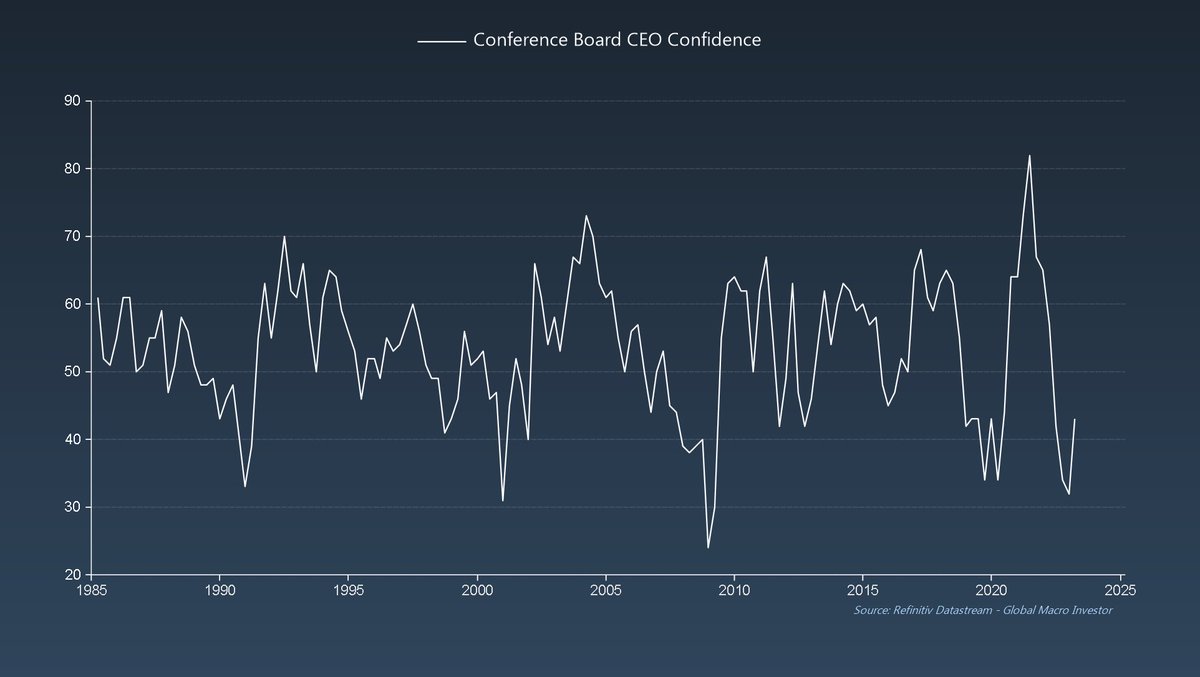

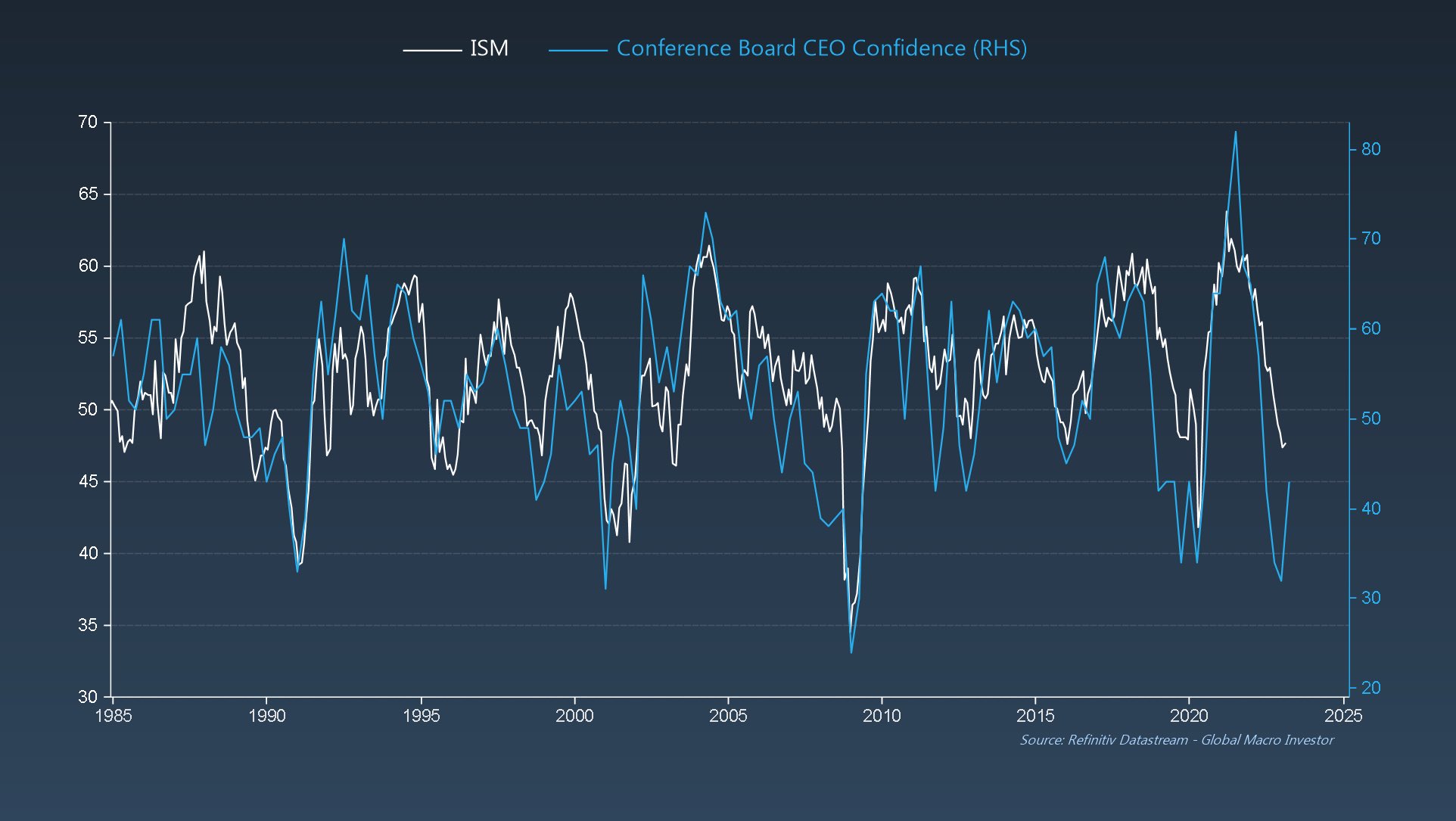

And CEO confidence fell to nearly exactly the same levels as today…

Though, what’s important here is to be forward looking.

