Thread

Fears of another liquidity crisis have entered the mainstream, with many people guessing what will cause the next financial upheaval. Right now, all triggers have been suppressed, but not for long. The Great Liquidity Squeeze™ is upon us... 1/

2022 was believed to be the year when an enormous unwinding of central bank liquidity would produce another round of financial armageddon. But it never came. Instead, the response from monetary leaders over the COVID market meltdown more than prevented economic ruin...

After an epic financial bonanza, we've witnessed the rise of a risk-off environment like no other, a "slow grind" lower in most risky asset classes. The peak in global growth paired with the start of a long-awaited Fed tightening cycle ended the mania in the final days of 2021...

But the usual meltdown we've seen before in previous cycles was met by trillions of excess liquidity desperate to find a home. Unlike the COVID crash, the monetary excess era was able to neutralize levels of volatility that could cause a crisis...

It took a while, but over time market participants not only adapted to this new "slow grind" regime but reinforced it. So much so that the market's structure has shifted to enable the unhealthy suppression of volatility. Today, few are worried about protecting against losses...

A major flaw of finance is that it nearly always mutates the very instruments meant to protect investors into crisis-inducing time bombs. Coincidentally, over the past few quarters, we've seen the early innings of the latest instance play out, this time in derivatives markets...

As market participants have adapted to the "slow grind down" regime, they have come to think of buying protection using options as futile. Hedging with options only makes sense if you expect implied vol to soar. But today's market has been defined by volatility suppression...

One of the biggest losing trades of last year was buying VIX products (or other long volatility proxies) to hedge against falling stock prices. This, as usual, produced theories about the VIX being manipulated by the Illuminati or comparable shadowy outlets. In reality...

The lack of volatility, which usually spikes in bear markets, can be explained by today's status quo. Without a catalyst like a virus or banking panic sparking fear, the latest market downturn has been a snooze. Volatility is elevated but also contained by cash-rich parties...

Awash with capital and tired of losing money elsewhere, speculators have started piling into options that expire on the same day, known informally as "0DTE". These same-day expiries now make up a whopping 40-60% of daily options volumes. What could go wrong? A lot, it seems...

The major misconception is that retail investors, like in the COVID market mania, are now driving another speculative frenzy in the short-term options market. In reality, the "dumb money" is a mere 6-12% of 0DTE volume. Institutional traders are the major driving force...

The "smart money" is now exploiting a new regulatory loophole in the options market to make a quick (lucrative) buck. They are selling large amounts of deep out-of-the-money 0DTE options, without having to post margin to clearinghouses, who don't count intraday expiries...

It's "easy money" but fraught with risks. The reason these entities haven't blown up yet is that their actions have fueled and reinforced the volatility suppression dynamic. When, not if, they vanish from 0DTE options, those needing to cover will have few parties to sell to...

