Thread by Concoda 🥷

- Tweet

- Oct 21, 2022

- #BondMarket #FinancialCrisis

Thread

Bond markets are growing increasingly unstable, and many have warned of a "sovereign debt crisis" unfolding. But monetary leaders now possess numerous tools to prevent a disaster. The Great Sovereign Debt Intervention™ is upon us... 1/

Tasked with preventing sky-high inflation largely caused by supply issues beyond their control, the Federal Reserve has been forced into raising rates sharply to lower prices toward their 2% target...

This will undoubtedly cause substantial pain worldwide. Rate differentials will spur a stronger U.S dollar, affecting the 50% of transactions invoiced in Greenbacks globally. The Fed's gambit is to fight inflation without "blowing up" other nations through a rising U.S dollar...

Many commentators deem rate hikes to be the worst solution to what has been a crisis of supply. But political goals have ensured that dollar fatalism will be enforced to battle rising prices. For now, the "dollar milkshake wrecking ball" will keep crushing prosperity worldwide...

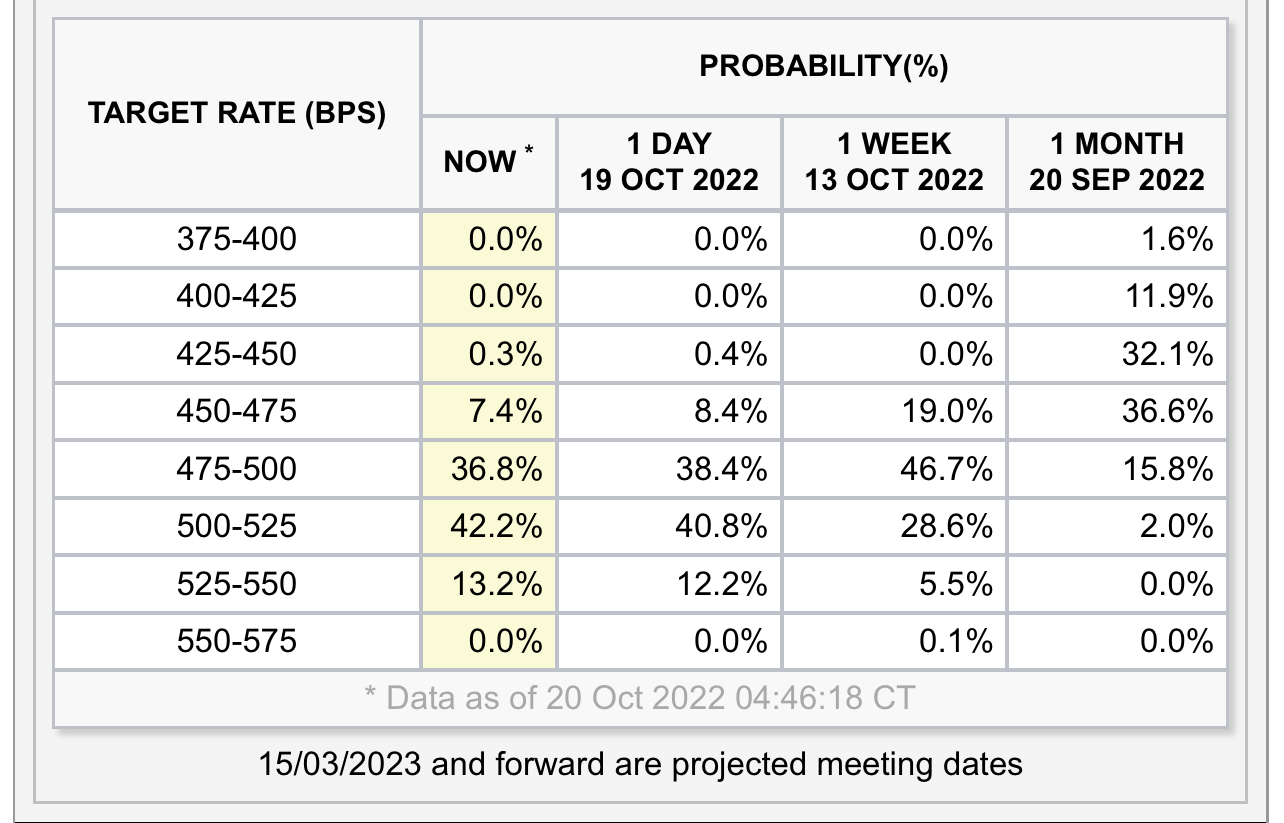

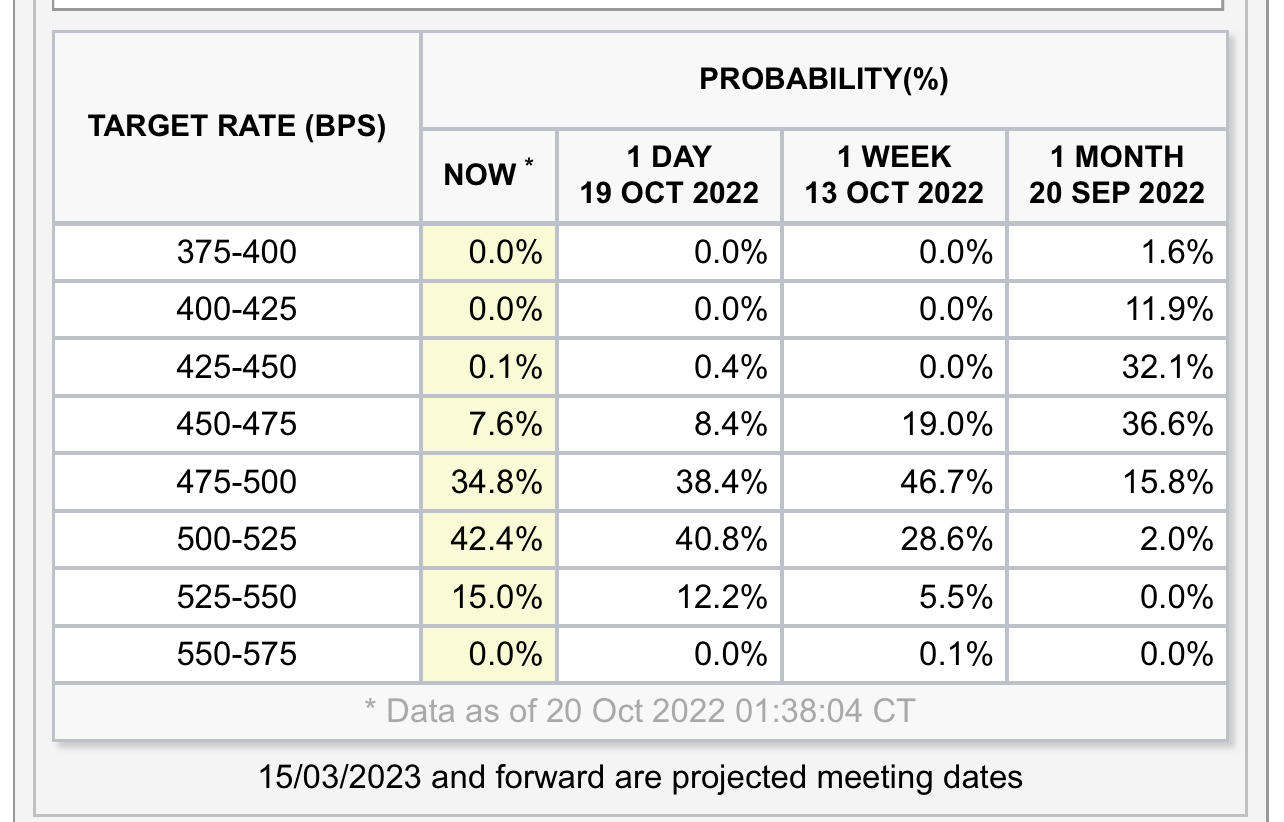

With the potential for another 2% in rate hikes by March 2023, and inflationary pressures continuing to build, further Treasury market turmoil is about to unfold...

