It's not 2008 again

It's not 2008 again

It's probably not even 2000

Financial headlines are replete with bad news: the S&P 500 is down 16% year-to-date, with previous market darlings like Amazon (-35%), Robinhood (-45%), and Netflix (-69%) down even more. Last month, we even had a negative GDP print and the Federal Reserve is continuing to hike rates to tamp down on staggeringly-high inflation.

All of this doom-and-gloom has prompted many observers to worry about a repeat of the 2008 financial crisis, or at least a redux of the 2000 tech bubble crash. I’m here to echo most mainstream commentators and say “probably not”. Risks in the economy are very real, but we probably are not currently in a recession. If a recession ultimately does occur, it very likely will be less severe than 2008, and probably less than 2000 as well.

Banks are far better situated than in 2008

Let’s start with the 2008 financial crisis. Despite a laundry list of aggravating factors, at its core 2008 was a bank run on the shadow banking sector. In short, banks had a lot of short-term debt (often overnight loans) that they continually rolled over. Meanwhile, their assets were mostly long-term (such as mortgage-backed securities). Once a spate of bad news rolled in (such as home default rates ticking up), embattled banks’ creditors got skittish and refused to roll over the debt. Suddenly, these highly leveraged banks had to come up with the cash to pay off the loans immediately. Even if they were fundamentally solvent, they were temporarily illiquid. Since so many of their assets were complicated long-term assets, they couldn’t find buyers for their products quickly and had to firesell the assets to get the money immediately. A liquidity crisis thus metastasized into a solvency crisis. As other creditors worried that their counterparties were in similar dire straits, they too refused to roll over their debt. Just like a bank run.

Is this a (big) simplification? Of course–millions of pages worth of ink have been spilled explaining the precise mechanisms of the crisis, but this is a helpful mental model nonetheless because it helps illustrate what makes today so different. Unlike in 2008, due to changes in regulation, liquidity preference and the Fed’s balance sheet expansions expanding the amount of reserves sloshing around the banking system, banks have a lot more cash or cash-like assets available to them. Even if tech stocks were to continue to crater, banks are simply far more run-proof than they were in the late 2000s.

In other words, 2008 wasn’t a catastrophe because the stock market fell. It was a catastrophe because the specific conditions of the financial system enabled small issues to snowball into an unmitigated disaster. Those conditions simply no longer exist.