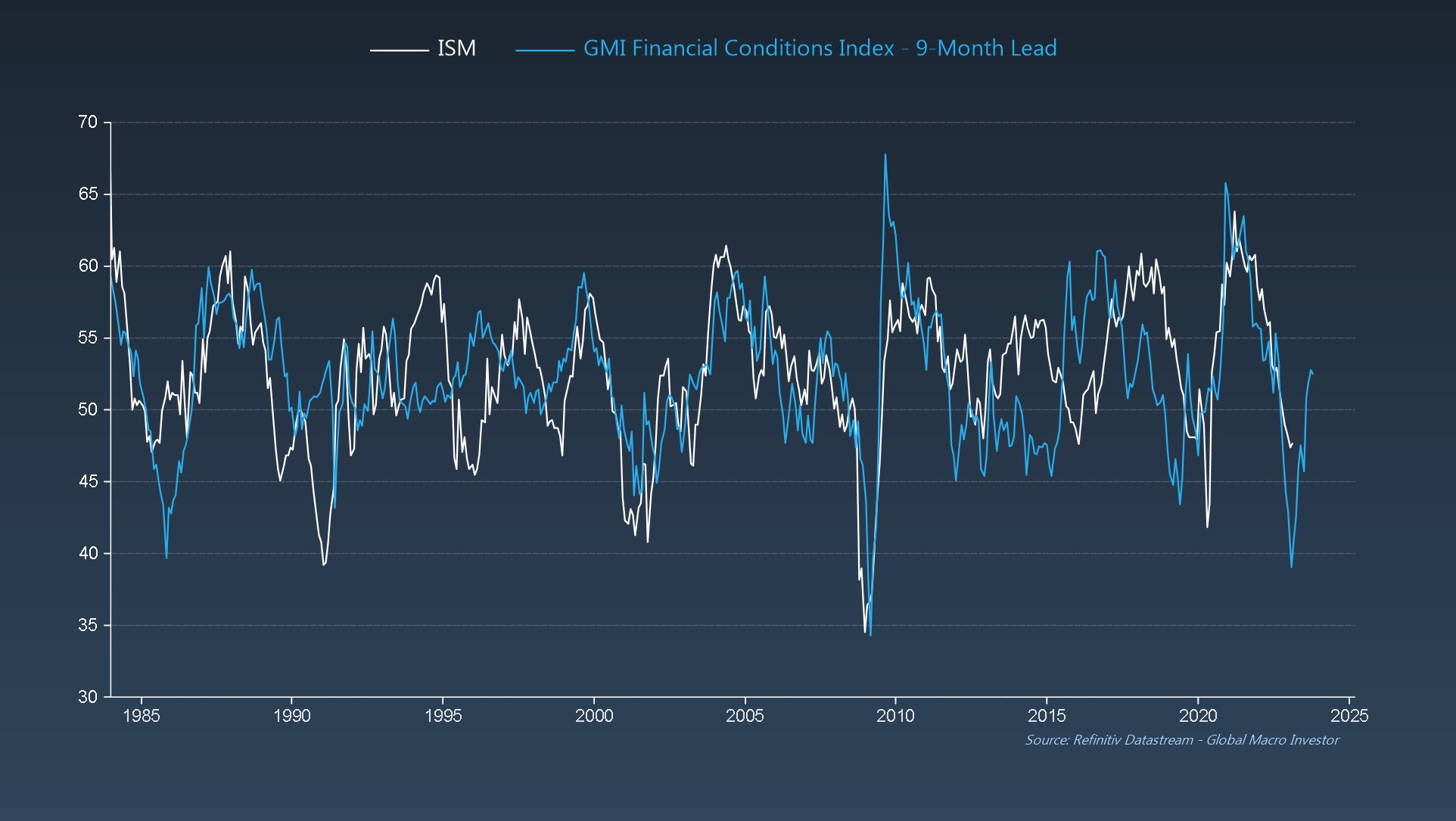

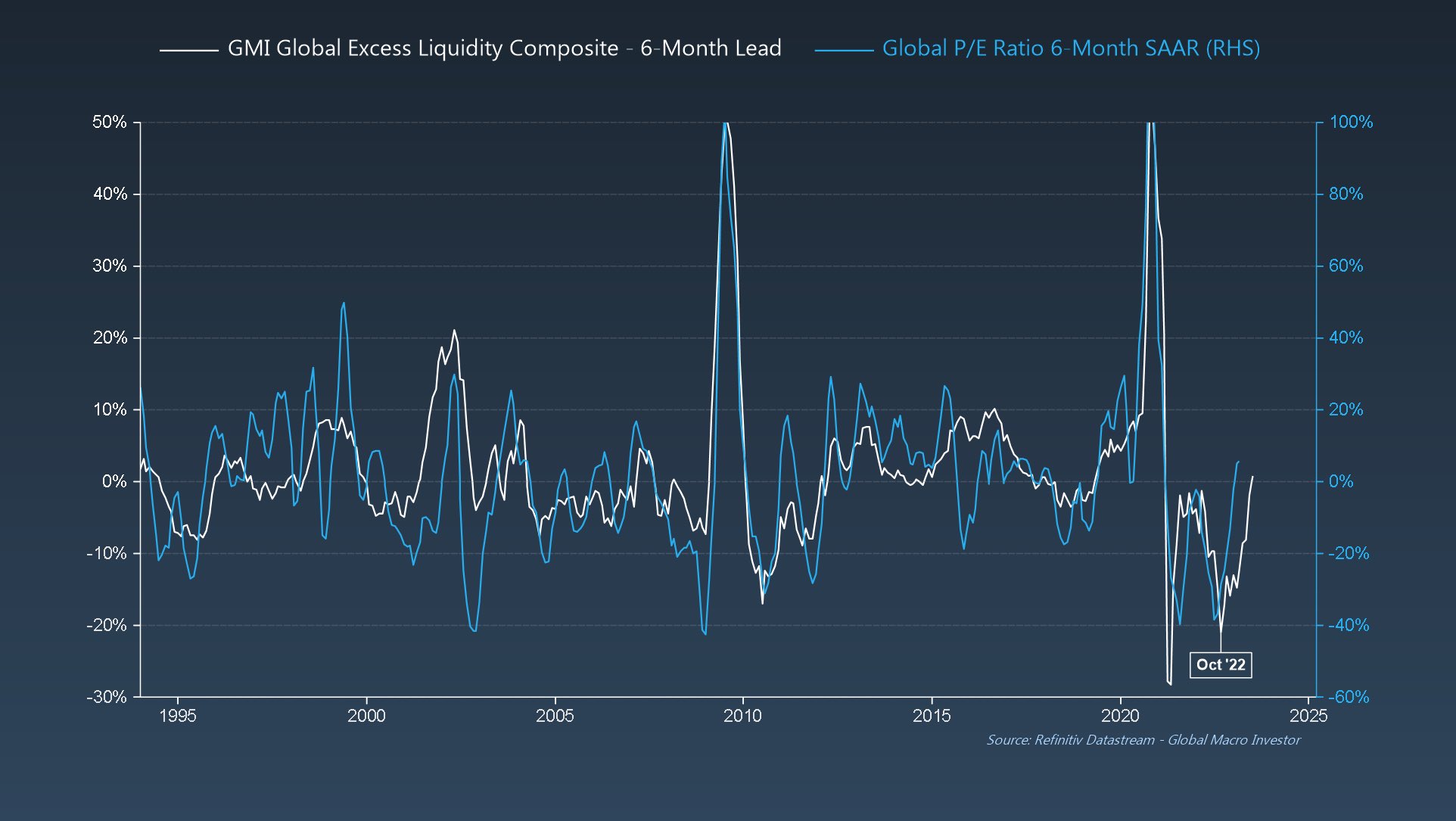

Our GMI Financial Conditions Index continues to suggest that the lows for ISM are now in sight…

Our GMI Financial Conditions Index continues to suggest that the lows for ISM are now in sight…