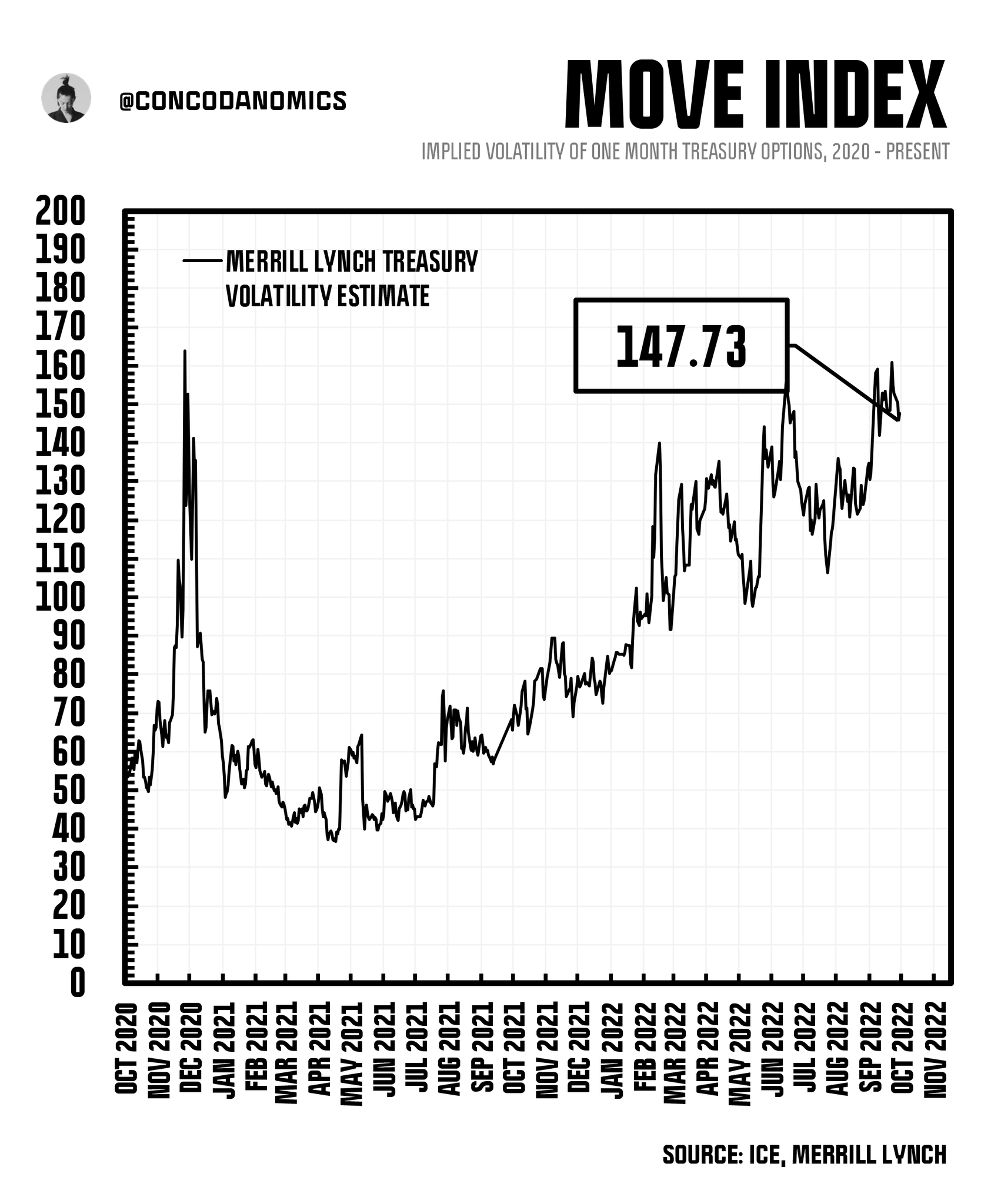

Just this week, bond yields have risen to levels not seen since the failure of Lehman Brothers. The expansionary impulse of trillions in stimulus, plus the sharpest rate hiking cycle in decades, has caused a significant selloff in Treasuries...

While yields have risen due to the market's perception of inflation, growth, and interest rates, rising volatility has revealed structural weaknesses. America continues to issue twice the amount of bonds per year compared to pre-COVID, into increasingly illiquid conditions...

Concoda’s “illiquidity spiral” (the doom loop of volatility creating illiquidity creating more volatility, and so on) is playing out, wreaking havoc in America’s sovereign debt market...

Increased volatility, diminished liquidity, and declining market depth means further instability is assured, which will likely send bond yields higher. Monetary officials will eventually have to intervene, and with intervention comes monetary alchemy...

Central planners have an abundance of mechanisms to prevent (what some assume to be) a sovereign debt bubble from bursting. With numerous tools in hand, officials will only resort to full-on yield curve control as a last-ditch attempt to rescue Treasury markets...

Instead, at the earliest indication that illiquidity is becoming hazardous, Treasury officials will respond with a different solution: Treasury buybacks...

Using funds from either bond sales or its bank account at the Fed, the U.S Treasury will repurchase bonds in the secondary market (via primary dealers such as JPMorgan and Nomura) to improve liquidity and suppress yields. Higher bond prices equal lower yields and expenses...

The aim is to revive Treasury market liquidity and suppress volatility, while also earning America the added bonus of reducing interest payments on its outstanding debt...

Previously, Treasury buybacks have been an effective tool for suppressing bond volatility, yet it's unlikely to dampen today's record-high levels. Officials will have to fire up their next mechanism: indirectly incentivizing large financial players to buy more Treasuries...

