Thread

A lot of talk over whether SVB "should" get a "bailout," but it's worth outlining that it might not be able to without legislation.

Crisis-fighters' authorities were curtailed following 2008. The Fed and Treasury almost certainly can't rescue SVB now. Maybeeee the FDIC...

[1/x]

Crisis-fighters' authorities were curtailed following 2008. The Fed and Treasury almost certainly can't rescue SVB now. Maybeeee the FDIC...

[1/x]

First, it's worth noting that whether SVB or any of its stakeholders "should" get rescued is not typically how *financial authorities* think about rescues.

The first test is typically "is it systemic?" - not clear we're anywhere near there yet.

The first test is typically "is it systemic?" - not clear we're anywhere near there yet.

The "should they get rescued" question thus probably falls to Congress. Insert: stock statement about how slow/unproductive Congress is. Not to mention the bind of the debt ceiling...

Ok, the Fed. It rescued Bear and AIG. But, it can't anymore.

The Dodd-Frank Act changes require all Fed interventions to be "broad-based" and not for the benefit a single institution.

The Dodd-Frank Act changes require all Fed interventions to be "broad-based" and not for the benefit a single institution.

But, couldn't it set up the Silicon Valley Emergency Liquidity Facility - making assistance broadly available?

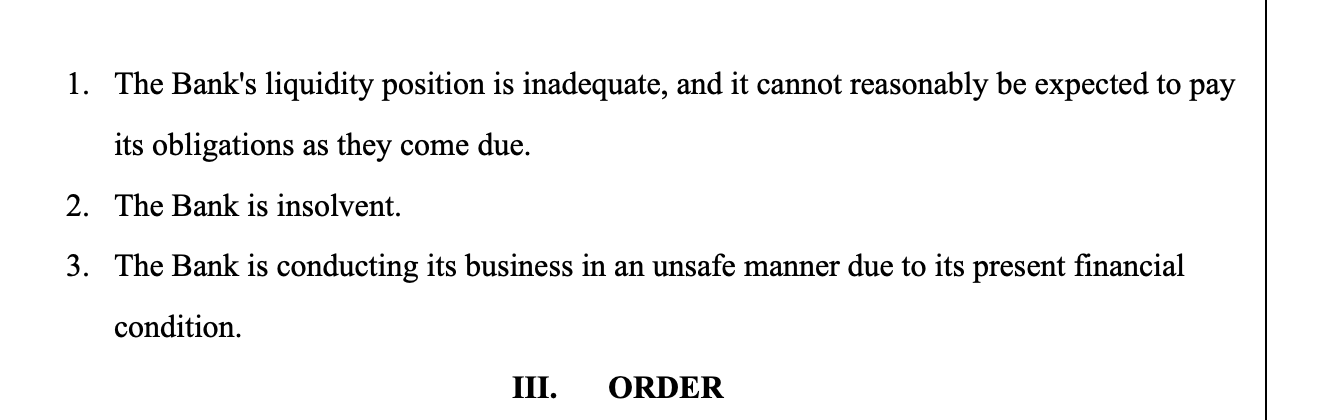

Dodd-Frank also forbade the Fed from assisting insolvent entities. The Fed has flexibility in defining "insolvent," but the SVB's state regulator declared it insolvent:

Dodd-Frank also forbade the Fed from assisting insolvent entities. The Fed has flexibility in defining "insolvent," but the SVB's state regulator declared it insolvent:

Ok, so the Fed is out. What about Treasury?

Treasury can't spend money that hasn't been legislated. The only real discretionary money it has is in the infamous Exchange Stabilization Fund. The ESF backed some systemwide interventions in 2020 and one in 2008.

Treasury can't spend money that hasn't been legislated. The only real discretionary money it has is in the infamous Exchange Stabilization Fund. The ESF backed some systemwide interventions in 2020 and one in 2008.

Originally designed for FX intervention, the ESF is available to promote orderly exchange rates and systemic stability — and has about $200B.

sites.duke.edu/thefinregblog/2021/08/10/while-congress-is-asleep-the-future-of-u-s-financial-crisis-r...

sites.duke.edu/thefinregblog/2021/08/10/while-congress-is-asleep-the-future-of-u-s-financial-crisis-r...

While its legal constraints are vague, Treasury lawyers rejected use of the ESF for Bear Stearns & for AIG in 2008 — but signed off on using it to rescue the multi-trillion-dollar money market fund industry.

If Bear and AIG didn't meet the threshold, SVB definitely doesn't.

If Bear and AIG didn't meet the threshold, SVB definitely doesn't.

So Treasury's out. What about the FDIC?

Can they just tell all uninsured depositors that they get their money back? It wouldn't be easy.

Can they just tell all uninsured depositors that they get their money back? It wouldn't be easy.

The FDIC is legally obligated to resolve a bank in the fashion that is the "least cost" to the deposit insurance fund.

It's a reallyyy tough argument for the FDIC to make to say that paying out uninsured deposits is the "least cost."

It's a reallyyy tough argument for the FDIC to make to say that paying out uninsured deposits is the "least cost."

The FDIC can invoke its so-called systemic risk exception. This was the basis for the FDIC's bank debt guarantees and expanded deposit guarantees in 2008.

Dodd-Frank requires Congress to now sign off on such a broad-based use, and banned its use for a single *open* institution. However, now that SVB is in FDIC receivership, it's eligible.

But the FDIC can only invoke the exception if a "least-cost" resolution would mean "serious adverse effects on economic conditions or financial stability" and the exception "would avoid or mitigate such adverse effects."

Again, a tough standard to meet. And even if the FDIC signs off on that, the systemic risk exception also requires signoff from the Treasury Secretary (easy) and two-thirds of the Fed Board. And it's especially not clear the Fed would think this is systemic.

All of which is to say, the "should SVB get a bailout" question might be putting the cart before the "can they" horse.

Of course, there's always private money - and we'll see where the bids come in for the deposit franchise.

/end

Of course, there's always private money - and we'll see where the bids come in for the deposit franchise.

/end