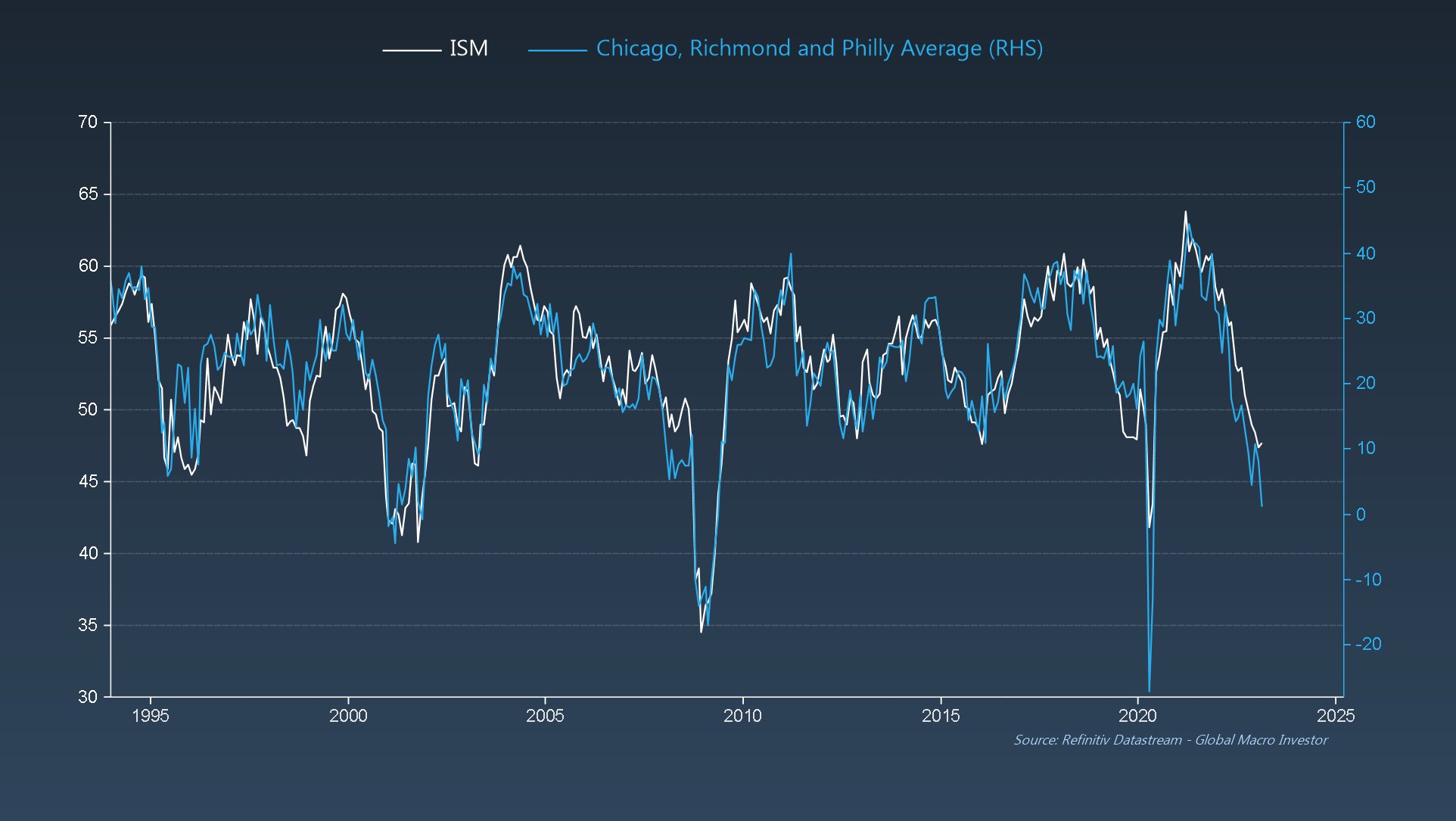

Sure, the ISM can still take a final dip lower based on recent Chicago, Philly and Richmond PMI data, say down to around 40…