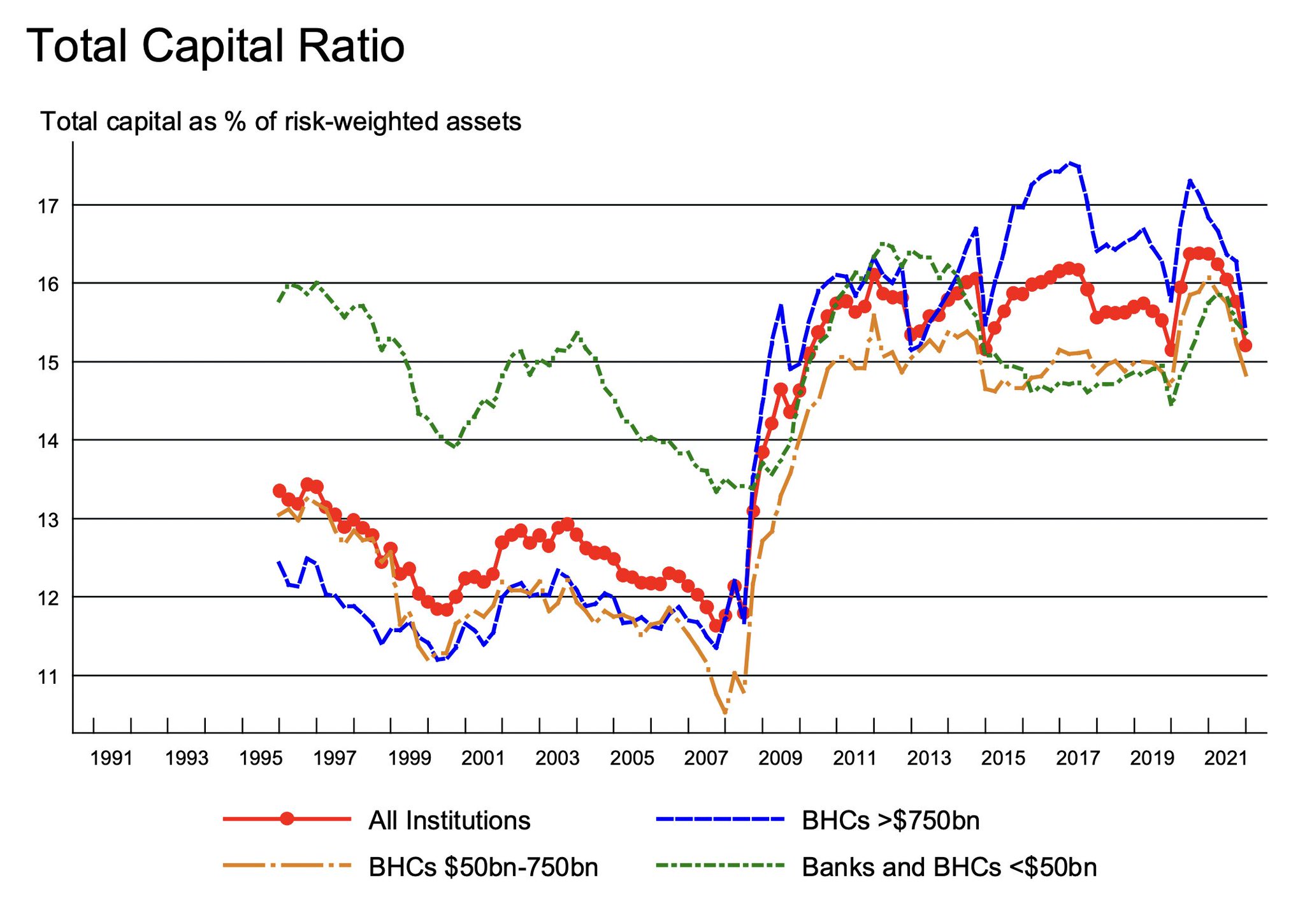

This, however, is easier than it sounds. Ever since the Great Financial Crisis (GFC) in 2008, banks have become "balance sheet constrained," a fancy way of saying regulation has prevented financial entities from taking on too much risk, even if it's beneficial to the system...