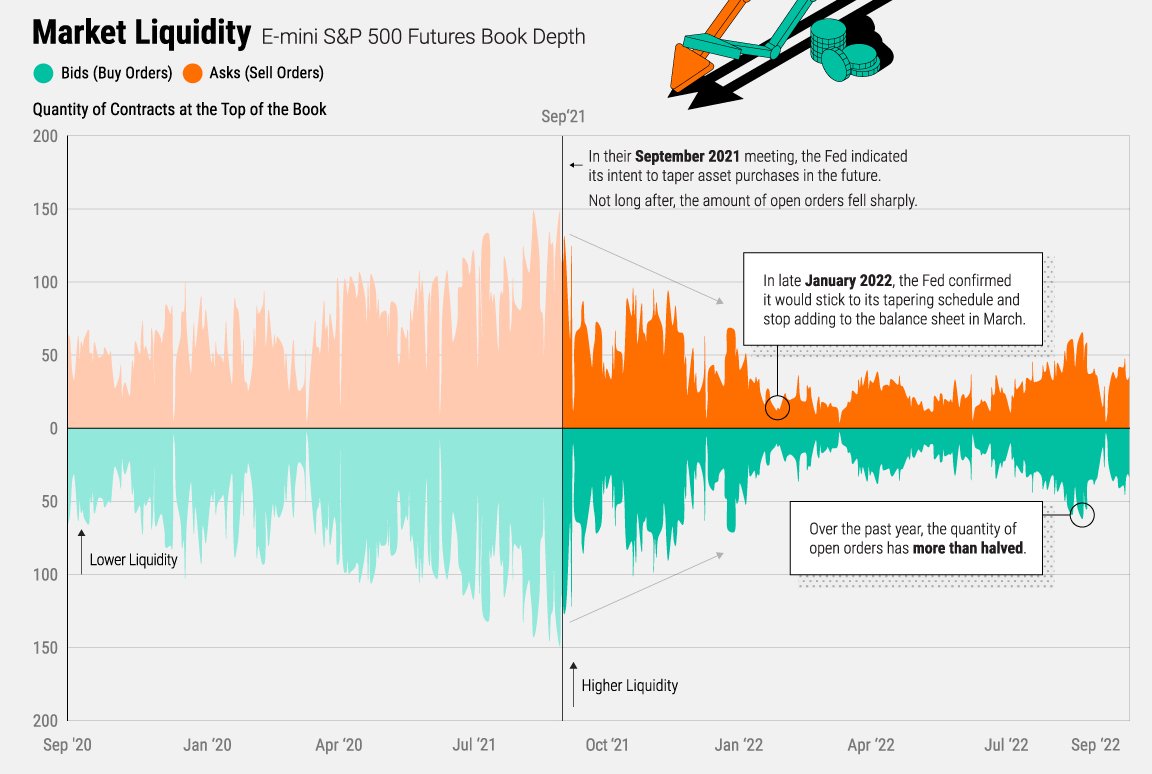

The market is heavily concentrated, with a few types of players providing most of the liquidity. Banks don't want to bear the risks while hedge funds want to avoid the wrath of angry clients. That leaves market makers, algo traders, and dynamic hedgers. Therein lies the hazard...

When you pair the sudden exit of a large market player with how liquidity in the stock market has sunk during the Fed's tightening cycle, we could see high levels of volatility (which you'd usually expect in a bear market) make an unwelcome return...

If the rules of the game change, volatility could return to its former spikey glory, turning this bear market into a normal, volatile replica. All it takes is an unexpected departure from a large market participant or a sudden move from a regulator who's started to take notice...

In February 2018, "Volmageddon" erupted, where a mix of dubious innovation and greed ended in a sharp stock market selloff, plus the death of volatility products like Credit Suisse's infamous "XIV" ETN. A suspected trigger was the Fed adding stricter capital constraints...

Today, similar threats linger. Low volatility tends to spawn lower volatility, creating the ideal incentive structure for blowups. We're witnessing the largest compression since Volmageddon in an already illiquid market. Though, as with most blowups, these take time to unravel...

Whether it's the private sector, regulators, or a combination of the two that causes the next volatility cascade, this is a match that has yet to be lit. And as Concoda noted earlier, a similar scenario exists in many areas of financial markets. It's the calm before the storm...

Early signs of waning liquidity have emerged deep in the monetary system. The spread between Fed Funds and SOFR, which measures the balance between cash versus Treasury collateral, suggests that cash is becoming less plentiful...

Meanwhile, many people have started to point to the gradual rise in "emergency loans" that the Federal Reserve has extended through its Discount Window, where it acts as a lender of last resort to banks in need of funding. This, however, is only an early sign of stress...

The rise in loans does not imply a banking panic but more a shortage of liquidity gaining momentum. A slow uptick points to a willingness to borrow funds directly from the Fed, even though a potential "stigma" will likely be attached to them...

It's believed that other institutions can figure out who's using the facility, thereby applying a negative stigma on those wanting to borrow. If any party changes its behavior in the interbank market, it would become an easily identifiable target to avoid lending to...

But in today's monetary system, this "stigma" appears to have grown insignificant. Since 2008, authorities have transformed the system almost entirely, punishing banks with regulatory costs when they lend cash to each other in the Fed Funds market...

A variety of alphabet soup regulations (NSFR, SLR, LCR, etc.) penalized banks for partaking in UNSECURED forms of lending, such as Federal Funds. Subsequently, the market for unsecured interbank lending has subsided...

Squinting at the average bank balance sheet (below), you can almost make out the amount of Fed Funds borrowed between institutions with access to the interbank market, mostly commercial banks and government-sponsored entities (GSEs)...