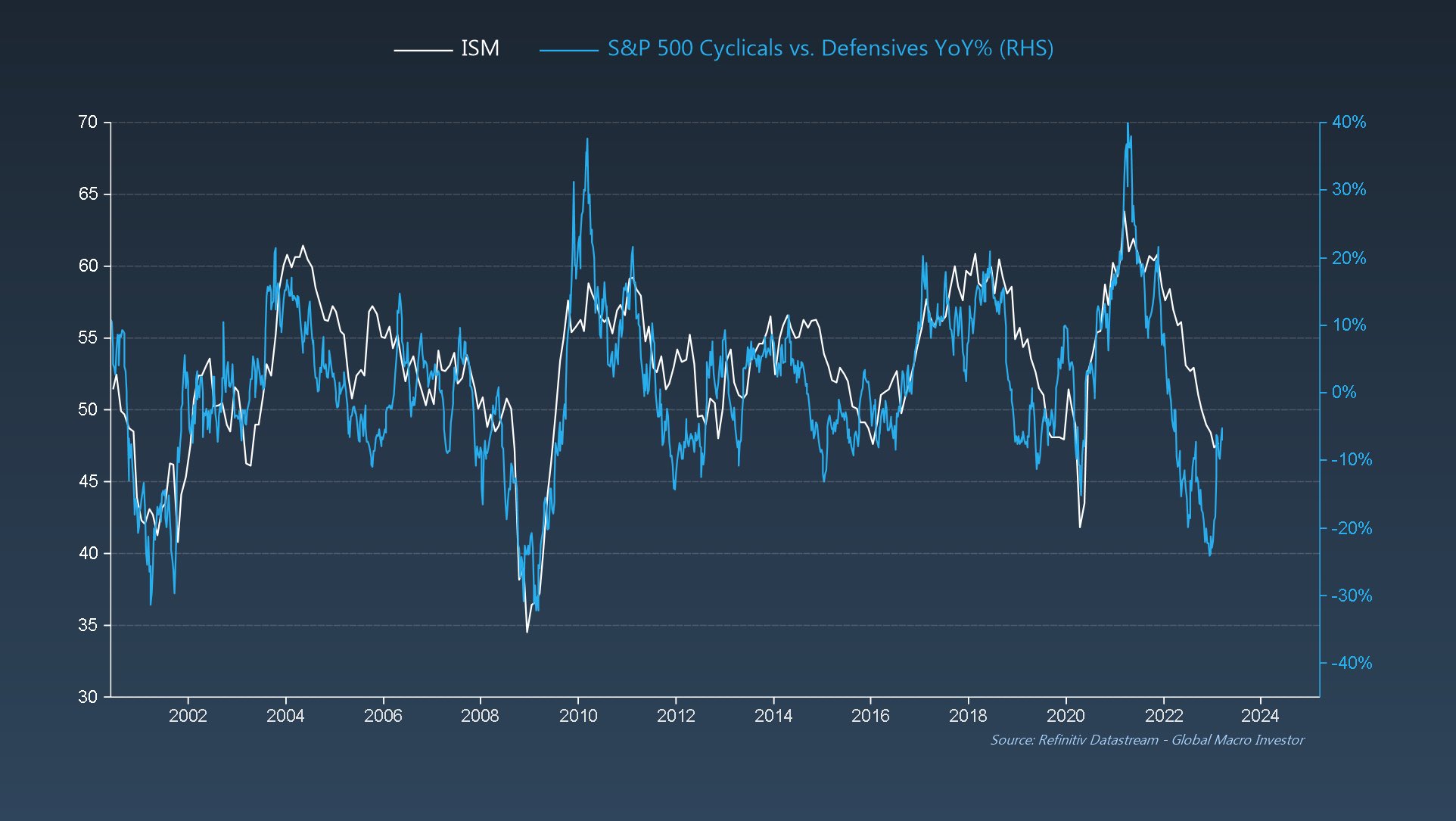

But crucially ISM New Orders Less Inventories is starting to rise again…

… and as previously shown, CEO Confidence has already bottomed, and