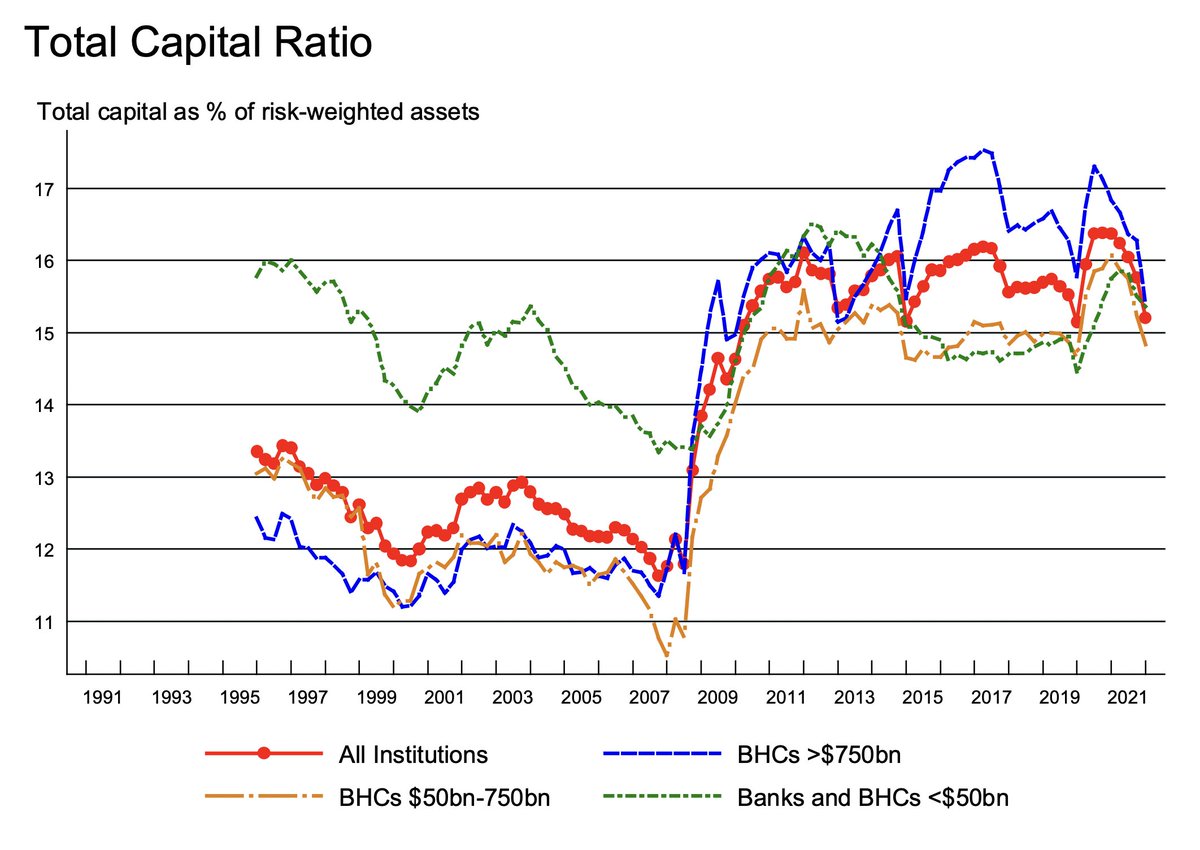

In the GFC’s aftermath, the Bank for International Settlements (BIS), the self-described "central bank for central banks", introduced its third round of rules: the Basel III Accords. This set out a plethora of rules and regulations, aimed at preventing future crises...

Regulators had taken a hard line against fraud-ridden bubbles like the subprime MBS boom of 2007/2008. Subsequently, banks have had to retain a lot more capital relative to their assets (a higher "capital ratio") to comply with regulations...

Banks had to also retain enough "high-quality assets" (HQLA), such as bank reserves and Treasuries, to meet their Liquidity Coverage Ratio (LCR). This regulation requires financial institutions to hold 30 days' worth of HQLA, so they can handle customer outflows during crises...

Still, with this large safety net, big players have not been buying enough bonds to create normal levels of volatility in Treasury markets. But that's about to change. When chaos ensues, monetary officials will modify with another rule: the SLR, or Supplementary Leverage Ratio...

The SLR directs banks to hold around 3-5% capital against “unweighted assets”, meaning even risk-free reserves and Treasuries are deemed just as unsafe as risky investments, like mortgage-backed securities (MBS).

This was a reaction to the events of the financial crisis...

This was a reaction to the events of the financial crisis...

During the subprime boom, mortgage-backed securities were deemed so safe that banks couldn't imagine a scenario where they went to zero. What's more, banks believed they'd taken out risk-free credit default swaps against MBS, which would hedge them against a financial disaster...