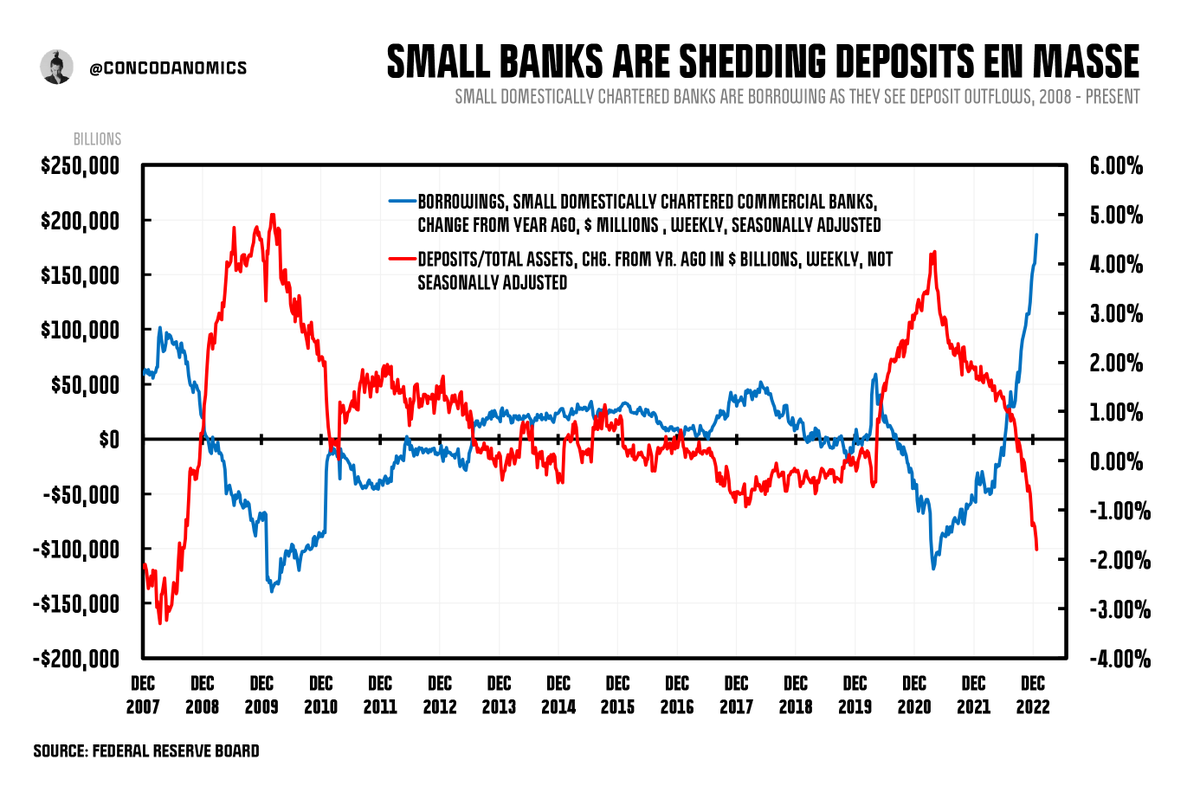

In response to regulations, banks replaced Fed Funds with more retail deposits and other balance sheet-friendly sources of funding. Today, financial institutions overwhelmingly choose to borrow via SECURED forms of lending...

One of those being repurchase agreements, or "repo" for short. Market participants borrow cash overnight (or for longer) by pledging collateral, usually Treasuries or state-issued mortgage-backed securities...

Nothing shows the near-demise of the Fed Funds market like the relative volume of SOFR (the Secured Overnight Financing Rate), the benchmark for secured repo lending. Around $100 billion in Fed Funds change hands every day, compared to $1.1 TRILLION in SOFR...

Since regulations discourage banks from lending to each other and repo has become a vital cog in the monetary plumbing, the chances of "Discount Window stigma" remain slim. Entities now feel safer when borrowing directly from the Fed. The question now is who...

JPMorgan pointed to numerous small banks who (bizarrely) appeared to avoid hedging interest rate risk in their securities portfolios, a relatively routine practice of a bank's risk department following the 2008 financial crisis...

The Wall Street giant found that around 30 banks (with total assets of less than $1 billion) had fallen into negative equity as of September 2022, an increase from zero since the start of last year...