the ISM is never far behind…

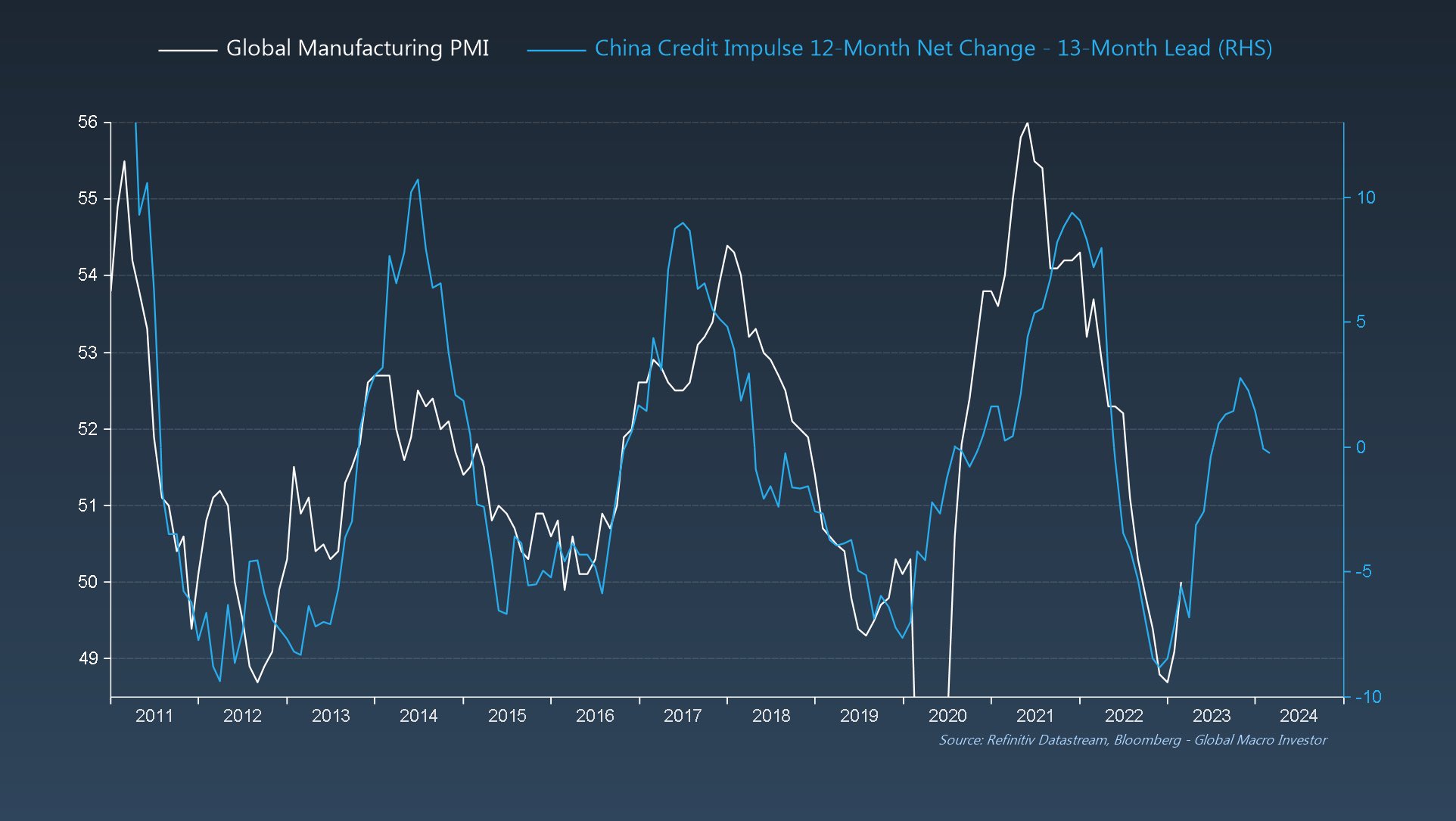

Additionally, similar to previous boom/bust cycles since 2008, China is driving the global growth cycle higher…

