Thread

Wow, just recorded one of most revealing interviews of my life with the ultimate expert on interest rate hedging (issue at heart of bank turmoil).

He said hedges at many U.S. banks were nowhere close to offsetting unrealized losses on securities (incl.some big banks)

A thread.

He said hedges at many U.S. banks were nowhere close to offsetting unrealized losses on securities (incl.some big banks)

A thread.

DISCLAIMER: DO NOT MAKE ANY DEPOSIT DECISION ON THE BASIS OF THIS THREAD. FOR INFORMATION PURPOSES ONLY.

My personal opinion is that banking system will be fine and since Monday I've viewed many bank stocks as bargains (will explain later why).

But back to hedging... (2/22)

My personal opinion is that banking system will be fine and since Monday I've viewed many bank stocks as bargains (will explain later why).

But back to hedging... (2/22)

First, a bit about my guest. He pioneered the use of swaptions to manage convexity risk in mortgage portfolios in the 1990s.

And he was directly in charge of hedging Freddie Mac's >$500 Billion mortgage book pre-GFC.

So yes, he knows what he's talking about.

(3/22)

And he was directly in charge of hedging Freddie Mac's >$500 Billion mortgage book pre-GFC.

So yes, he knows what he's talking about.

(3/22)

Now that we've gotten that out of the way, let's get to business.

