Thread

Last week I visited a half-dozen hardware companies throughout the western US, with a heavy climatetech bent. It solidified previous impressions I had into reality. While all very different, a 🧵 of some patterns across them, covering policy, geopolitics, and teams:

1/ First, this is well known, but the trip really drove home that our climate future is a revolution in atoms, not bits. And not just some atoms, lots and lots of atoms, which means huge factories and production sites. Exciting to see them start getting built!

2/ There will certainly also be software plays that aid in the transition, but success at its core is always measured in moving atoms. And folks across the country are starting to build up the real infrastructure needed to deliver them.

3/ The scale of the hardware is impossible internalize w/o seeing in person (and then still hard). The pics I took don't capture the feeling. The early dev machinery fills huge warehouses. Full production will be stunningly grand in scale.

4/ Nearly every company mentioned feeling pushed out of California to setup operations, or opting out of starting in CA because it's so hard and slow to build here. It's the industrial version of @ezraklein's excellent piece:

www.nytimes.com/2022/03/13/opinion/berkeley-enrollment-climate-crisis.html

www.nytimes.com/2022/03/13/opinion/berkeley-enrollment-climate-crisis.html

5/ Deeply ironic given that many of these same companies have CA as their 1st market, and want to be close by to keep transportation costs down. As a result, CA climate funding is being prevented from being recycled into local businesses, jobs, and, eventually, taxes.

6/ As an example, we need to not only incentivize the purchase of heat pumps, train local workers to install them across CA, and update permitting rules to enable fast install, but also enable and encourage end-product and parts manufacturing here to get the full econ benefit.

7/ Many folks now leading this new wave of companies are from California, loved living in CA, but just don't see it as tenable to set up their climatetech/hardware businesses there to scale in the long-run. Huge loss to California innovation and economy.

8/ Worrying trend that software companies are becoming remote-first, so less tied to CA, in parallel with one of the next big waves of innovation and wealth-creation coming from climatetech/hardware feeling stymied in CA, and moving away, with taxes following.

9/ And this isn't coming from a Miami-flyer. I grew up in Santa Barbara, have lived in SF since college, and want to be maximally optimistic about our future here. So it's hard to see innovators and builders of our clean infrastructure economy feeling pushed out.

10/ In climatetech, there's a consistent push towards verticalization, as a result of rapidly building new industrial sectors at scale. Co's need higher vol of new parts than any suppliers yet produce. If that capacity has to be built for the 1st time, might as well be internal.

11/ There are certainly still many supplier relationships, and often suppliers and buyers are both scaling rapidly in parallel. With a focus on efficiency, there's strong pull for these to be geographically clustered, sometimes around raw material availability.

12/ Seeds being planted in now in terms of where still relatively early manufacturing efforts are being setup have the possibility of completely transforming the job markets where they're based.

13/ The new mineral economy's shifting supply chains will also shift geopolitics, great @drvolts podcast on that below. US patriotism runs high amongst the folks racing to build and scale manufacturing capacity here.

www.volts.wtf/p/volts-podcast-jason-bordoff-and-meghan

www.volts.wtf/p/volts-podcast-jason-bordoff-and-meghan

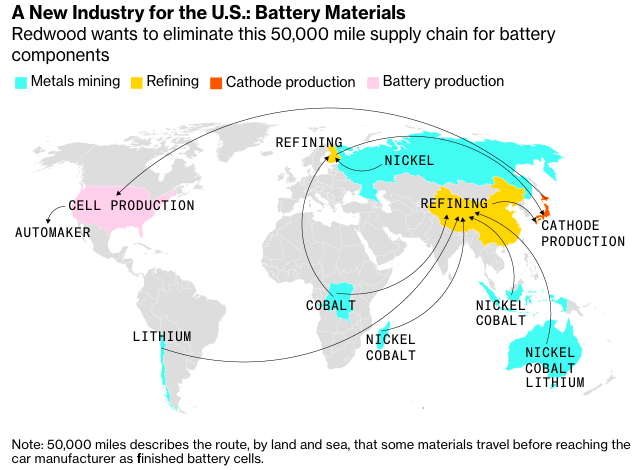

14/ As just one example, EV batteries currently depend on an incredibly global supply chain, with many single-country bottlenecks. Supporting efforts to bring mining (and recycling) and manufacturing capacity to the US will be the new version of "energy independence."

15/ The set of founders and execs building hardware companies, seems to trend older than parts of the software ecosystem. "Hardware is hard," and coming in with strong past operational experience, access to major capital, etc. helps.

16/ One founder archetype is early/senior ex-employees of Elon companies (mostly Tesla so far). Already seeing lots of these, expect many more.

climatetechvc.org/%F0%9F%8C%8F-tesla-graduates-new-climate-mafia-65/

climatetechvc.org/%F0%9F%8C%8F-tesla-graduates-new-climate-mafia-65/

17/ Another is the software exec, translating biz exp. The timing of younger folks being able to start SW cos in the last 2 decades, and then be well-positioned to leverage their "trial by fire MBA" into climatetech now made the 2000's+10's an incredible time to get started.

18/ At the same time, lots of founders expressed finding themselves in their current roles thinking "why me?" They followed their curiosity + started pulling a 🧶, then found next to nothing on the other side, and figured if no one else was yet solving it, they might as well try.

19/ Even Elon fits into this category. He originally just wanted to send some plants to Mars, but couldn't find a reliable, cheap rocket. Might as well build one at that point!

www.vice.com/en/article/jp5g8k/spacex-is-because-elon-musk-wanted-to-grow-plants-on-mars

www.vice.com/en/article/jp5g8k/spacex-is-because-elon-musk-wanted-to-grow-plants-on-mars

20/ For the curious and driven, there's huge whitespace out there (in climate and non-climate hardware). Find the frontier, and push it. Bring friends along — we desperately need all of you.

21/ Finally, you learn a ton seeing stuff in person, and talking directly to the folks working on it. Pictures and interviews never quite do anything or anyone justice. Whatever it is that interests you, just go see it. Make the trip, meet the person.

P.S. This trip also got me thinking abt diversity. There are many programs in software+STEM broadly, but this new critical wave of innovation and wealth generation will be driven by MechE/EE/ChemE/Materials/etc. Who's working on this for students+employees going into climatetech?

Founders also incredibly important directly and indirectly, but there's already more awareness of that 🎉 (still much more work to do there as well, for sure)