Also, remember ISM of 40? Already priced in…

Yes, unemployment is going to rise…

But, just like during the 1990 recession, the Fed will respond by cutting rates again, aggressively…

Remember, the Fed is not focused on lead indicators…

They’re focused on their mandate: employment and inflation, both of which are extremely lagging…

Remember, the Fed is not focused on lead indicators…

They’re focused on their mandate: employment and inflation, both of which are extremely lagging…

Unemployment lags the ISM by six months and will now start to rise…

(here inverted)

(here inverted)

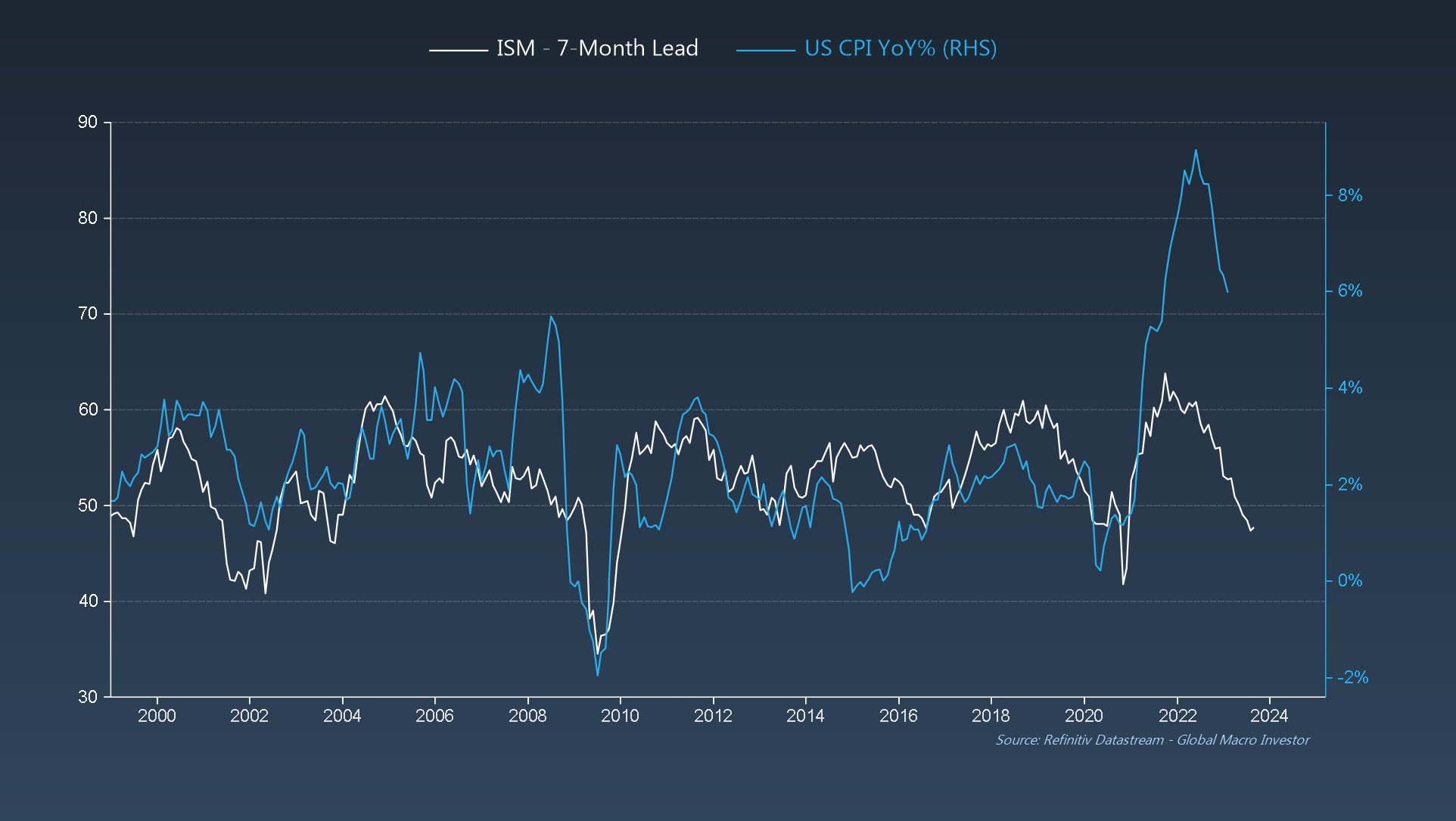

… and CPI lags the ISM by seven months and will continue to fall…

To conclude, today looks a lot like the 1990 recession:

War, a massive spike in commodity prices, hot inflation, Fed hiking, inverted yield curve, growth collapse, rising unemployment, extreme bearish sentiment and a ~20% drop in SPX.

It’s also a pretty good fit contextually…

War, a massive spike in commodity prices, hot inflation, Fed hiking, inverted yield curve, growth collapse, rising unemployment, extreme bearish sentiment and a ~20% drop in SPX.