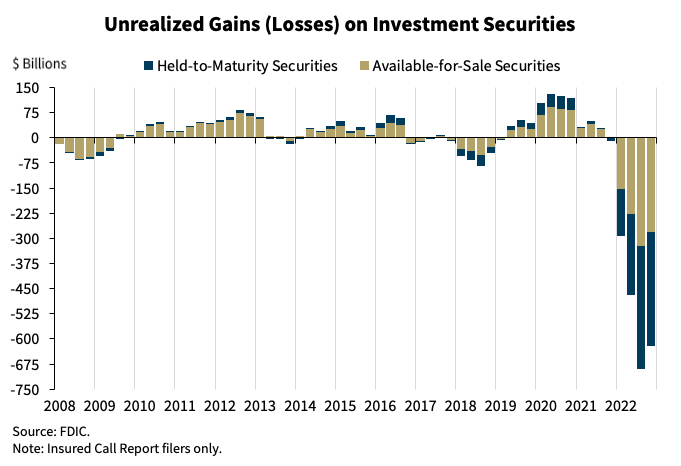

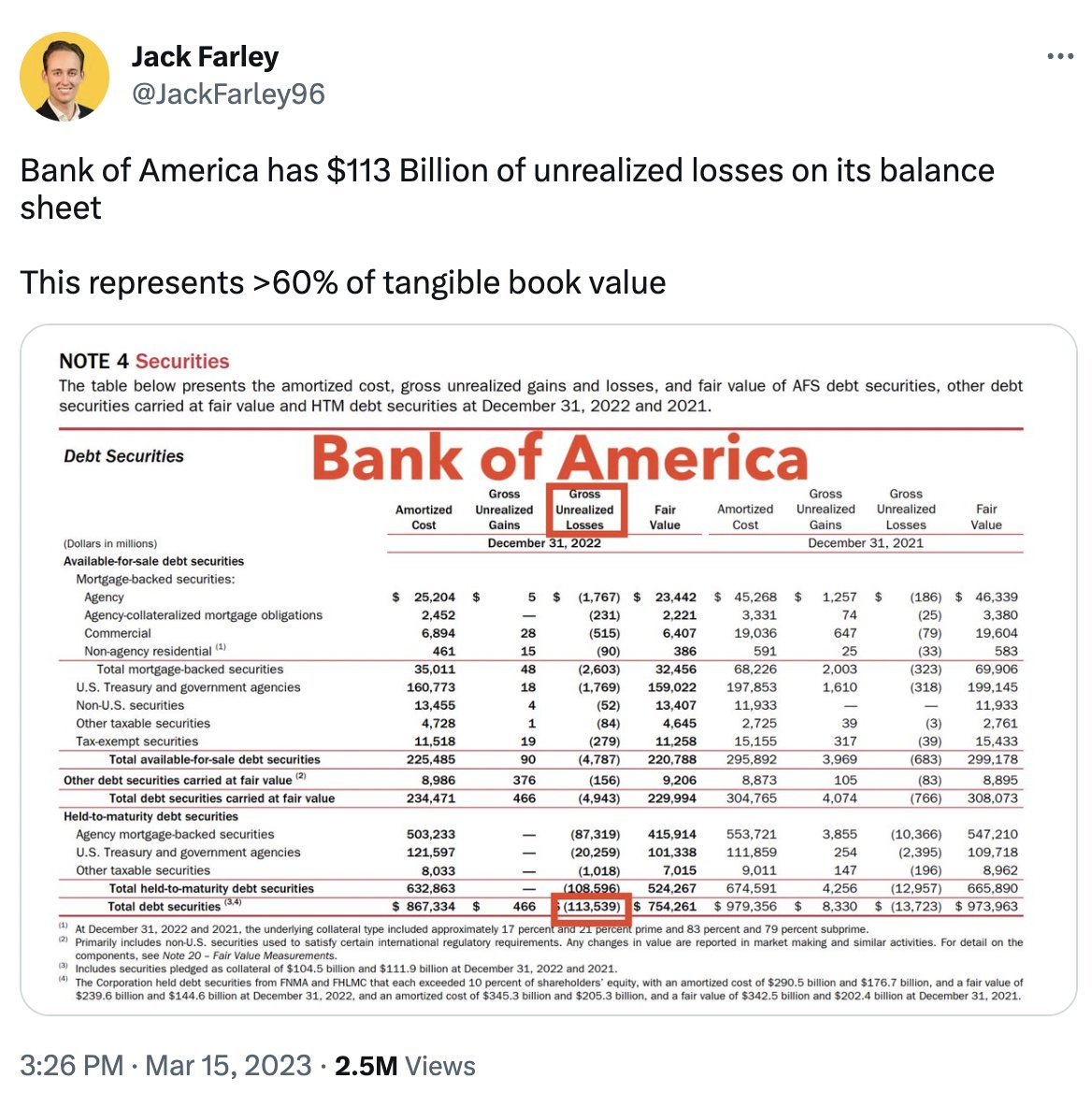

You may've seen this chart showing unrealized losses of U.S. banks on investment securities totals over half a trillion dollars.

This is due almost entirely to INTEREST RATE RISK not credit risk (as in 2008).

You may've seen this chart showing unrealized losses of U.S. banks on investment securities totals over half a trillion dollars.

This is due almost entirely to INTEREST RATE RISK not credit risk (as in 2008).

You may have heard people say "oh but don't worry about it, the banks have hedged that risk out."

My guest strongly disagreed this claim. He said that only a very small fraction of the unrealized losses on bank balance sheets that occurred in 2022 (as rates rose) were hedged.

My guest strongly disagreed this claim. He said that only a very small fraction of the unrealized losses on bank balance sheets that occurred in 2022 (as rates rose) were hedged.

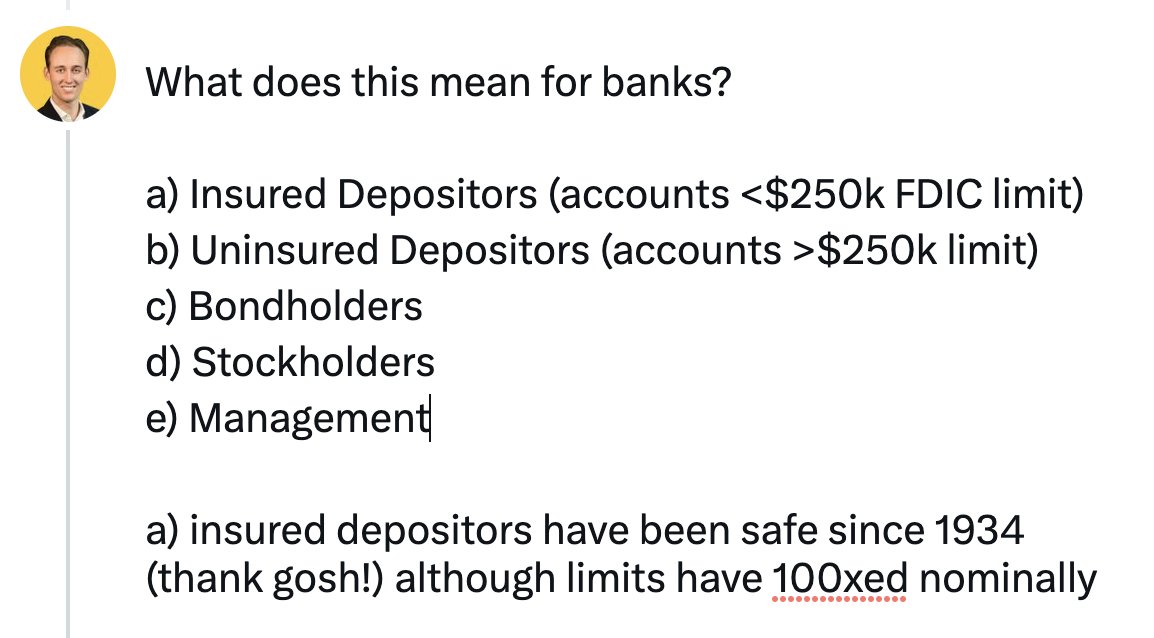

What does this mean for banks?