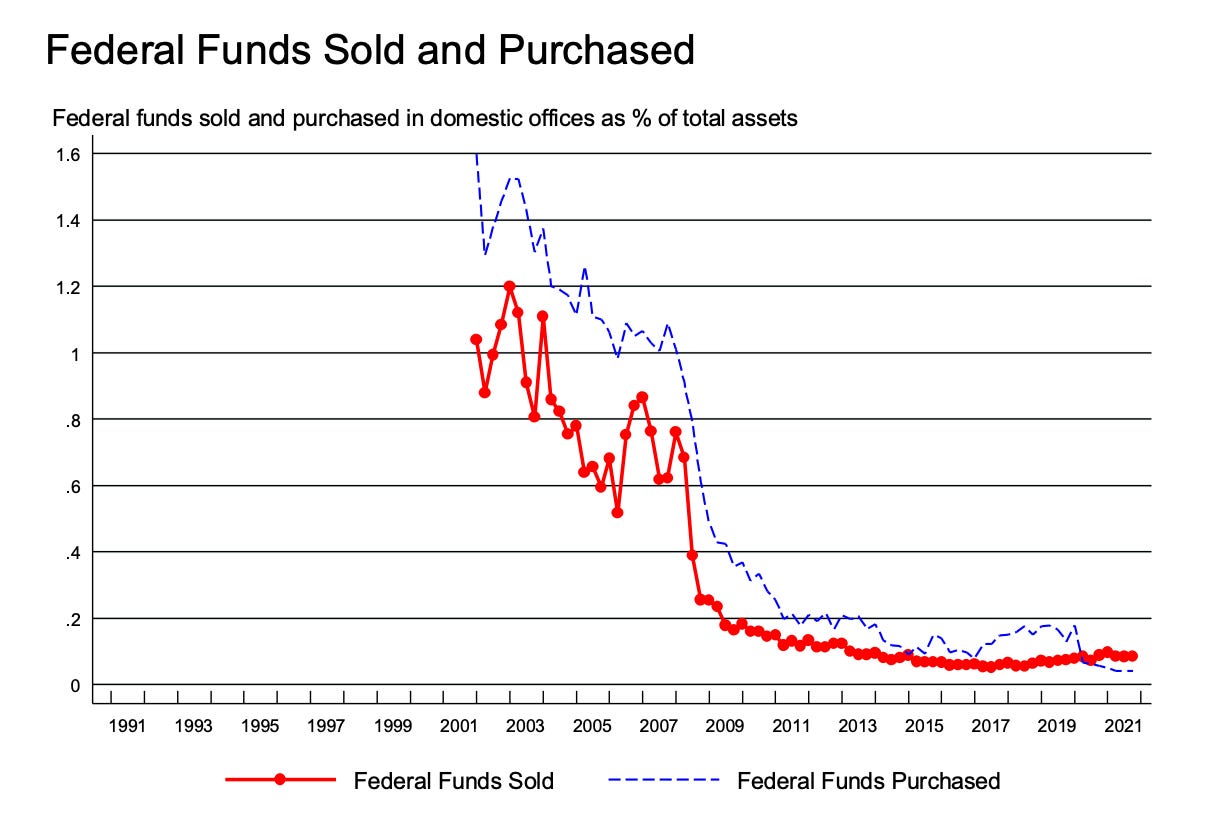

Overnight borrowing on the Fed Funds market is way, way down since the pre-crisis era (source: Federal Reserve Bank of New York)

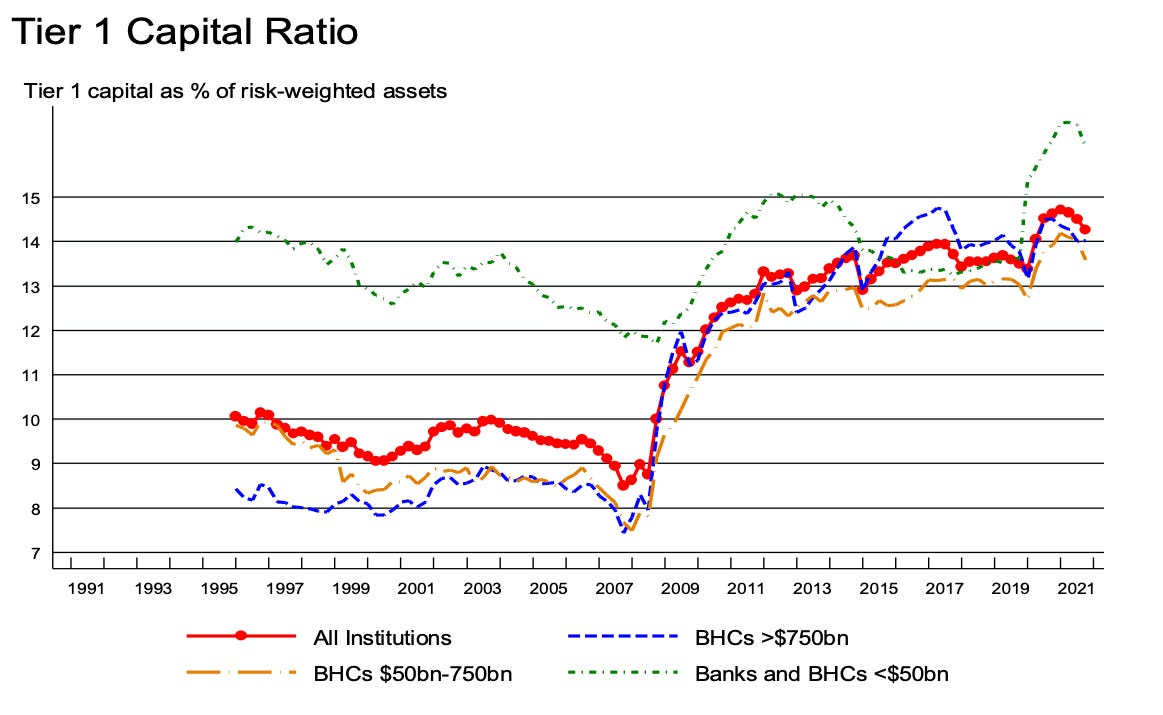

The FRBNY puts out dozens of charts each year on bank capitalization risk and they all tell the same story–banks are far far better capitalized today than in 2008 (source: Federal Reserve Bank of New York)