It’s also a pretty good fit contextually…

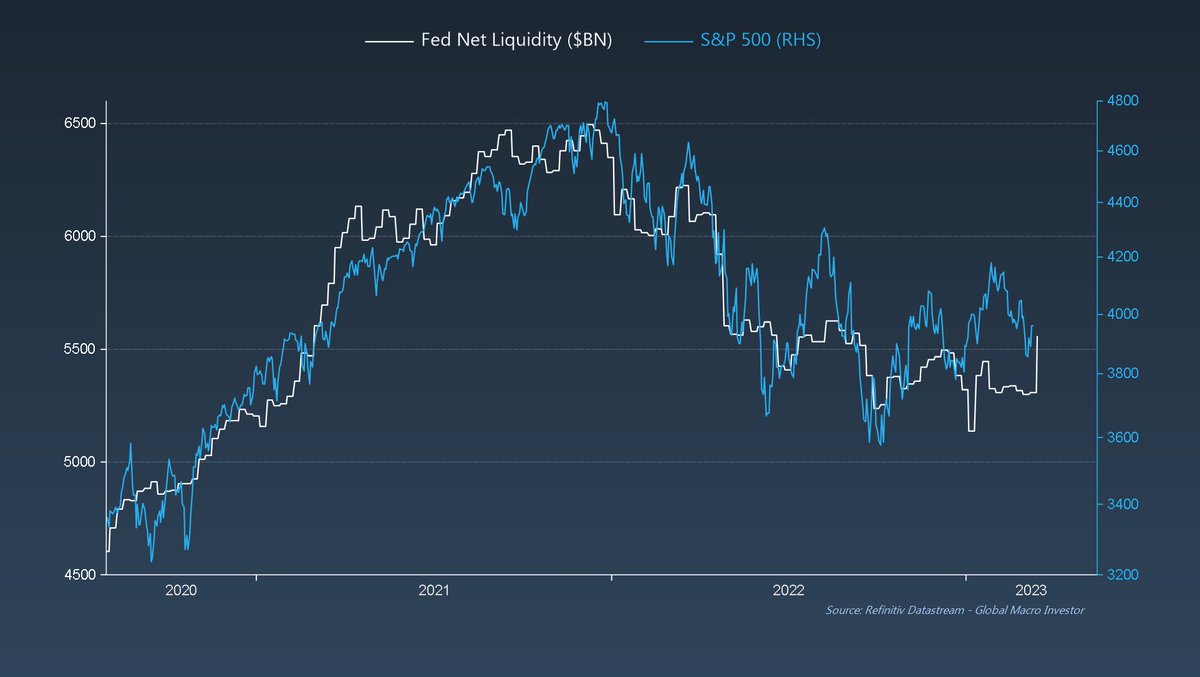

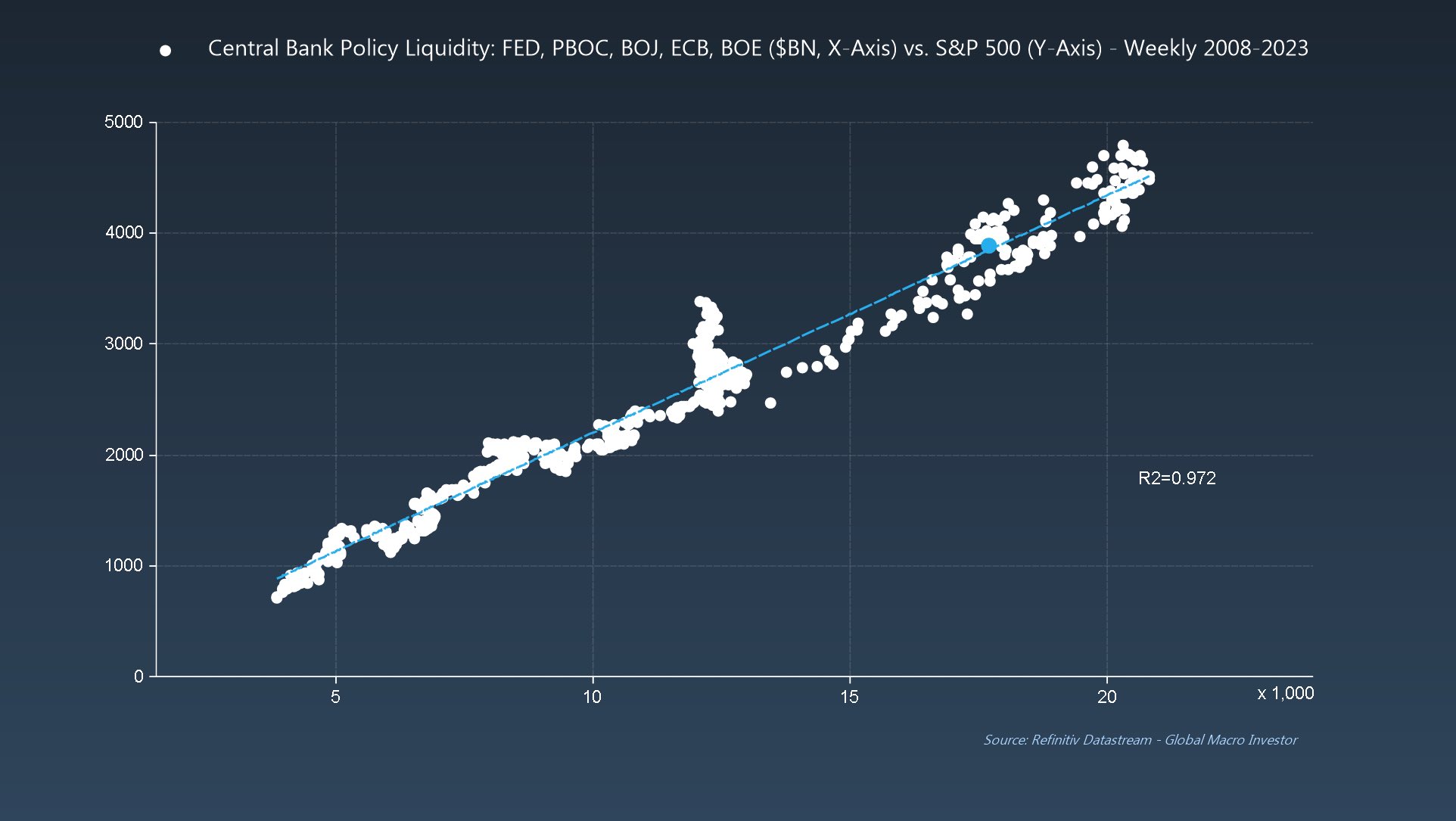

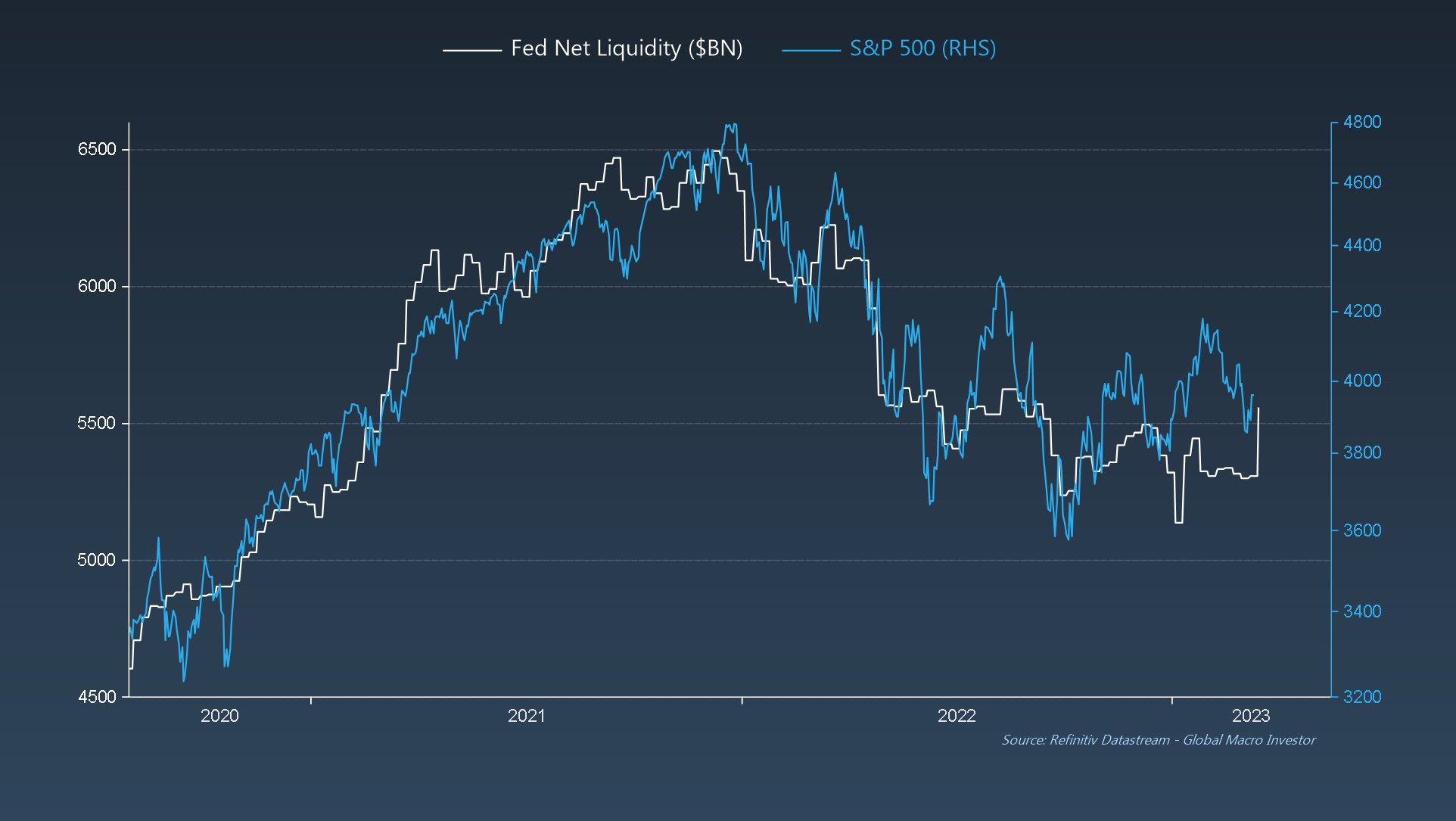

What’s been driving our more bullish take on equities since October is that we had been seeing liquidity turning higher and this has been a key driver behind the equity re-rating story so far this year…

Liquidity is extremely important for equities which are back to trading at fair value versus global liquidity conditions.

Prior to the sell-off, we had been trading at around an 8% premium but the gap has now closed…

Prior to the sell-off, we had been trading at around an 8% premium but the gap has now closed…

Obviously the next few weeks will be very important. Contagion risks are real and deflation risks are growing despite the sticky inflation crowd being louder than ever…

Equities may get a bit nervous about all of this, but the cowbell is coming.

In fact, it’s already started…

Equities may get a bit nervous about all of this, but the cowbell is coming.

In fact, it’s already started…