But as we found out, safe assets can become tainted. Not too long ago during COVID, even the Treasury market lay on the brink of a meltdown before authorities intervened. In reaction to the subprime crisis, however, banks had to implement SLR.

This created strange results...

This created strange results...

The SLR, along with other regulations in the Basel III Accords, has increased the financial system's peculiarities. Since it prevents bank balance sheets from becoming too large, banks must now MAXIMIZE returns on a SMALLER portfolio of assets...

This resulted in banks ditching low-yielding assets that curbed their profitability, one of those being Treasuries.

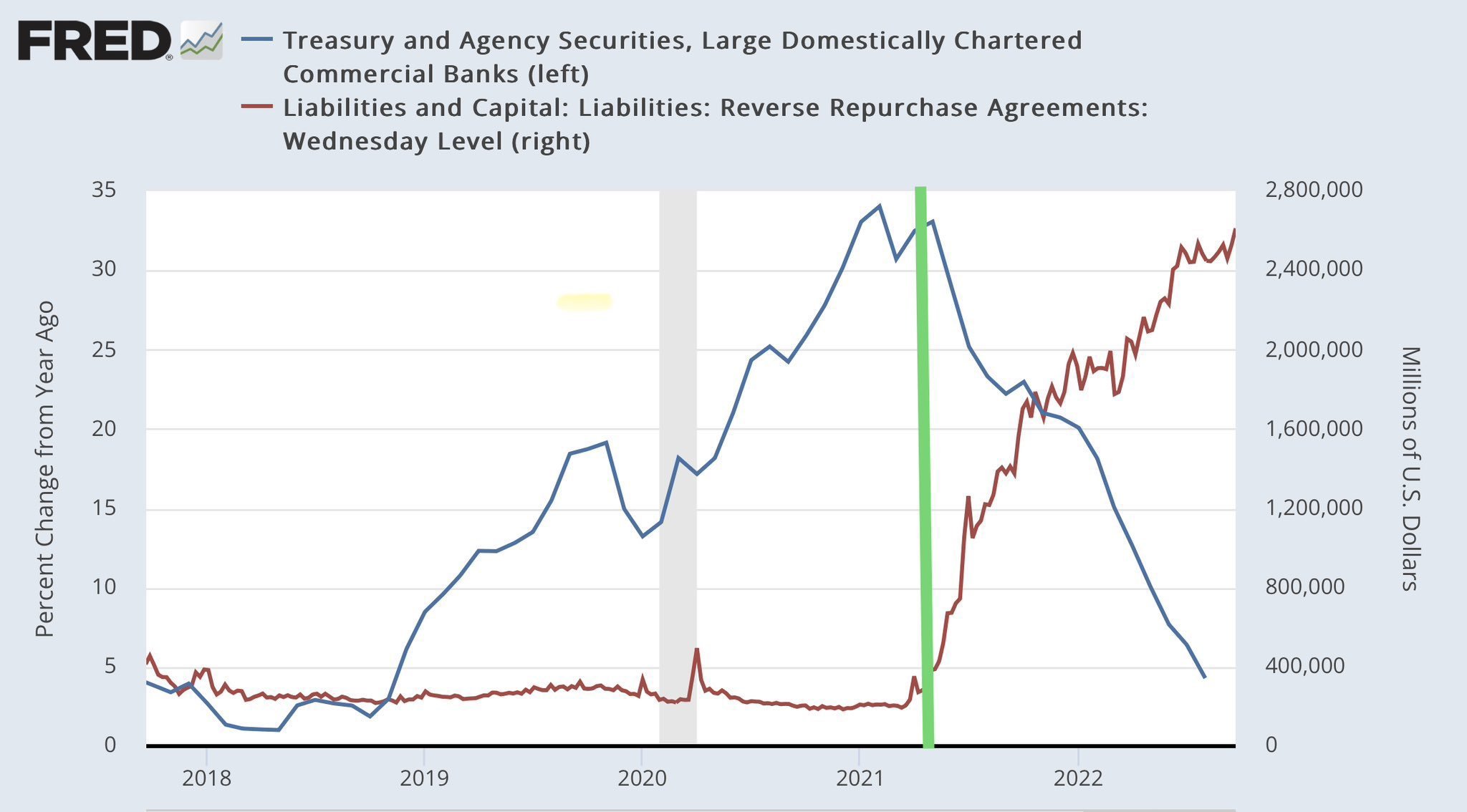

Then, again, COVID changed the game. One month after the crash in April '20, trillions of government debt entered the system...

Then, again, COVID changed the game. One month after the crash in April '20, trillions of government debt entered the system...