A bit of a crude measure, but cash assets on bank balance sheets are now a far greater share of their total liabilities (source: FRED)

Job market and demand indicators remain strong

The other major difference between 2008 and today is the forward-looking demand indicators. Unemployment currently stands at 3.6%, with prediction markets estimating a 64% chance that unemployment will drop below the pre-pandemic high of 3.5% this year and a 61% chance that the employment-population ratio will surpass the pre-pandemic high of 80.4% this year. That doesn’t seem like a labor market that’s about to crater! Consumer spending remains robust, with retail sales jumping 0.9% in April. Domestic demand remains extremely strong.

What about the negative GDP print? That was certainly disappointing, but a lot of it was negative inventory drawdowns that are unlikely to persist next quarter. The Atlanta Fed GDPNow forecast expects the second quarter GDP to grow at a 2.5% annualized rate (the Blue Chip consensus is closer to 3%). 2008 this is not.

Even 2000 is a poor analogy

The 2000 analogy is a bit closer to the mark, since both centered a frothy tech market crashing down to earth. But the magnitudes are quite different. The Nasdaq-100 (an index of tech stocks) fell 60% in 2000. While the Nasdaq-100 is now down 25% on the year–it’s still only back at the levels of 2020. The drawdown is half as large as 2000.

Of course, this begs the obvious response: what if the collapse continues? It’s certainly possible! And then it’d be worth revisiting these claims. But the market has already priced in several further rounds of Fed tightening this year, same as they’ve priced in recent troubles with the Chinese ports. If it was inevitable that tech stocks would fall much further, people would sell off today in anticipation and the price collapse would already have occurred. That’s not to say that a further collapse is impossible–but a further collapse would likely be a function of new, unexpected information (such as worse-than-expected earnings reports, or worse-than-expected inflation inducing even faster rate hikes) and not what is already known.

In my amateur opinion, most of the stock collapse is a function of two factors: first, a tightening interest rate environment means that lenders have a greater preference for current profitability over future growth (in other words, if stocks have a relationship to the discounted present value of future dividends, then the discount rate just went way up). For tech companies previously trading at high price-to-earnings ratios, tightening discount rates is definitely bad news. Second, a lot of people (myself included) expected that many of the major consumer changes during the pandemic would be somewhat enduring. This belief manifested in record-high stock prices for Covid darlings like Zoom, Amazon, Peloton and Netflix. As it became clear that these changes were either just pulled-forward growth or one-off events, these prices came back down to earth. But due to strong bank balance sheets, high levels of pain already priced in, and far lower price-to-earnings ratio than back in 1999, I strongly suspect that the current selloff will likely not manifest in a broader crash.

However, all is not great

All of the above sounds vaguely pollyannaish. However, saying “there is unlikely to be a historically bad recession” is not the same thing as saying economic conditions are great. Historically high inflation has meant that real wages have fallen 2.6% over the last year.

Derek Thompson over at the Atlantic has a great round-up of all the risks still facing the economy, from the Chinese port mess, to an impending European recession and heightened domestic debt levels. These trading partner economic crises could severely impact US exporters, and declining equity prices could disincentivize investment and hiring. If you have large amounts of money in stocks, or work at certain tech companies, the good times are (at least for now) definitely over.

What then is an apt analogy? The closest is probably 1991 (even if the causes are quite different), where a minor recession cost George HW Bush the presidency but didn’t cause a decades-long economic disaster like 2008. In short, the situation is grim but hardly apocalyptic.