Thread

There's a common misconception that apartment construction has moved to suburban locations as a result of the pandemic. That isn't exactly true. Yes, suburban construction is up ... but urban construction is up even more for reasons not directly related...

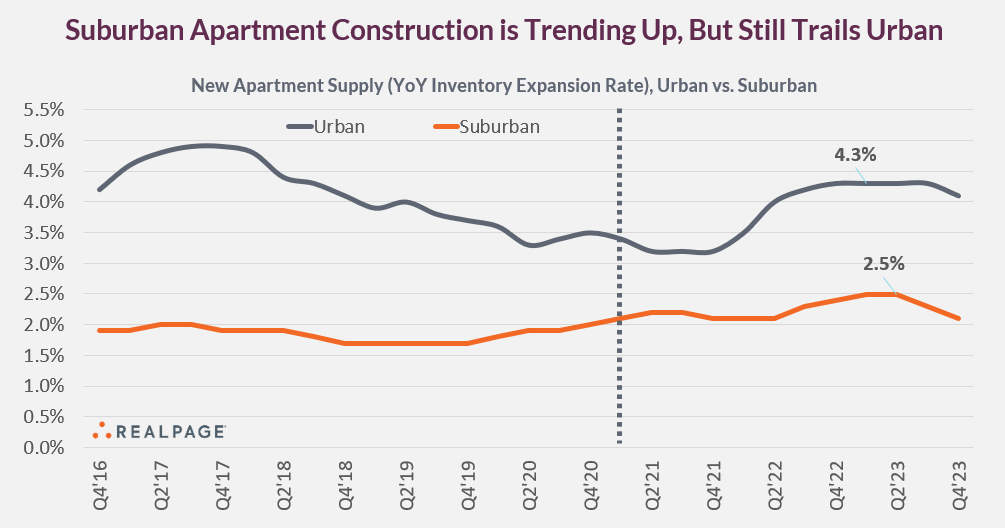

Bottom line: Apartment supply will continue to grow at a much faster rate in urban locations (CBDs and surrounding neighborhoods) than in the suburbs -- at least over the next few years...

Here's what happened: Prior to COVID, starts decelerated in many urban locations due to 10+ years of elevated supply + softening performance.

When COVID hit, there was heightened interest in suburbs ... And yes, we did see permits and starts accelerate, BUT...

When COVID hit, there was heightened interest in suburbs ... And yes, we did see permits and starts accelerate, BUT...

... probably not nearly as much as you might think. Why is that?

Developers in high-demand suburbs continued to run into challenges with limited site availability, restrictive zoning, NIMBYism, and perceived land price barriers (which turned out to be a bargain in hindsight)...

Developers in high-demand suburbs continued to run into challenges with limited site availability, restrictive zoning, NIMBYism, and perceived land price barriers (which turned out to be a bargain in hindsight)...

With land prices compressing between urban and suburban locations (and with challenges securing the more desired suburban sites), the urban and near-urban locations all of a sudden started looking more attractive...

That resurgence in construction will translate to another spike in urban completions starting in late 2022 and extending into 2023 and likely 2024. Urban completions peaked with an expansion rate of 4.9% in 2017, slowed to 3.2% in 2021, and will jump up to 4.3% by 2023...

Meanwhile, suburban completions nationally currently amount to just a 2.1% expansion rate, and are scheduled to peak in 2023 at just 2.5%. Suburban construction tends to be more spread out and less concentrated than urban -- making it less competitive with existing apartments...

Big picture-- this is one reason why we remain very bullish on the suburbs, particularly higher-rent, high-quality suburbs in the Sun Belt but really all across the country.