Banks were given "SLR relief" and were now allowed to hold more Treasuries and reserves with no regulatory constraints...

After the crisis turned into calm, regulators removed SLR relief in March 2021. Banks DUMPED their Treasuries en masse, as it hindered their profitability once again...

h/t @siddiqui71

h/t @siddiqui71

Now, when Treasury buybacks prove ineffective, authorities could entice big players to gorge on a larger number of Treasuries (instead of being mere middlemen). Multiple federal agencies must sign off to provide "SLR relief", but in a panic, there will be no hesitation...

Freed from the constraints of SLR, large banks will be able to absorb a larger number of bonds at no cost to their regulatory ratios. But they must be willing to buy. If they aren't enticed, authorities must increase temptation...

Before going into full-on “yield curve control mode”, the Fed will try imposing a “soft ceiling”, announcing they'll temporarily buy a certain amount of Treasuries at a set rate. Market players will likely participate, and Treasury volatility will wane. Or so you'd think...

Because in the last few months, an alternate prophecy has emerged in mainstream financial circles. Prominent thinkers have predicted that inflation could persist even after every major supply issue has been resolved. That could mean higher bond yields for longer...

They argue that since global demographics and globalization have peaked, the subsequent impacts will cause a structural shift toward persistent inflation. They say deflation in Japan was an anomaly, caused by the disinflationary force of China joining the global U.S order...

Now that China's growth model has peaked, among other catalysts, inflation could stick around longer than any policymaker anticipates. They could be caught off-guard by long-term structural forces...

Monetary leaders are well aware of how bonds act in the current paradigm. But now they must consider what might happen if inflation is far from transitory...

If the contrarian prediction comes true, Concoda predicts officials will try to cling to the status quo of lower yields for as long as possible. In response, they will utilize a new set of tools to maintain lower bond yields in a persistently inflationary environment...