It's hard to imagine risk departments at banks failing to hedge their books with interest rate swaps (hence offsetting the losses above) in a highly inflationary environment. Alas, if they were living under a rock, they could have been tapping the Fed for funding...

A more badass explanation also exists: consumers are becoming wise to the game being played by the banks. As the Wall Street giants pay barely any interest, consumers have likely decided to transfer their deposits into money market funds, Treasuries, and even the stock market...

Consequently, as depositors withdraw en masse, banks have had to replace these deposits, which they were previously using for funding, with other more costly sources. This could include borrowing in repo or in the Fed funds market...

(h/t @RashadA334)

(h/t @RashadA334)

But as these outflows have coincided with a boom in loan growth, it's likely some banks have faced balance sheet issues. They could not only have resorted to balancing their books by using costly sources of funding but by even borrowing directly from the Fed's Discount Window...

Other potential theories have been offered. Some institutions may find the penalty rate attractive despite the Fed's premium rate, and crypto and fintech banks have suffered major losses. Nevertheless, their usage of the Discount Window shows financial strains only emerging...

Again, like with the misaligned incentives in market structure, it seems that poor liquidity is just a match without a flame. With bad incentive structures only starting to turn sour and liquidity in the system far from constrained, we turn to the most imminent hazard...

As of September last year, the Fed's QT (quantitative tightening) program has entered full swing. Yet, its effects have been minimal. QT has had much less of an impact on deterring inflation and risk sentiment than policymakers, commentators, and the financial media expected...

Still, the QT process will drain enough reserves from the system to prompt monetary leaders to increase liquidity before a squeeze or (the most probable scenario) react to another money market tantrum when hysteria emerges...

For now, reserves remain ample for the large systemically-important banks, which possess trillions of dollars in reserves sitting in their Fed accounts, ready to settle payments. But plentiful liquidity won't last forever...

Liquidity is about to decline rapidly in the largest, most aggressive Fed rug-pull since, well, the Fed's last attempt to reduce its balance sheet. The Fed will now try to roll off a maximum of $95 billion a month from its $8.5 trillion asset portfolio...

The size of the balance sheet, although enormous, is not an imminent concern of the Fed or the banks. Instead, it's the number of reserves that QT also sometimes removes when bonds are rolled off. To the Fed, if reserves fall to $2 trillion, the potential for chaos emerges...

While we predict it will take around nine months to run into issues, some Fed experts Concoda spoke to indicated that liquidity problems could emerge within half a year. This again ties in with the common theme of adequate liquidity that's withering slowly...

Emerging threats have yet to become menaces. Options with same-day expiries provoking the next Volmageddon, or the Fed creating an eventual bottleneck in the monetary plumbing, are just some perils that lie ahead. In each scenario, however, turmoil will take time to emerge...

As @BobEUnlimited dubbed it, we're in a "transitory goldilocks" period, where slowing growth meets disinflationary forces. This is a recipe for the "slow grind" status quo to continue. Hedging will turn into speculation which will turn into ruin. The usual cycle iterates...

Unsustainable levels of volatility and illiquidity will return to markets once again, prompting the long-awaited Fed Pivot™. But the real dilemma is knowing when this will occur and what will be the trigger. As you, and hopefully some Fed officials now know, many remain...

When volatility suppression turns into a volatile blowup, the response from monetary leaders will look all too familiar but in much greater magnitude. The Fed's volatility suppressor, the only true entity capable of stifling market turmoil, is about to face its latest challenge.

If you enjoyed this, feel free to retweet the opening tweet of this thread and follow @concodanomics for more.

You can also subscribe below to receive free in-depth articles about finance, markets, and geopolitics in your inbox...

concoda.substack.com/subscribe

You can also subscribe below to receive free in-depth articles about finance, markets, and geopolitics in your inbox...

concoda.substack.com/subscribe

ARTICLE VERSION: The Coming Liquidity Squeeze

As illiquidity and volatility rises to ominous levels, all threats to financial stability have been thwarted, but not for long

concoda.substack.com/p/the-coming-liquidity-squeeze

As illiquidity and volatility rises to ominous levels, all threats to financial stability have been thwarted, but not for long

concoda.substack.com/p/the-coming-liquidity-squeeze

Mentions

See All

Grant Williams @ttmygh

·

Jan 18, 2023

Another superb thread from @concodanomics