a) Insured Depositors (accounts <$250k FDIC limit)

b) Uninsured Depositors (accounts >$250k limit)

c) Bondholders

d) Stockholders

e) Management

a) insured depositors have been safe since 1934 (thank gosh!) although limits have 100xed nominally

a) Insured Depositors (accounts <$250k FDIC limit)

b) Uninsured Depositors (accounts >$250k limit)

c) Bondholders

d) Stockholders

e) Management

a) insured depositors have been safe since 1934 (thank gosh!) although limits have 100xed nominally

b) the FDIC & Treasury made whole uninsured depositors of SVB + Signature (two banks that failed over past week) and my guest thinks it is very likely that they will do so if more banks are taken over by FDIC (which is neither his nor my base case)

(7/22)

(7/22)

so systemic bank run? my guest says no.

However, for bondholder and stockholders (c & d), that's where he gets more pessimistic. He thinks banks' cost of funds will rise significantly and therefore their net interest margin will go down.

(8/22)

However, for bondholder and stockholders (c & d), that's where he gets more pessimistic. He thinks banks' cost of funds will rise significantly and therefore their net interest margin will go down.

(8/22)

For example, while the Fed's new facility (BTFP, Bank Term Funding Program) may prevent future bank failures, the yield that banks would pay to borrow with this program would likely exceed the yield on many of the investment securities they own.

(9/22)

(9/22)

that's why I was originally reluctant to call it a "bailout" - the emergency measures on Sunday directly protected b) but not c) d) or e)

(10/22)

(10/22)

So yes, my guest is optimistic regarding future bank failures (although he thinks there will be some consolidation) but relatively pessimistic about banks' earnings power going forward.

Now there are many positive things that the banks have going for them that we discussed:

Now there are many positive things that the banks have going for them that we discussed:

Now there are many positive things that the banks have going for them that we discussed (a-f)

a) banks very well-capitalized (have raised more equity, less leverage, etc.)

b) money has to go somewhere (under the mattress? c'mon)

(12/22)

a) banks very well-capitalized (have raised more equity, less leverage, etc.)

b) money has to go somewhere (under the mattress? c'mon)

(12/22)

c) a large percent of the banks' unrealized losses are in hold-to-maturity (HTM) portfolios and if they don't have to sell, those securities will be gradually pulled to par and no losses (except for opportunity cost)

(13/22)

(13/22)

d) credit losses have been remarkably low so far (with a few exceptions)

e) optimism and confidence is just as contagious as panic. therefore the same psychological forces that led to a bank run could lead to a surprising retention of deposits (not only amnts but also rates)

e) optimism and confidence is just as contagious as panic. therefore the same psychological forces that led to a bank run could lead to a surprising retention of deposits (not only amnts but also rates)

f) as much interest rate risk as the U.S. private banking system contains, the Federal Reserve also holds a LOT.

By not selling mortgage-backed securities (QT is conducted via balance sheet run-off), the Fed is actually INCREASED the amount of duration risk it holds... (15/22)

By not selling mortgage-backed securities (QT is conducted via balance sheet run-off), the Fed is actually INCREASED the amount of duration risk it holds... (15/22)

...because MBS have negative convexity (interest rate sensitivity increases as rates rise), and because the Fed is on the hook for so much rate risk, this is an ASSET for U.S. consumers and corporations who have locked in long-term funding at cheap rates...

(16/22)

(16/22)

...if you bought a house with a 2.9% 30-year fixed mortgage when the Fed kept rates at 0, you are in a very good position. Same with the companies that locked in low rates in the bond market.

(17/22)

(17/22)

Hope that addresses some of the pushback I got on this post

The interview airs on Monday.

(18/22)

The interview airs on Monday.

(18/22)

If you still think I'm trying to engineer a bank run I don't know what to tell you.

Have zero short positions in any bank stocks nor have I had any since this started (don't think I've ever really ever shorted banks tbh)...

(19/22)

Have zero short positions in any bank stocks nor have I had any since this started (don't think I've ever really ever shorted banks tbh)...

(19/22)

Have aired 5 interviews since emergency relief measures passed on Sunday from Fed+Treasury+FDIC and 0 of the 5 predicted further bank runs were likely, 0 out of 5 said in any way to pull money out as deposits.

(20/22)

(20/22)

As a matter of fact in 2 interviews a guest said they were buying bank stocks (not investment advice obvi but I'm just saying, I may be a noice but I am not the doom porn charlatan some of you seem to think I am!)

(21/22)

(21/22)

a final point: just because the U.S. banking system was under-hedged for 450 basis point rise in interest rates in 12 months doesn't mean that they SHOULD have been fully hedged. If you constantly buy insurance for a very rare event, you will lose money

(22/22)

(22/22)