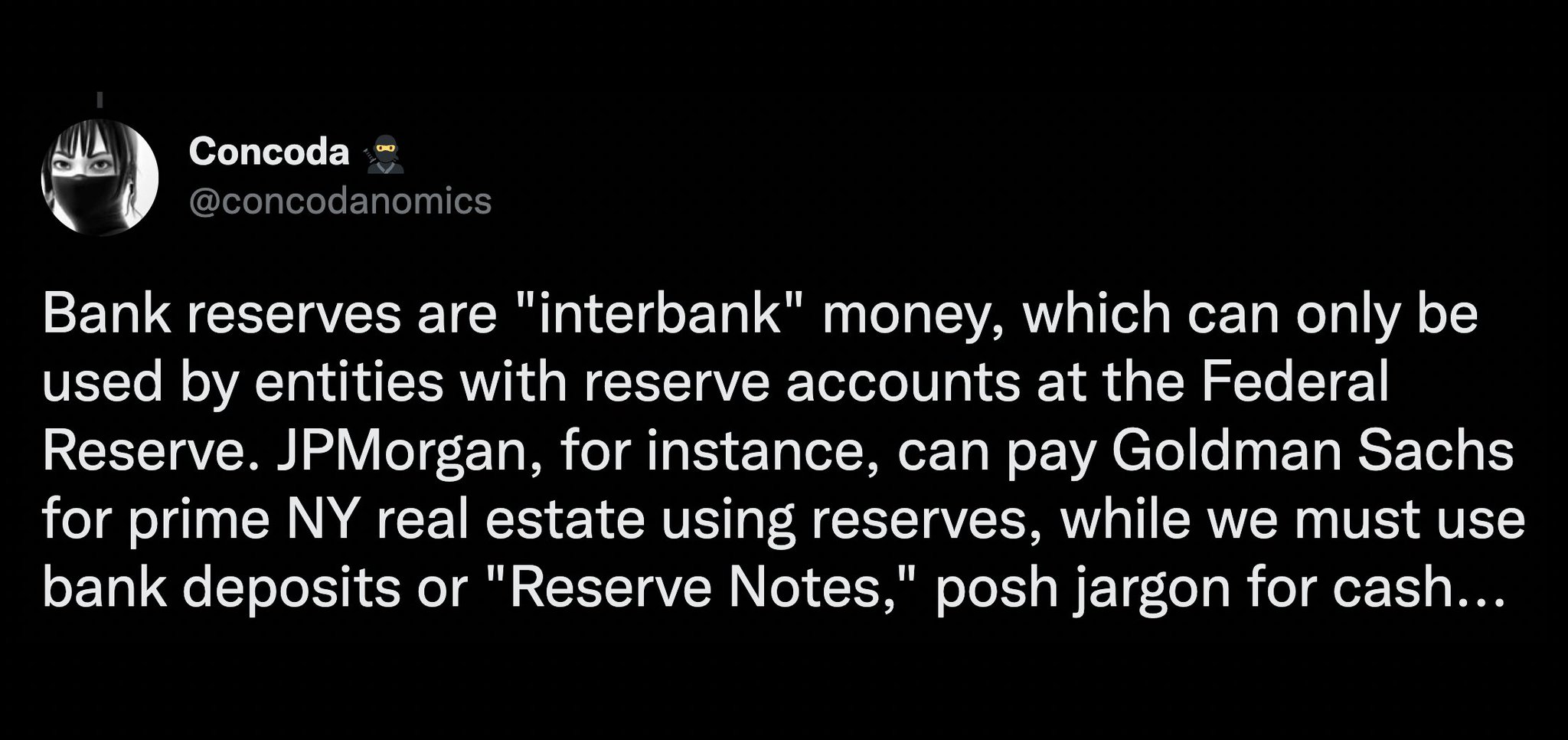

Officials will eventually start to utilize their most powerful tool: yield curve control, imposing an "upper bound" on yields. With the ability to create INFINITE amounts of money in the form of bank reserves, the Fed will buy as many bonds as they need to suppress yields...

While this will limit the amount of interest the U.S government pays on its debts, it will not solve inflation. And if measures outside rate hikes don't manage to control rising prices, the Fed's upper bound might meet some serious opposition...

Though unlikely to reach such a situation, the U.S could mandate citizens to buy government bonds, reducing pressure on the upper bound but, more importantly, preventing the Fed from directly buying bonds from the U.S Treasury (currently illegal under the Federal Reserve Act)...

With most citizens wanting stability, not calamity, most will oblige, bearing the burden of what will likely become highly negative (real) yielding assets. But if they aren't tempted, the persuasion toolbox for incentivizing bond buying can always expand...

The U.S government could introduce measures such as increasing rent controls to discourage real estate investment, raising taxes on stock purchases, and even curbing the ability of U.S citizens to invest abroad...

Monetary and fiscal alchemy will be pushed to new limits, but as Concoda has stated before, we won't even come close to a U.S "sovereign debt collapse" that many have warned about for decades...

Nor will we see a "debt jubilee". History does show ancient rulers canceling debt when it created too much social tension and low productivity. But since pensions now hold so many sovereign bonds, debt cancelation would cause systemic risk. Jubilees simply aren't feasible now...

In fact, many nations are already carrying out a quasi-debt jubilee. Central banks such as the Fed and BoJ have been acquiring bonds on their balance sheets, turning their sovereign debt into interest-free loans that never need repaying...

When the bonds mature, central banks take the principal they receive and buy newly-issued Treasuries from the secondary market. And since central banks send all interest payments back to the Treasury during the bond's tenor, a perpetual interest-free loan is created...

Japan has already been canceling around half of its debt and will eliminate roughly ¥90 trillion more each year. The U.S, meanwhile, is paying off around a quarter of its liabilities, free of charge.

Though, for the U.S at least, this is changing as we speak...

Though, for the U.S at least, this is changing as we speak...

With Quantitative Tightening (QT) underway, the Fed is forcing citizens (who won't offer the state a free perpetual loan) to fund more of America's debt. QT is transferring ownership of bonds from the Fed to the private market, requiring more public trust to fund the U.S govt...

The fact that the Federal Reserve, hence the U.S government, is willing to take on more responsibility for rolling over U.S debt shows monetary officials are far from entering panic mode at the moment. They are hoping the skeptics are proven wrong once again.

If not...

If not...

The endgame for America's Great Sovereign Debt Intervention™ will be permanent support from the Federal Reserve. At whatever cost, bond market stability will be achieved, making today's policies seem normal.

For other nations, however, their bond markets might not be so lucky.

For other nations, however, their bond markets might not be so lucky.

Thanks for reading!

If you enjoyed this, feel free to retweet the opening tweet of this thread and follow @concodanomics for more.

You can also subscribe below to receive free in-depth articles about geopolitics, finance, and economics in your inbox.

concoda.substack.com/subscribe

If you enjoyed this, feel free to retweet the opening tweet of this thread and follow @concodanomics for more.

You can also subscribe below to receive free in-depth articles about geopolitics, finance, and economics in your inbox.

concoda.substack.com/subscribe

Article version just dropped: concoda.substack.com/p/the-great-sovereign-debt-intervention?utm_source=post-email-title&publication_...